Bilanol

Funding Thesis

GE Vernova (NYSE:GEV) is primed to capitalize on hovering energy demand, leveraging their spectacular put in base of progressive fuel and wind generators. Below CEO Scott Strazik’s management, GEV is gearing up for big earnings development, because of intense administration refocus on bottom-line margin enchancment and operational effectivity. GEV’s Energy phase is on a strong development trajectory, bolstered by a sturdy backlog of $72.8 billion and robust demand for superior fuel generators and companies. The Electrification phase can be quickly increasing, fueled by the secular traits of AI knowledge facilities and the necessity for grid modernization and high-voltage direct present (HVDC) applied sciences. Basically, we additionally see that the renewable phase is about to interrupt even in 2024 and switch worthwhile by 2025, promising substantial upside.

In the intervening time, GEV’s excessive ahead P/E ratio of 40.04x may make some buyers hesitant, however there’s extra beneath the floor. The corporate’s income stream is spectacular, and though it is a lower-margin enterprise with an unprofitable wind phase, administration steerage exhibits important strides in operational optimizations and margin enhancements. Our evaluation exhibits that GEV is at the moment undervalued, with a 17.03% upside to a goal share value of $197.49 from its value of $168.76 as of 6/17/2024. This makes GEV a compelling medium-term funding alternative, with the potential for larger returns as the corporate continues to optimize and develop independently.

Firm Overview

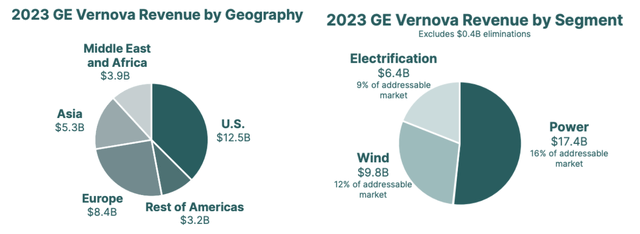

Buying and selling beneath the brand new ticker GEV, GE Vernova inherits the legacy and scale of its guardian firm GE, serving as a key participant in driving the worldwide transition in direction of sustainable and dependable power options. GEV gives superior gear and companies for fuel, nuclear, hydro, and steam energy, in addition to wind generators and grid applied sciences. This firm portfolio is organized into three segments: Energy, Wind, and Electrification. GEV is built-in in each the upstream and downstream channels of energy technology. At a high-level, they supply gear obligatory for producing energy from each fuel and renewable sources, provide upkeep, upgrading, and operational companies for these gear, and supply further storage options and grid applied sciences to optimize channels of electrical energy to customers. By way of this unified operation, GEV’s services have been utilized in over 100 nations by main utilities, builders, and governments to generate roughly 30% of the world’s electrical energy.

GE Type 10 Submitting

GE Vernova’s spin-off from Normal Electrical (GE) simply two months in the past has been a game-changer, marking a big strategic transformation geared toward enhancing operational effectivity and focused development. Traditionally, GE’s conglomerate construction with vastly completely different and huge enterprise veins led to capital inefficiencies, company waste, and general lack of strategic route. One of many main issues was that GE’s centralized construction created layers of administration that slowed decision-making processes, making it troublesome for particular person segments to adapt rapidly to market adjustments. This inefficiency was significantly evident within the renewable power and energy segments, the place fast technological developments and market dynamics required agility and swift execution. Moreover, capital allocation inside GE was suboptimal. The conglomerate’s various portfolio meant that worthwhile segments sponsored underperforming ones, resulting in misallocation of sources, particularly within the wind and renewable power divisions, which struggled with excessive mission prices and low margins. Now, as an unbiased entity, Vernova can function with larger agility and independence, whereas benefiting from GE’s backing, permitting for higher monetary stability and mortgage charges – getting the very best of each worlds.

Phase Enhancements

Diving into every phase of GEV’s operations, there’s rather a lot to unpack as latest administration steerage on enhancing prime and bottom-line development provides us purpose to be optimistic about GEV.

Energy phase

That is GEV’s largest and contains fuel, nuclear, hydro, and steam applied sciences. This phase depends on two most important income streams: gear gross sales and companies. Its gear portfolio of superior fuel generators, nuclear reactors like small modular reactors (SMRs), hydroelectric mills, and steam generators, introduced in $1.2 billion in Q1 2024, accounting for 29.5% of the facility phase income. The true revenue-driver, nonetheless, comes from the extra companies GEV gives on their gear, like upkeep, upgrades, and repairs. These companies pulled in a $2.8 billion in Q1 2024, making up 70.5% of the income. These aren’t simply one-off offers either-they’re backed by long-term service agreements (LTSAs), which give a steady and recurring income stream, serving to insulate GEV towards the ups and downs of kit gross sales. GEV is assured about this stream of income, as roughly 70% of their present contracts final over 10 years. Given the excessive service contract renewal charges and hike in demand for gear, GEV is ready to upsell further companies and upgrades, general enhancing margins.

Inside energy, the basics for the fuel facet are robust and nonetheless rising at this second. As of April, GEV had utilities working round 7000 fuel generators worldwide with 1700 items beneath LTSAs, producing over double that quantity of rivals. Because the power trade continues to ditch coal for cleaner alternate options like pure fuel, clients might be investing in additional fuel generators, including on extra capability to the put in base and subsequently extra companies, which is able to drive north of $2 billion of free money circulation a 12 months. We have already seen this demand come into fruition: GEV reported orders up 24% for fuel turbine gear, including to their intensive backlog of roughly $14.4 billion in gear and nearly all of $58.4 billion in service. For now, with the sustained fuel energy demand, robust income visibility for the following years, and increasing EBITDA margins, the fuel energy phase is about to be the spine for GEV’s enterprise.

Wind Phase

This phase, alternatively, is a story with extra downs than ups. However because the trade itself has navigated by means of some powerful few years, we’re now recognizing some strong medium-term development alternatives. Separated into each onshore and offshore applied sciences, this phase generates gross sales from wind generators and related service contracts, amounting to complete income of $1.64 billion in 2024.

On the onshore facet, the corporate has seen a big turnaround, reaching profitability in the course of the second half of 2023, and with improved pricing and value cuts, margin expansions are on the horizon. Administration remains to be centered on consolidating its product variants to a extra simplified product suite known as “workhorse merchandise”. This transfer has enabled GEV to streamline higher performing, high-quality belongings, producing them at scale and at decrease prices to enhance gear gross sales, which make up round 85% of phase income. The truth is, the operational enhancements have already proven inside GEV’s price construction and profitability. Mounted prices as a proportion of income lowered by 6 factors and their breakeven level lowered to lower than 1,000 items per 12 months. GEV’s additionally consolidating their geographical attain, focusing primarily on North America for the near-term due to its provide chain footprint and product compatibility. This shift provides important enhancements in mission economics for patrons and turbine producers as new and prolonged tax incentives roll out from the Inflation Discount Act.

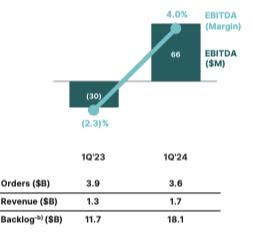

Offshore wind remains to be in muddy waters, and has been a thorn in GEV’s facet for years. They’re coping with an unprofitable backlog of about $4 billion, which they goal to clear by the top of 2025. Not too long ago, the corporate additionally needed to pivot from bigger 18 MW generators to the 15.5 MW Haliade-X mannequin after market difficulties, provide chain disruptions, and inflationary prices. The phase’s unfavourable profitability has been a results of an arduous allowing system with allow delays, which led to renegotiated weaker pricings and better prices throughout inflation. CEO Scott Strazik explains their plan is to be extremely stringent and selective with new tasks, focusing solely on high-margin tasks whereas staying disciplined in contract negotiations, making certain that costs replicate the true price of manufacturing and the danger of allowing delays. Nevertheless, the rapid focus has been clearing the low-margin backlogs, which as they begin coming down, ought to enhance general margins. Regardless of going through challenges, wind together with all the opposite segments noticed enhancements in profitability throughout Q1 with an EBITDA loss narrowing to $173 million from $260 million the earlier 12 months.

For now, GEV’s wind phase is anticipated to see flat income development, however administration is specializing in driving bottom-line development with improved underwriting practices, mission combine, and substantial price financial savings. The long-term upside for GEV’s wind phase hinges on gaining quantity leverage over time, significantly from policy-driven development such because the IRA. These incentives are anticipated to considerably increase demand for wind power tasks and cut back per-unit prices by means of economies of scale, features which have but to be mirrored within the near-term monetary outlook. Though GEV has clear steerage to this point to mitigate offshore wind points, we must always nonetheless be vigilant concerning the wind trade. Pure-play wind firms and shut rivals like Siemens Power (OTCPK:SMNEY) and Mitsubishi Heavy Industries (OTCPK:MHVYF) have proven related unprofitable traits of their wind segments, and GEV could comply with swimsuit on this low margin motion.

GEV IQ 2024 Traders Presentation

Electrification phase

That is its fastest-growing sector, encompassing grid options, energy conversion, electrification software program, and photo voltaic and storage options. In 2024, this phase noticed sturdy demand, with revenues hitting $1.65 billion-a 24% enhance from the earlier 12 months. Grid Options, the biggest a part of this phase, skilled important development on account of high-voltage direct present, HVDC, orders and different transmission actions, driving a 21% income enhance and increasing the EBITDA margin by roughly 600 foundation factors. The truth is, GEV’s grid options newly signed a big settlement to produce two HVDC converter stations to deliver renewable power from the northern a part of the UK to utilization facilities within the south.

GEV is essentially the most bullish on their Electrification phase, and I feel there may be good purpose to be. Presently, the US grid’s effectivity losses are at round 5% and a projected doubling of gigawatts are wanted as electrical energy calls for develop. The phase’s robust market is underscored by a $12 billion order ebook, reflecting a wholesome backlog up $6 billion year-over-year. With a $75 billion addressable market right this moment and a forecasted $175 billion market in 2030, the phase is poised for additional growth and significant upside. GEV is dedicated to investing $1 billion in R&D this 12 months, specializing in advancing applied sciences essential to electrification and decarbonization, particularly grid options, energy conversion, electrification software program, and renewable power integration.

GEV has a well-defined technique for optimizing every of its enterprise segments, positioning the corporate for substantial future development and a commanding market share.

Business Tailwinds

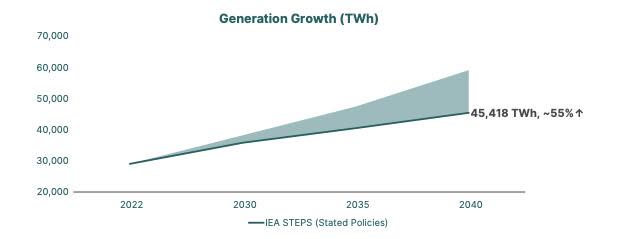

The worldwide power sector is rising significantly, with electrical energy demand projected to surge by over 55% by 2040. This increase is pushed by a number of elements, together with the rise of electrical autos, which accounted for 9% of latest automotive gross sales in 2023, the growing use of electrical warmth pumps, and the large power consumption of information facilities powering AI fashions and blockchain expertise. Knowledge facilities are on the forefront of this pattern. Simply in 2020, the load demand from U.S. knowledge facilities was round 2%; by 2030, this determine is projected to rise to just about 8%.

GE Type 10 Submitting

The U.S. is an particularly ripe marketplace for this development as a result of sturdy infrastructure, aggressive electrical energy costs, proximity to main tech hubs, and substantial authorities incentives. Moreover, knowledge facilities are more and more investing in greenfield tasks – new developments on beforehand undeveloped land-to permit for the development of amenities that incorporate the newest energy-efficient applied sciences and infrastructure from the beginning. Greenfield websites additionally provide the flexibleness to combine renewable power sources like photo voltaic and wind energy, aligning with sustainability targets and regulatory necessities. With its robust foothold within the U.S. and diversified energy useful resource capabilities, GEV is most suited to supply dependable and sustainable power sources and capitalize on the upsurge in demand.

On the renewable power entrance, the IRA gives important tax incentives and credit which can be anticipated to spice up the wind phase. The act extends the Funding Tax Credit score, ITC, and Manufacturing Tax Credit score, PTC, by means of 2024, making wind tasks extra economically viable. The ITC gives a 30% credit score for investments in clear power tasks, whereas the PTC gives 2.6 cents per kilowatt-hour of electrical energy produced from wind generators. The act additionally contains bonus credit for tasks utilizing USA-made elements and people arrange in historically fossil fuel-reliant communities, giving GEV much more perks with their US-centric provide chain. Typically, we see the IRA incentives as an enormous tailwind in ramping up demand and manufacturing for wind power tasks.

Competitor Evaluation

GEV’s closest rival is Siemens Power. The truth is, each had spun off from their guardian firms, comply with related enterprise fashions with a strong deal with energy, wind and electrification, and bolster an order ebook of over $100 billion. The massive distinction is geography: Siemens Power is a pacesetter within the European market, whereas GEV is stronger within the US. The income image is as follows: Siemens reported $83.09B in income and optimistic internet earnings of $8.50B, which interprets right into a internet margin of 12.27 %. On the flip facet, GEV paints a bleaker image: with $33.245B in income however a internet lack of -$438M, as points persist within the wind phase’s profitability.

Despite their completely different monetary performances, each share a BBB credit standing from S&P. GEV’s score is because of its low margins over the previous couple of years and uncertainty in efficiency following its latest spin-off. Siemens Power’s score comes from important losses in its wind trade in 2023, brought on by high quality points and the fast rollout of latest turbine fashions. Their onshore generators, together with the 4.X and 5.X, had technical points with rotor blade wrinkles and bearing particles, resulting in excessive restore prices.

With such headwinds, GEV is buying and selling round 14.7x estimated 2025 EBITDA, whereas Siemens is at 7.3x; therefore, the market is placing a reduction on Siemens. A big purpose for that is GEV’s stronger US leverage and put in base, which is anticipated to develop and enhance higher-margin service gross sales. Moreover, decrease valuations might come from Siemens Power’s repurchase of Indian belongings bought in 2023, which is estimated to be value between $2 and $6 billion.

Deal with Margin Enchancment and Operational Effectivity

Administration is repeatedly honing of their lean manufacturing technique, an operation that has been occurring for a number of years, meant to chop company waste and increase operational effectivity throughout their channels. This top-down dedication from management is all about fostering transparency, problem-solving, and steady enchancment at each stage. As an example, at their Greenville, South Carolina facility, they’ve applied single-piece circulation, leading to a 40% enhance in manufacturing quantity and a 35% increase in each day output, all whereas lowering cycle occasions and scrap charges. Within the Fuel Energy phase, its been pivotal within the elimination of $1 billion in fastened prices since 2018, considerably enhancing buyer expertise and long-term efficiency. Throughout its numerous segments, cost-savings have already been realized: roughly $300 million within the Electrification phase and $500 million within the Onshore Wind enterprise over the previous three years. This strategy has been essential in boosting GE Vernova’s backside line. With ongoing cost-cutting efforts post-spin-off, we anticipate that GE Vernova will acquire a aggressive benefit as a leaner, extra worthwhile participant within the power sector.

On the finish of this Might, GEV bought a portion of their Steam Energy enterprise to EDF, as soon as once more demonstrating administration’s resolve to refocus on strategic areas and minimize prices. This deal is taking the manufacturing of typical island gear for brand spanking new nuclear energy vegetation and associated upkeep off their palms. With this monetary burden lifted, GEV is now zeroing in on high-margin, development areas, placing the sources again into boosting service capabilities and investing with small modular reactor (SMR) applied sciences, key for the continuing power transition.

Valuation

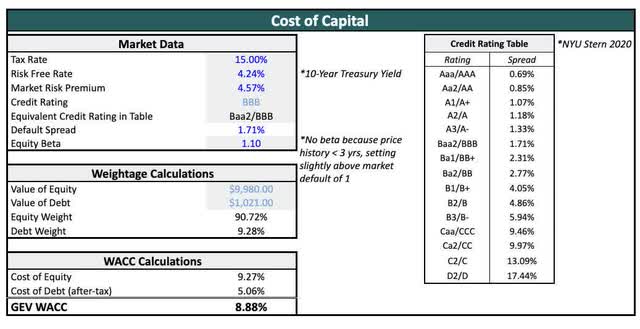

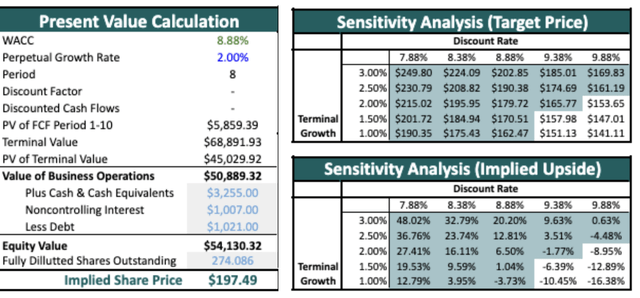

We used a Discounted Money Movement mannequin over an eight-year interval to derive GEV’s intrinsic worth. The Weighted Common Value of Capital is 8.88%, reflecting the 10-year US Treasury yield, market threat profile, credit standing, and the predominantly equity-based capital construction. On account of GEV’s brief pricing historical past, we set the sector-specific beta barely above the default market beta.

QOE Capital – Analyst Madison Huang

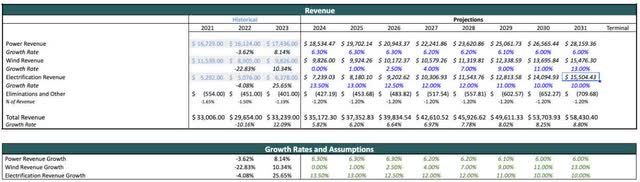

GEV’s top-line development for the upcoming years is anticipated to be pushed considerably by the Fuel Energy and Electrification segments, whereas transitioning to a larger dependence on wind within the long-run because it achieves profitability and margin growth. The Fuel Energy phase, bolstered by elevated orders for HA and Aero-derivative fuel generators and a $72.8 billion backlog, is projected to realize a mid-single digit annual development charge. The Electrification phase, which skilled a 24% income enhance in 2024, is anticipated to take care of sturdy low double-digit development pushed by the secular demand for grid options and an inflow of high-voltage direct present (HVDC) orders. Whereas Wind phase revenues are anticipated to stay flat as GEV addresses its backlog, the offshore wind phase is projected to show worthwhile by the top of 2025, enabling quick future income development. General, complete revenues are projected to develop at an annual charge of round 6.2%.

QOE Capital – Analyst Madison Huang

Transitioning to the calculations wanted for EBIT and EBITDA, we forecasted working bills as a proportion of income. We consider that GEV’s lean manufacturing practices will considerably cut back COGS regardless of inflationary pressures. SGA bills are anticipated to rise on account of increased company prices related to working as a stand-alone public firm, and R&D expenditures are additionally anticipated to extend as GEV invests in new electrification and decarbonization applied sciences.

The earnings tax charge for 2023 was -10.4%, reflecting a tax provision on a pre-tax loss on account of taxes in worthwhile jurisdictions and a valuation allowance on deferred tax belongings. Shifting ahead, we assumed the Inflation Discount Act’s (IRA) 15% minimal company tax charge and included accelerated depreciation and amortization (D&A) of unpolluted power belongings allowed by the act, leading to increased preliminary money circulation and improved mission economics.

QOE Capital – Analyst Madison Huang

Modifications in internet working capital had been projected as a proportion of income primarily based on historic traits. Capital Expenditures (CapEx) development was projected primarily based on historic CapEx-to-revenue ratios, stored fixed at round 2% for future projections. For the terminal worth calculation, we assumed a perpetual development charge of two%, justified by the optimistic trade outlook and ongoing power transition traits.

By way of our DCF mannequin, we derived a goal value of $197.49 per share, reflecting a 17.03% upside from the buying and selling value as of June 17, 2024. Our sensitivity evaluation explored implied share costs with low cost charges starting from 7.88% to 9.88% and perpetual development charges starting from 1% to three%, displaying majority upside potential throughout numerous situations.

QOE Capital – Analyst Madison Huang

Dangers

GEV is navigating turbulent waters in its offshore wind phase. The broader wind trade skilled declining EBITDA margins on account of rising uncooked materials prices, elevated transportation bills, provide chain disruptions, and stiff competitors from lower-cost Chinese language producers. Corporations within the sector, together with GEV, have been compelled to meet loss-making contracts signed earlier than the latest surge in prices, resulting in widespread monetary pressure throughout the trade. The hovering prices of uncooked supplies and transportation have turned a $4 billion backlog of unprofitable tasks into a big monetary burden. Whether or not or not they can obtain steerage to get by means of the backlog by 2025 remains to be up within the air, and this warrants some warning from buyers.

Authorities insurance policies and incentives are one other essential issue. GEV’s operations closely rely upon regulatory help and subsidies for renewable power tasks, making it inclined to coverage shifts. Modifications in tax credit beneath the Inflation Discount Act and the Infrastructure Funding and Jobs Act might impression profitability. Whereas these dangers are largely priced into the market, potential will increase in authorities help for renewable tasks might mitigate unfavourable results and supply a lift.

Conclusion

GE Vernova is navigating a difficult but promising panorama. Whereas the corporate stays in a restructuring part, there are important causes for investor optimism. The corporate’s strategic deal with margin enchancment and operational effectivity, mixed with a robust market place within the US and a considerable put in base, units the stage for future development. The Energy and Electrification segments are already driving profitability, and the Wind phase is poised to show round by 2025. Traders ought to think about holding GEV shares to capitalize on the long-term development potential, whereas preserving a vigilant eye out on market situations and the way the corporate’s steerage performs out. With its complete strategy to electrification and decarbonization, GE Vernova is well-positioned to steer within the international power transition and ship substantial worth to its shareholders.

{kind=link}