groveb/iStock through Getty Photos

Funding Abstract

Corteva Inc (NYSE:CTVA) is a famend international agricultural chemical and seed firm, identified for its constant monetary efficiency and promising progress alternatives. Because the demand for dependable meals provides continues to rise, Corteva is well-positioned to capitalize on this pattern and preserve regular progress. The corporate’s modern merchandise play an important position in addressing this rising want for meals manufacturing.

Space Scarcity (Investor Presentation)

The corporate had a robust begin to the yr, with maybe not parabolic progress however nonetheless a 6% YoY improve in gross sales does assist bolster the outlook for each the corporate and the business it’s in. Presently, the corporate is buying and selling underneath the extent after I launched my first article about Corteva, however I’m nonetheless bullish concerning the outlook for it and can preserve my purchase score. Paying 18x ahead earnings for an organization with stable margins, a historical past of buybacks, and likewise a good dividend yield appears real looking.

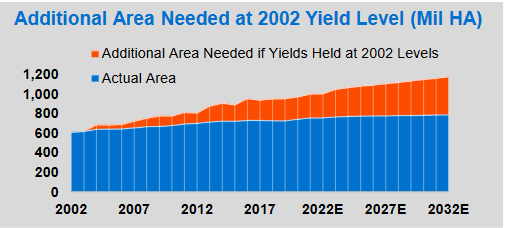

Constructive Market Outlook And Demand

The fertilizer market is experiencing vital tailwinds pushed by the growing demand for meals attributable to a rising international inhabitants. This surge in demand for crops has created a corresponding want for fertilizers. Furthermore, the shift in direction of sustainable and natural agricultural practices has additional fueled the demand for natural fertilizers derived from pure sources.

International Demand (Investor Presentation)

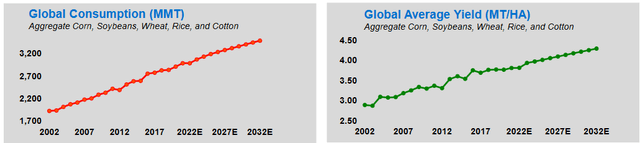

The fertilizer market is carefully intertwined with the seed and crop safety markets, as all three sectors contribute to the expansion and vitality of crops. Each standard and genetically modified seeds are projected to witness regular progress, pushed by components equivalent to inhabitants progress and the hunt for dependable meals sources. Moreover, the battle in Ukraine has created a void within the international market, resulting in a pointy decline in grain and corn provide. This has intensified the demand for fertilizers, as new areas have to be cultivated promptly to compensate for the decreased provide.

Market Postion (Investor Presentation)

In abstract, the fertilizer market is propelled by components like inhabitants progress, the necessity for meals safety, and the aftermath of geopolitical occasions. This creates alternatives for sustained progress and growth within the agricultural business. A spot that Corteva can assist fill with their merchandise. With an already establishes place available in the market they’re extra ready than any to profit from this demand and progress.

Dangers

Corteva faces sure dangers related to commodity costs and potential disruptions within the provide chain. Fluctuations within the prices of important uncooked supplies utilized in its product manufacturing have the potential to have an effect on the corporate’s revenue margins and total monetary efficiency.

Moreover, working in a fiercely aggressive business poses challenges for Corteva. With established opponents and new gamers coming into the market, the corporate should navigate intense competitors. This aggressive panorama might exert strain on pricing and doubtlessly affect Corteva’s market share.

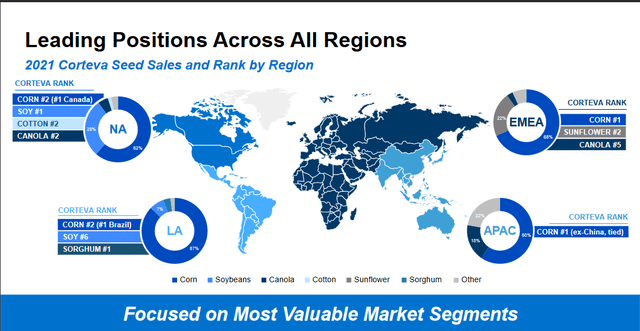

Market Income (Investor Presentation)

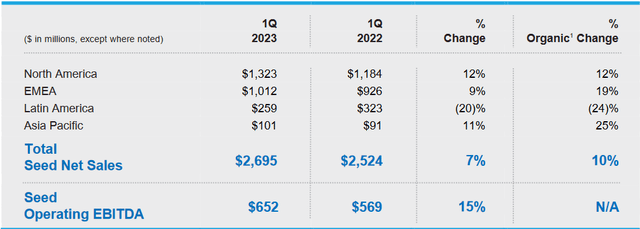

The place I maybe would possibly see a slight threat is the Latin American market. it was highlighted within the final report by the corporate, the place the web gross sales decreased by 20% for the seed section of the corporate. Thankfully, the remaining markets they’re in serving to the section develop at 7% YoY no less than. A few of the notes by the corporate right here is that Latin America appeared to have constraints in corn provide. Going ahead I believe this will probably be key to be careful for. I believe seasonality points like this are to be increasingly anticipated as local weather change is taking its impact on the business.

Financials

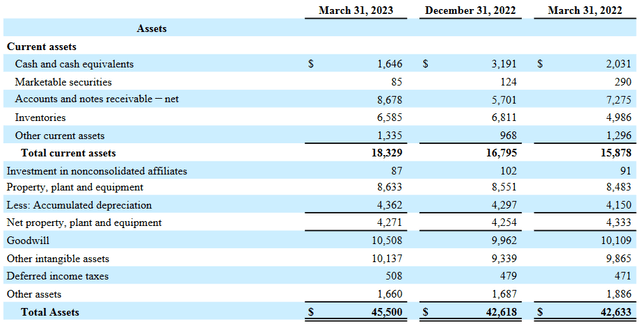

Shifting over to the financials of the corporate they’ve seen a fairly drastic decline within the money place, going from over $3 billion in This fall of 2022 to underneath $1.7 billion within the final report. Nonetheless, the present belongings have elevated considerably primarily pushed by a rise within the receivables. Pushed by elevated demand and a gentle demand for fertilizers throughout the a number of markets the corporate operates in. I believe this offers proof of the spark that also exists on this business and although final yr’s run-up was nice for an organization like CTVA, the trajectory continues to be upwards.

Belongings (Stability Sheet)

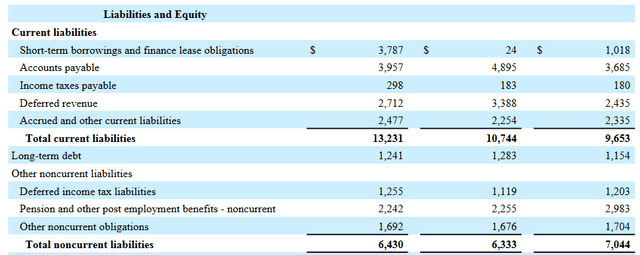

The place I see some fear right here is the present liabilities creeping up slowly to the identical as the present belongings. The corporate has near $4 billion in short-term borrowings which the money place is in fact not capable of deal with. The rise is drastic as in This fall 2022 it was near 0 as a substitute. However with $1.2 – $1.4 billion in FCF estimated for 2023 paired with the money they appear to have the ability to handle this in any case. Trying on the long-term money owed as a substitute, they sit far decrease at $1.2 billion proper now. 2023 will probably be an fascinating yr when it comes to the event of not simply the enterprise and gross sales, however the stability sheet particularly.

Liabilites (In search of Alpha)

The corporate has a stable web debt/EBITDA ratio of underneath 1 proper now and EBITDA is estimated to extend by 13% on the midpoint in 2023 in comparison with 2022, I’m assured they are going to be capable of navigate their financials effectively. Going into the remaining reviews for the yr, I do not anticipate to see a robust improve within the money place, however as a substitute, a hopeful lower within the short-term liabilities as a substitute. All in all, I believe Corteva stays financially steady and do not see sufficient of a motive right here that might deter funding within the firm.

Valuation & Wrap Up

I imagine Corteva is a superb possibility to achieve publicity to the fertilizer market. The corporate holds a robust place right here and may supply worth not simply by progress within the firm, but additionally with a dividend yield of 1.09% and a stable share buyback historical past. Taking a look at comparable firms within the sector, one which involves thoughts is The Mosaic Firm (MOS). The place I see the advantage of proudly owning CTVA as a substitute of MOS is the superior progress trajectory they’ve. Earnings for CTVA are anticipated to develop round 10% CAGR the following 5 years, whereas MOS is predicted to see a virtually 30% decline in EPS as a substitute. With this earnings trajectory for CTVA I believe they arrive out forward in comparison with MOS.

Regardless of MOS having FWD p/e of simply 6, the dearth of future earnings progress possible helps with preserving the corporate at this low a number of. Shifting over to margins, MOS does have a stable backside line with a web margin of 15%. MOS hasn’t used these robust margins to assist construct up a stable stability sheet, as a substitute it appears a lot of the capital has gone to buybacks and dividends as a substitute. CTVA has to this point been capable of preserve a really robust money place in comparison with the debt, one thing I do not see with MOS, and that does carry threat into the calculation, an element I believe results in the corporate buying and selling on the low a number of it does. For example, CTVA has 1.3 as a lot money at hand as long-term debt, whereas MOS has 5x as a lot long-term debt as money presently.

Inventory Chart (Inventory Chart (In search of Alpha))

The market is ripe to proceed rising as the need to determine robust and dependable meals provide routes will probably be key. Corteva can assist with this immensely. Corteva is continuous to accumulate firms to assist develop their enterprise which has resulted in an EPS steering of $2.8 – $3 for 2023, placing the corporate at a ahead p/e of about 18. It is a valuation I’m glad to pay and will probably be score Corteva a purchase, and it isn’t far above the historic common both. The sector’s common p/e appears to be round 12 – 14 on a ahead foundation. Why I see a purchase for CTVA even at the next a number of then that is the stable progress I see the corporate having, which I believe is price paying the premium for. Other than that, it is a well-run firm that has a steady dividend and a stability sheet that appears nice. That kind of stability is price paying just a little bit additional for for my part.

{kind=link}