Sundry Images

Funding Thesis

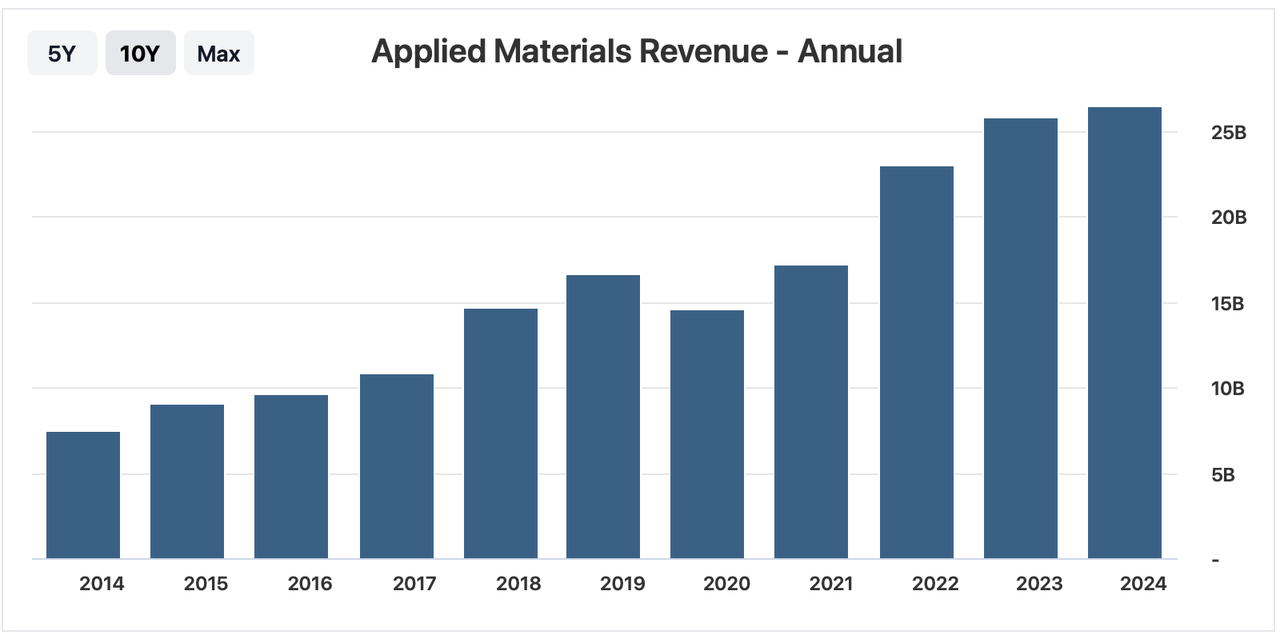

I consider Utilized Supplies (NASDAQ:AMAT) has demonstrated sturdy income and EPS progress and that is set to proceed. During the last 10 years, Utilized Supplies has seen sturdy income progress. In 2014, income totaled $7.51 billion; 2024 income is the same as $26.52 billion, a 353% improve.

Trying ahead, consensus income estimates have proven this compounding persevering with, with income projected to extend from $26.94 billion in fiscal 2024 to $37.36 billion in fiscal 2028.

One of many largest issues about semiconductor shares is their cyclical nature, main some traders to consider semiconductors need to commerce at a decrease price-to-earnings (P/E) a number of.

Nevertheless, I consider that some semiconductor firms, like Utilized Supplies, don’t comply with this cyclical nature. I believe that the market’s opinion on the {industry} (and Utilized Supplies) is starting to vary as semiconductor quantity accelerates, pushed by developments in know-how and growing demand pushed by the AI revolution.

Including to this, Utilized Supplies has showcased constant income and earnings per share (EPS) progress even earlier than the AI growth. Within the final 10 fiscal years, their income compounded annual progress charge (CAGR) was over 13%, and their Non-GAAP earnings per share grew at roughly 30%.

With the expansion of AI, I consider Utilized Supplies will profit considerably. As an organization, they have already got a powerful historical past of executing wonderful income and EPS progress. With growing demand for AI purposes, I count on Utilized Supplies’ income and EPS progress to speed up additional. Given the conservative progress estimates (under these present progress charge estimates), which I consider are prone to be revised upward, Utilized Supplies represents a compelling sturdy purchase.

Background: Sturdy Compounder

Utilized Supplies has proven to be a constant compounder of earnings per share (EPS) and income. Contributing to this are their three key working segments— semiconductor programs, utilized world providers, and show and adjoining markets.

Zooming out to the previous 10 years, Utilized Supplies has seen regular income and EPS progress, as displayed within the charts under.

AMAT Annual Income (Stockanalysis)

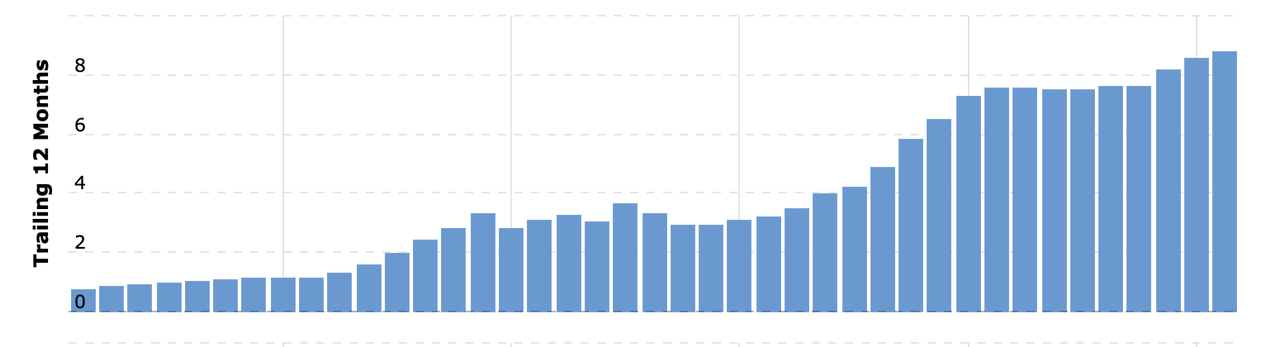

EPS has seen this even stronger compounding, which has been much more spectacular. On nearly all the rolling 12-month durations over the past 10 years, EPS continued to compound greater. In truth, EPS has elevated by over 8x on this timeframe. That is highly effective.

AMAT EPS Development (Macrotrends)

This graph exhibits the EPS of Utilized Supplies, displaying an EPS of $.88 in October 2014, and an EPS of $8.77 as of Might 2024. This equals a rise of 996%. That is the place administration will get their 30% CAGR of EPS they reference of their most up-to-date earnings name.

Trying Ahead: Development Seems Understated

I consider we’re within the midst of an enormous AI transformation, but the expansion estimates for Utilized Supplies (Utilized Supplies) appear conservative. Regardless of the speedy developments and growing demand for semiconductor know-how pushed by AI, with Utilized supplies enjoying a key function in retooling amenities that make DRAM (like Micron (MU) which is seeing sturdy order bookings on their very own), income and EPS progress projections for Utilized Supplies stay under the {industry} common. As an illustration, Utilized Supplies’ estimated ahead income progress charge is about far under their 10-year private CAGR of 13%, projected at 5.25%.

That is additionally under the sector median of 6.64%, indicating a 20.95% distinction. Within the occasion of an enormous AI revolution, I consider their actualized income shouldn’t solely exceed predictions and the sector median, but additionally their private common of 13%. Equally, the ahead EBITDA progress charge is projected at 4.43%, additionally under the sector median of 6.38%. I believe what we’re seeing here’s a related setup to Micron just a few months in the past. Utilized Supplies is a key a part of the brand new AI future, serving to provide instruments to DRAM makers like Micron. As soon as Micron’s order guide necessitates new fab retooling, I count on orders to choose up in a fashion stronger than what estimates are penciling in.

As highlighted in my current evaluation on ASML (ASML), the semiconductor {industry} is present process a major retooling to accommodate the wants of AI purposes. For instance, ASML’s superior lithography machines are in excessive demand, and this demand is predicted to drive substantial progress throughout your entire semiconductor provide chain. Utilized Supplies, being a vital participant in semiconductor gear, stands to profit immensely from this identical industry-wide improve cycle. What I’m saying right here is we’re seeing the downstream impact on different firms that retool fabs. I’ve no cause to consider we is not going to see this identical uptick in progress with Utilized Supplies.

I consider analysts are starting to acknowledge the expansion potential of this firm. Utilized Supplies’ consensus income and EPS estimates have proven constant upward revisions. For the upcoming fiscal yr, the variety of upward revisions for EPS within the final 3 months stands at 21, in comparison with 7 downward revisions. For income, there are 21 upward revisions towards 8 downward revisions.

In truth, now we have seen EPS estimates for simply this yr improve by 8.86% for the fiscal yr ending October 2024. This has taken EPS estimates from a lower to a now 3.97% year-over-year progress estimate. I nonetheless suppose these estimates might turn into too conservative, particularly given how briskly AI DRAM orders are ramping up at Micron.

The necessity for substantial semiconductor retooling for AI will likely be a significant progress driver for Utilized Supplies. As your entire semiconductor {industry} gears up for AI retooling, the demand for Utilized Supplies’ gear is predicted to leap. As talked about of their Q2 2024 earnings name,

…the superior chips that energy AI datacenters are enabled by 4 key semiconductor applied sciences: modern logic; compute reminiscence or high-performance DRAM; DRAM stacking know-how, known as high-bandwidth reminiscence, or HBM; and superior packaging to attach the logic and reminiscence chips collectively and create a ‘system in a package deal’.

Utilized has course of know-how management in all 4 of those areas, and now we have made vital investments in next-generation options to make attainable the important thing machine structure inflections which might be important for our clients’ future roadmaps. – Q2 2024 earnings name

I consider this assertion solidifies my thesis. As firms retool Utilized leads in these key areas; they’ll look in the direction of Utilized Supplies to offer the wanted know-how.

Valuation

Utilized Supplies’ valuation metrics, I consider the market is underestimating their potential for progress. For instance, their ahead P/E (GAAP) ratio is 28.71, which is under the sector median of 29.67, representing a 3.24% low cost.

Throughout the earnings name, CEO Gary Dickerson talked about a number of avenues of progress, one being the spending on course of gear for transistor steps. Dickerson acknowledged:

With the gate-all-around transition, we’re additionally gaining share, and we’re on observe to seize over 50% of the method gear spending for transistor steps. – Q2 2024 earnings name

Including onto this, Dickerson additionally acknowledged in the course of the name

We even have very sturdy market share in interconnect or the wiring used to transmit information at excessive velocity and low energy. Our obtainable marketplace for the wiring steps is roughly $6 billion for every 100,000 wafer begins per thirty days, and we count on it to develop by $1 billion when bottom energy supply is launched into quantity manufacturing. General, we count on to generate greater than $2.5 billion of income from gate-all-around nodes this yr and doubtlessly greater than double that in 2025.

– Q2 2024 earnings name

He simply stated some components of their enterprise will double in 2025 (a $2.5 billion division will double in 2025). The remainder of the corporate would severely need to underperform as a way to have income progress of 5.25% like what’s projected.

Shifting to their excessive bandwidth reminiscence (HBM) sector, Dickerson talked about:

[we] have lately seen clients speed up their capability plans for HBM, we now consider that our income might be 6x greater this yr, rising to greater than $600 million. Throughout all machine sorts, we now count on income from our superior packaging product portfolio to develop to roughly $1.7 billion this yr. – Q2 2024 earnings name

As demonstrated by these quotes from Utilized Supplies’ most up-to-date earnings name, the corporate is predicted to see exponential progress throughout a number of sectors, however the market doesn’t appear to agree.

Nevertheless, even with these conservative estimates, Utilized Supplies’ FWD (GAAP) EPS progress is projected to be 22.85% above the sector median over the following 12 months.

We’re at the moment paying a 3.24% to sector median GAAP P/E ratios to entry a compounder that’s estimated to develop (in what is probably going conservative estimates) 22.85% above the sector median. I believe it is a nice deal.

If we noticed their ahead P/E (GAAP) ratio acquire a 22.85% premium above the sector median, this is able to then equal a ahead P/E of 36.45. This ahead P/E would end in 26.96% upside in shares if the ahead P/E had been to converge on this progress premium.

Dangers

Regardless of the sturdy progress potential and enticing valuation of Utilized Supplies, there are a number of dangers that traders ought to contemplate. Probably the most vital threat is the geopolitical stress surrounding China. The U.S. authorities is contemplating further restrictions on China’s entry to superior semiconductor know-how, which might affect Utilized Supplies’ enterprise. Particularly, the U.S. is trying to curb China’s capacity to make use of superior chip architectures like gate all-around (GAA) know-how, which is essential for AI purposes.

Any extreme restrictions might result in a major drop in Utilized Supplies’ income from the Chinese language market. Nevertheless, it is essential to notice that most of the newest AI chips can’t be manufactured in China because of current bottlenecks and restrictions on vital applied sciences like these offered by ASML. This limitation partially mitigates the affect on Utilized Supplies, because the demand for his or her superior manufacturing gear stays excessive in different areas. On prime of this, any gear Utilized Supplies ships to China is probably going not their most superior gear, since different components of the AI chip making course of in China are bottle-necked by the dearth of superior know-how from ASML.

As talked about beforehand, the AI world is due for a retooling. In China, Utilized Supplies might assist with this retooling. Within the earnings name, Gary Dickerson talked about:

So, as that DRAM enterprise falls off, our ICAPS enterprise and our modern logic enterprise does improve to fill that in. And so, that is in keeping with continued power in ICAPS, which the remainder of the marketplace for us in China can be ICAPS-related. – Q2 2024 earnings name

This means that though Utilized Supplies might lose components of their DRAM enterprise in China, there are different avenues that may proceed to drive progress. For instance, as of 2022, the CHIPS Act was handed aiming to make america a fundamental producer of semiconductor chips. Due to this, firms like Micron wish to construct new amenities within the U.S., which is able to should be stuffed with Utilized Supplies machines. As extra firms prioritize U.S. manufacturing, I consider extra firms will look in the direction of Utilized Supplies for equipment.

Backside Line

I consider Utilized Supplies presents a powerful purchase, pushed by their constant income and earnings per share (EPS) progress. Regardless of historic issues on the cyclical nature of semiconductors, Utilized Supplies’ long-standing capacity to compound income and EPS, with projections indicating vital progress forward, mitigate these issues.

Whereas conservative progress estimates have saved their valuation under sector median, the continuing AI revolution and the required retooling throughout the semiconductor {industry} current substantial upside potential. Though geopolitical dangers in China are a priority to some traders, I consider with the rising demand for AI, the remainder of the world will make up for any downturn in income from China.

{kind=link}