Imgorthand/E+ by way of Getty Photos

The perfect factor that occurs to us is when an excellent firm will get into momentary hassle… We need to purchase them after they’re on the working desk. – Warren Buffett

Geberit (OTCPK:GBERY) is a nice firm that’s experiencing what we imagine to be momentary headwinds. It’s a main supplier of loo and plumbing options, with a really robust model that may be a key aggressive benefit. The corporate has constructed a repute for producing high-quality, dependable, sustainable, and revolutionary merchandise.

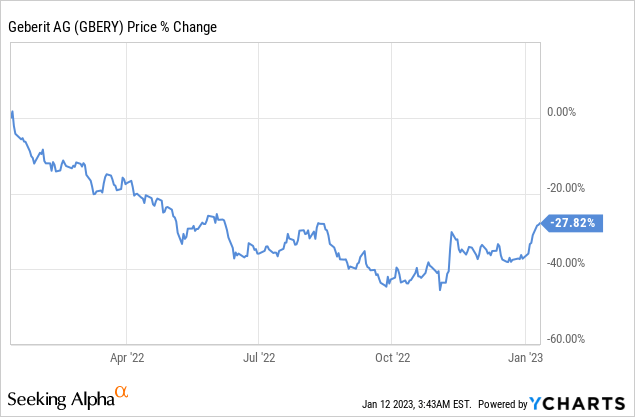

On account of the headwinds the corporate is experiencing, its shares have misplaced ~27% prior to now 12 months, nevertheless it appears like they’re beginning to get well.

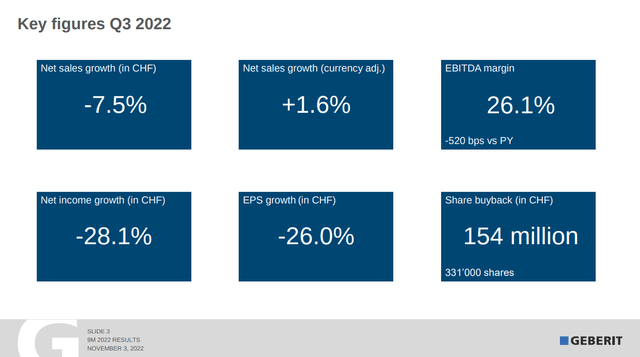

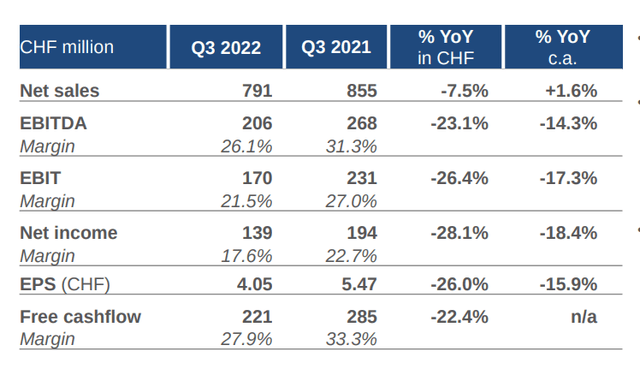

Headwinds embrace the rising rates of interest atmosphere that’s cooling-off the development market, and abnormally excessive vitality costs which can be affecting margins. As could be seen within the slide beneath that shares the corporate’s key figures for Q3 2022, internet gross sales progress was destructive 7.5% in Swiss Francs, and 1.6% in fixed foreign money. Consequently, earnings per share within the quarter declined an enormous 26%.

Geberit Investor Presentation

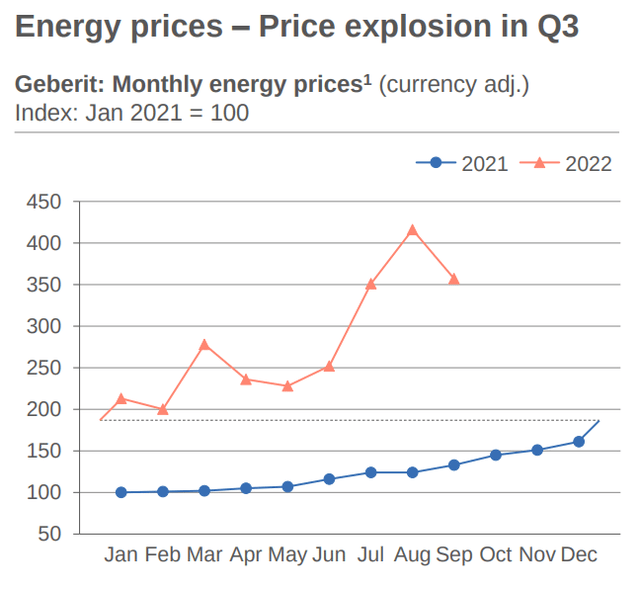

The corporate was considerably impacted by vitality costs, which ‘exploded’ in Q3 from already very elevated ranges. Geberit consumes vital vitality in its productions course of, and in consequence this has had a really destructive affect on its revenue margins.

Geberit Investor Presentation

Financials

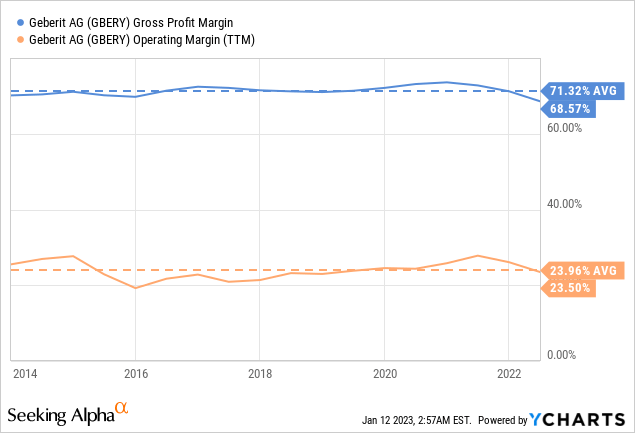

Traditionally, Geberit has had very excessive and steady revenue margins, with its working margin averaging ~23% over the previous ten years.

In the latest quarter, nevertheless, Geberit reported a major lower in its revenue margins attributable to destructive volumes progress and the extraordinarily excessive vitality costs. Regardless of this lower, the corporate stays solidly worthwhile and continues to generate vital free money circulation.

Geberit Investor Presentation

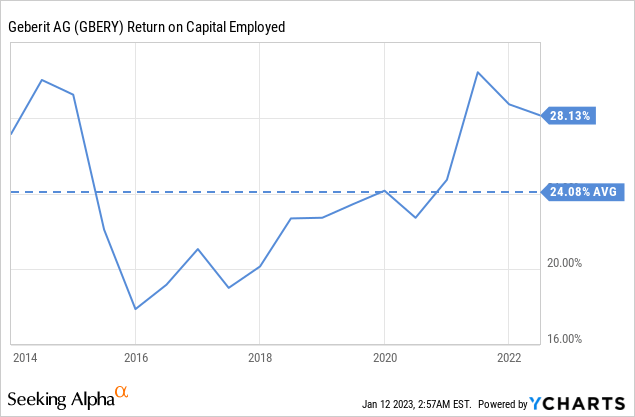

Yet one more fascinating statistic that displays the standard of the enterprise is its ten-year common return on capital employed of ~24%, which is extraordinarily excessive and permits the corporate to compound retained earnings in a really vital approach.

Development

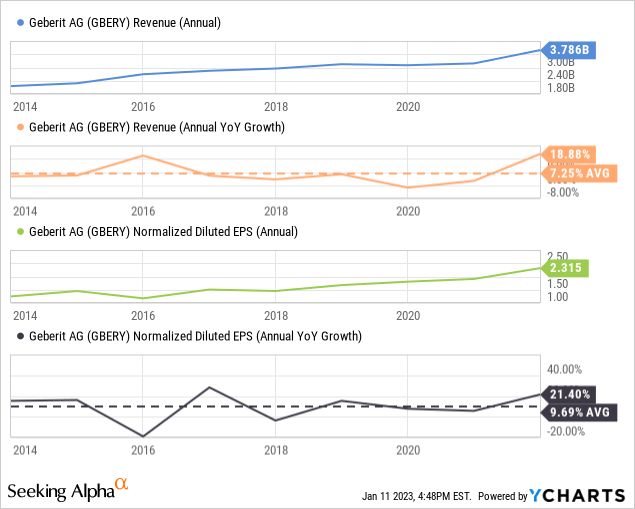

Income has grown meaningfully prior to now ten years, however this progress has been very cyclical. The common annual 12 months over 12 months income progress has been roughly 7%, whereas earnings have elevated at a barely extra fast tempo of ~9.6%. This isn’t a hyper-growth firm clearly, however these are very stable numbers, and we imagine this degree of progress could be very sustainable.

Stability Sheet

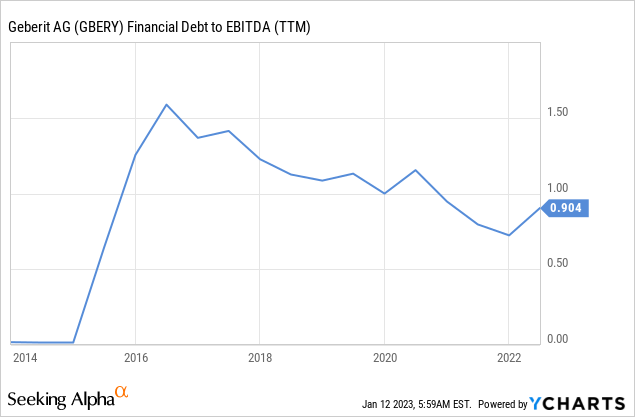

Whereas the Geberit Group’s monetary state of affairs stays very stable, the decrease free cash-flow era and elevated velocity of their share buyback program led to a deliberate enhance in internet debt to 831 million Swiss Franc on the finish of the latest quarter. The corporate’s monetary debt to EBITDA stays at a really affordable degree.

ESG

One other energy of Geberit is its dedication to sustainability and vitality effectivity. The corporate gives a spread of merchandise which can be designed to preserve water and vitality, which helps to scale back the environmental affect of its merchandise. Geberit has repeatedly been awarded the very best ranking of the EcoVadis platform for its sustainability administration, and has a low-risk ranking on Sustainalytics as nicely.

Geberit

Valuation

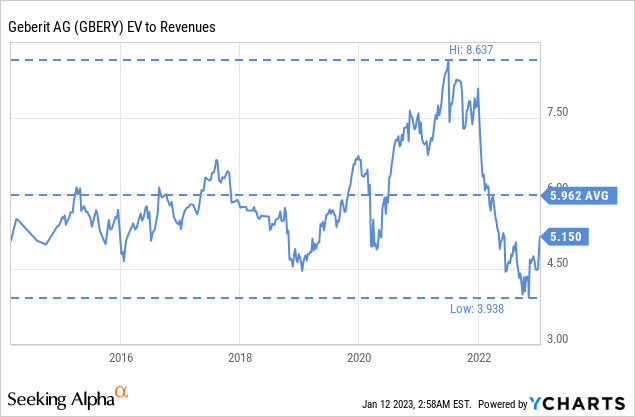

Prior to now ten 12 months shopping for shares round a 4.5x EV/Revenues a number of has labored out nicely for traders. Shares had been at these ranges not too long ago, and are at present simply barely larger. We imagine present costs, whereas barely much less enticing than a number of months in the past, nonetheless supply a superb shopping for alternative. It’s price noting that Geberit shares often commerce at a excessive valuation, and shopping for alternatives are uncommon.

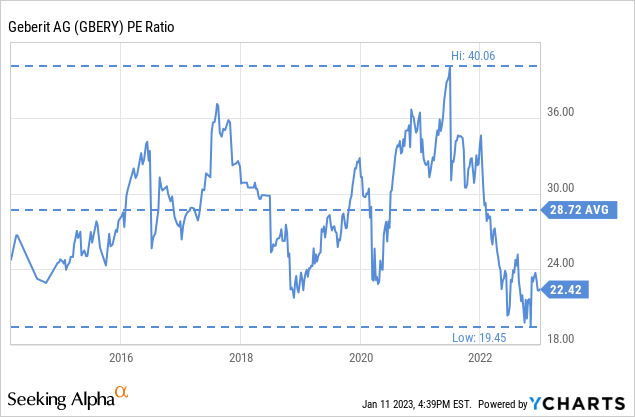

The ten-year common value/earnings ratio is ~28x, however at present shares could be bought round a 22x a number of.

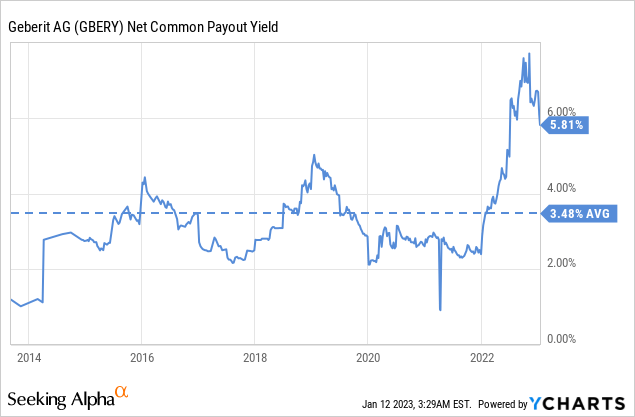

The web widespread payout yield, which mixes the dividend yield and the buyback yield, is at present fairly excessive at ~5.8%. That is considerably larger than the ten-year common. It seems that the corporate believes it is a nice time to purchase again shares, which is another excuse why we imagine present costs to be a chance.

Dangers

The primary dangers the corporate is at present dealing with are macroeconomic uncertainty ensuing from excessive inflation and a rising rate of interest atmosphere that’s cooling-off the development business. The corporate can also be dealing with extraordinarily excessive vitality prices which can be weakening its revenue margins. Regardless of these headwinds, the corporate has thus far been in a position to stay worthwhile, however there’s a danger that the state of affairs may worsen.

Conclusion

Geberit is a superb firm that’s at present experiencing momentary headwinds attributable to rising rates of interest, a cooling-off building market, and abnormally excessive vitality costs. This has negatively impacted internet gross sales progress and earnings per share. Regardless of these challenges, the corporate stays worthwhile and continues to generate vital free money circulation. Nonetheless, there are dangers to contemplate, together with vital macroeconomic uncertainty. Whereas the corporate’s shares have misplaced ~27% prior to now 12 months, they look like recovering, and we imagine present costs supply a uncommon shopping for alternative. We’re subsequently beginning protection with a ‘Purchase’ ranking.

Editor’s Be aware: This text discusses a number of securities that don’t commerce on a serious U.S. alternate. Please concentrate on the dangers related to these shares.

{kind=link}