Adriana Duduleanu

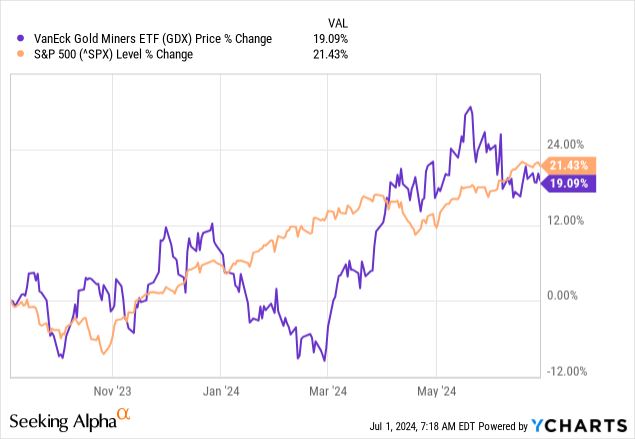

It has been about 10 months since I first coated VanEck Gold Miners ETF (NYSEARCA:GDX) and a bit greater than a month since I outlined my causes to be skeptical on the present market sentiment in the direction of the ETF.

Since my preliminary evaluation, the ETF has carried out largely in-line with the remainder of the fairness market, albeit with considerably increased volatility.

The graph above won’t look attractive, and the numerous swings within the GDX’s worth relative to the S&P 500 can also be a function that traders would rightfully see as a significant downside to the gold ETF.

There are, nevertheless, quite a few elements that we have to have in mind when evaluating the GDX efficiency.

Then we must always take a more in-depth take a look at the ETF’s high holdings pricing relative to their progress and margins. This could give us an concept of what we might count on from gold miners going ahead in an atmosphere the place equities are as soon as once more priced for perfection.

Dissecting Market Efficiency

The primary level that ought to be taken under consideration once we use the S&P 500 as a benchmark for efficiency is that the previous 12 months has been a relatively uncommon one.

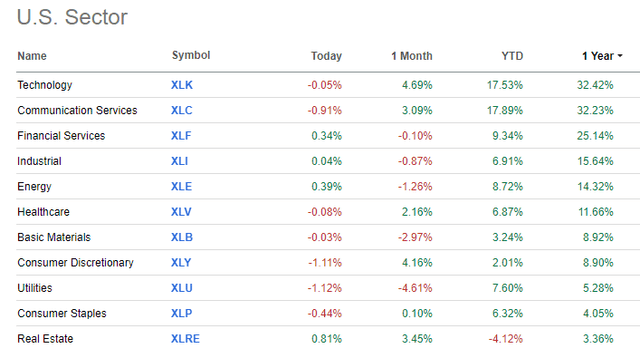

The fairness index has change into extraordinarily concentrated into a couple of know-how names in recent times and that is hardly ever a very good signal of a wholesome fairness market. Over the previous 12 months, we additionally noticed the hole between these know-how names and the remainder of the fairness market widening even additional.

As we see on the graph under, apart from Monetary Companies (XLF) all different sectors have returned lower than half of the highest two sector ETFs – Expertise (XLK) and Communication Companies (XLC).

In search of Alpha

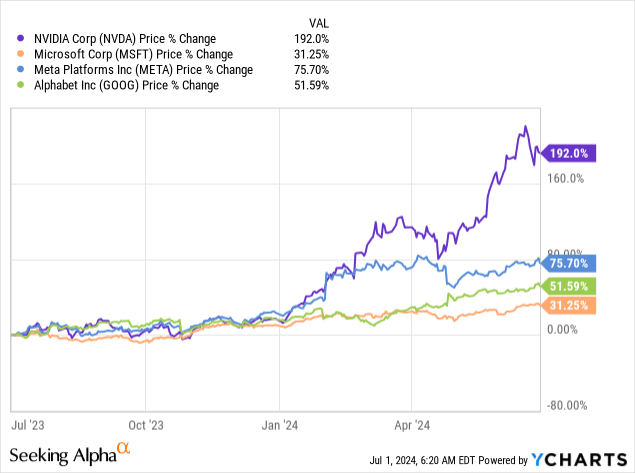

In fact, the rationale for this divergence between the XLK and XLC and the remainder of the sector ETFs is the focus of those two ETFs. Greater than 40% of the burden of the XLK is comprised of Nvidia (NVDA) and Microsoft (MSFT) and the identical is true for XLC with Meta (META) and Alphabet (GOOGL) (GOOG) shares.

The returns of those 4 shares have been nothing in need of spectacular over the previous 12 months, with NVDA almost tripling in worth in a matter of simply 12 months.

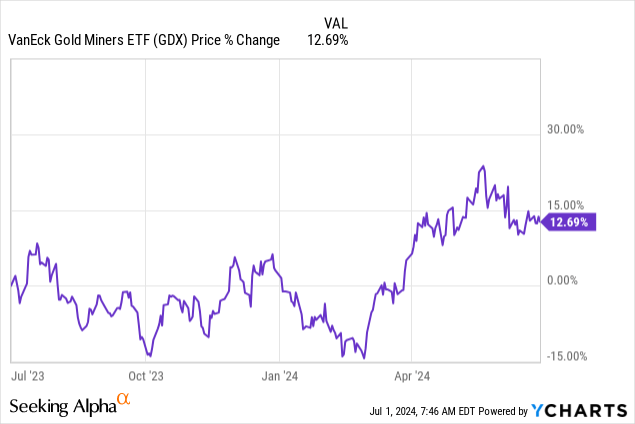

Thus, as soon as we account for these extraordinary actions of simply 4 shares, the almost 13% return of the GDX over the previous 12 months is likely one of the highest on a sector foundation.

Extra importantly, the prospects of the GDX now seem more and more beneficial over the approaching 12 months as traders went all-in on know-how shares and will simply be inflicting vital imbalances within the fairness market.

Nearer Look At Multiples And Margins

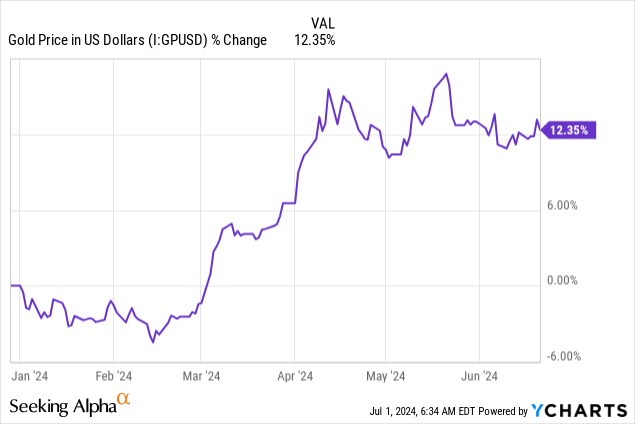

As a place to begin, the worth of gold is up by greater than 12% for the reason that starting of the 12 months and the long-term prospects of the dear metallic stay very enticing as free financial and monetary insurance policies are rising the danger for the prevailing financial regime.

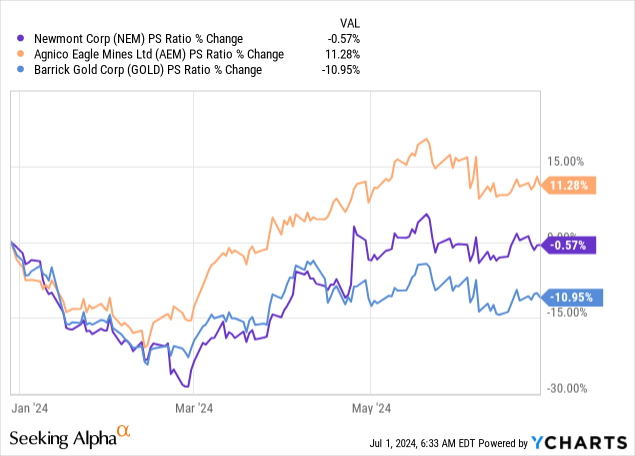

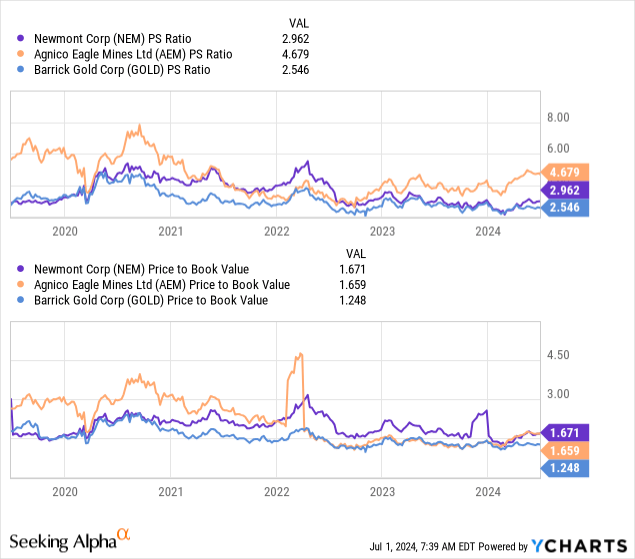

Within the meantime, the typical gross sales a number of of the top-3 holdings of GDX – Newmont (NEM), Agnico Eagle Mines (AEM) and Barrick Gold (GOLD), have remained comparatively flat for the previous six months.

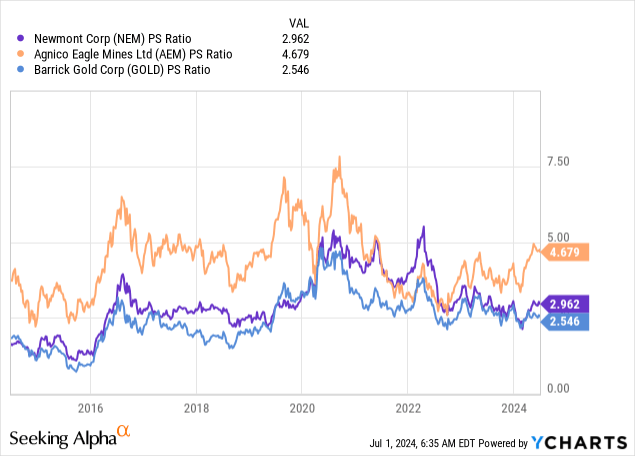

Zooming out a bit, and we might see that every of the three corporations commerce at a comparatively low gross sales a number of on a historic foundation. Extra importantly, every of the three trades at a big low cost to its respective a number of within the 2020-21 interval.

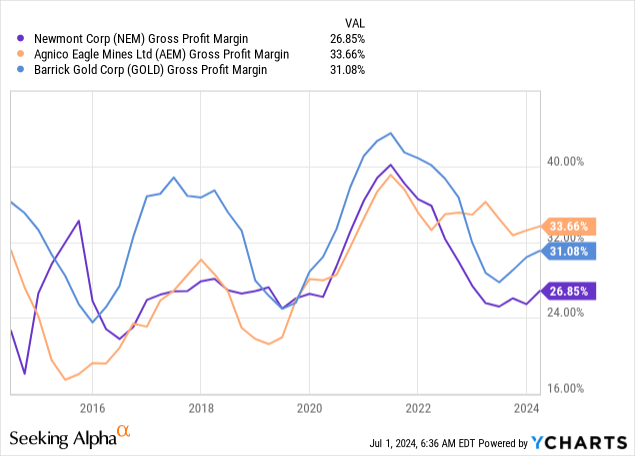

Then again, once we take a look at gross margins of those corporations, we might see that:

Firstly, they’ve someway improved over the previous 10-year interval; Secondly, they seem like at a cyclical low in the mean time and in-line with the gross sales multiples – approach under their 2020-21 highs.

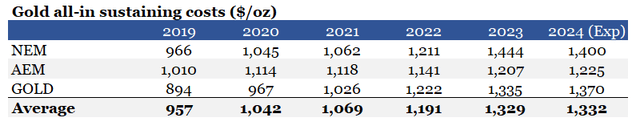

Nevertheless, in current quarters we see a notable uptick in margins, which if sustained, might imply a significant uptick in multiples of those three corporations. As a place to begin, we might see that all-in sustaining prices ($/oz) have elevated meaningfully in 2022-23, however primarily based on the steering supplied by every of the three corporations, are prone to stay flat in fiscal 12 months 2024 (observe that the place a steering vary was supplied I took the mid-point).

ready by the writer, utilizing information from Annual Reviews

Then, if we take the typical AISC of the three corporations in every of the intervals listed above and examine this to the typical worth of gold, we might see that in 2023 this ratio stood at 68% – approach increased than in 2020-21 interval. This distinction might clarify why multiples skyrocketed in 2020 and 2021 as prices have been considerably decrease than the worth of gold.

ready by the writer, utilizing information from Annual Reviews

Extra curiously, if every of the three corporations obtain its full fiscal 12 months 2024 steering on prices and the worth of gold stays at present ranges, it seems that the ratio would fall sharply to 60% – not materially totally different than the values we noticed in 2020-21.

On the similar time, each gross sales and e book worth of fairness multiples are nonetheless a lot decrease than they have been in the course of the aforementioned interval.

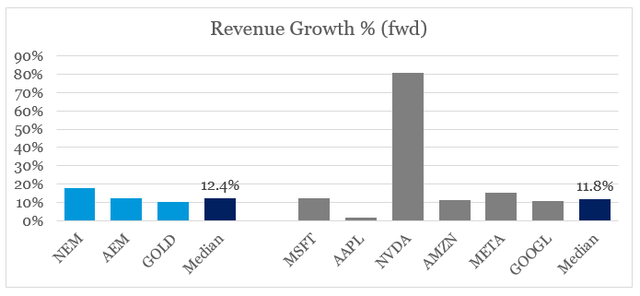

All that units the stage for a number of repricing of those corporations via the remainder of 2024, if initially supplied steering on AISC stays unchanged. However that is not the one factor that makes GDX enticing. These three corporations are anticipated to develop their topline figures at a median charge of 12.4%. This might lead to a double whammy impact of upward a number of repricing on a a lot increased gross sales determine for every of the top-3 holdings of GDX. Lastly, the median ahead progress charge of the gold miners can also be increased than the median progress charge of the top-5 largest tech corporations throughout the S&P 500. This might simply lead to a gradual change in sentiment in the direction of gold mining shares relative to the tech giants.

ready by the writer, utilizing information from In search of Alpha

Conclusion

Regardless of underperforming the S&P 500 on a risk-adjusted foundation in current months, GDX’s efficiency is passable given the relatively uncommon and imbalanced efficiency of tech shares. Extra importantly, nevertheless, the ETF’s top-3 holdings stay extremely enticing and their share costs might expertise a double whammy impact over the approaching months.

:max_bytes(150000):strip_icc()/NewsImages-PackageonWhatToExpect3-final-04daeaf95d3a4dc7972aa4591eb982a6.png)

{kind=link}