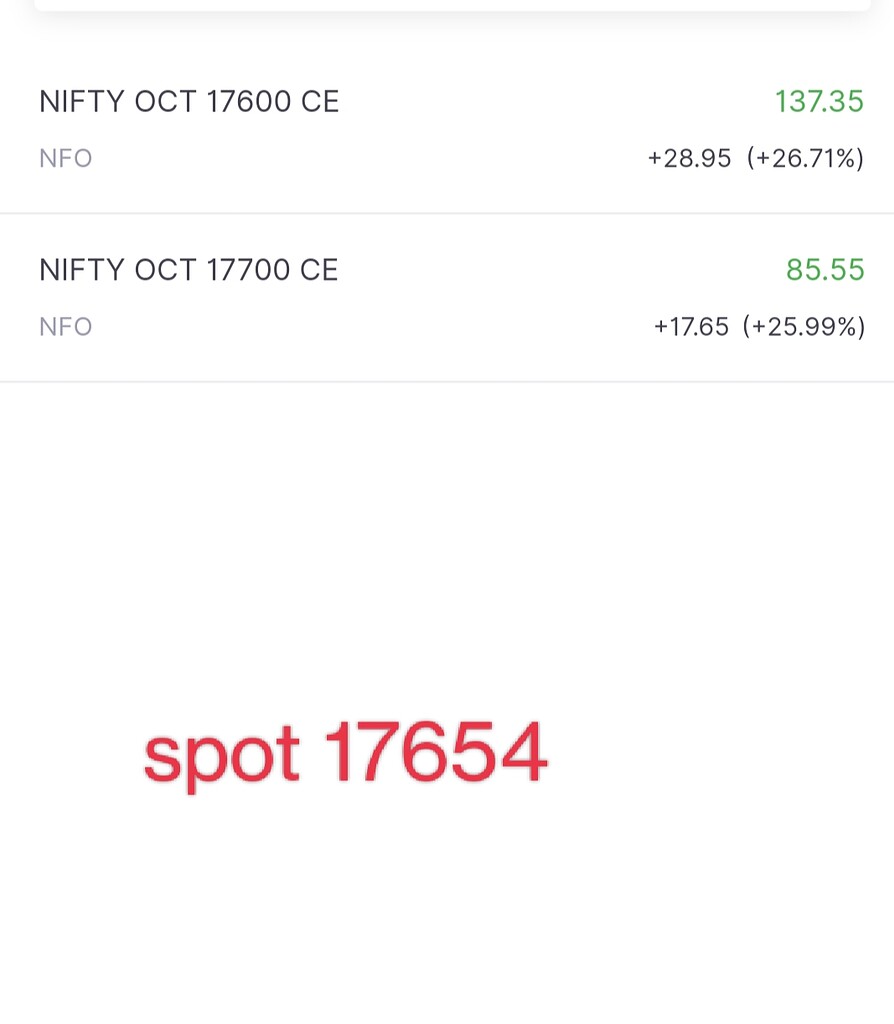

This query is when nifty is round 12:19 pm date 20 oct the spot is round 17654.

Ques – The premium calculation relies on delta my understanding right here is the deeper the itm the higher the delta that means motion compared to spit is larger on the premiums.Nevertheless right here i see that 17700 is deeper itm than 17600 nonetheless proportion change is larger for 17600 how can this be attainable as delta can be larger for 17700

In all probability i’m skipping one thing right here please help make it clear

Thanks

Hy @Animiesh

If Spot is at 17654 then 17700 CE turns into OTM(Out of the Cash). There are different elements as properly like Theta(Time Decay) and likewise verify for IV(Implied Volatility).

Animiesh:

17700 is deeper itm than 17600

Since spot is under strike value, 17700ce is OTM and 17600ce is ITM. So delta of 17600ce ought to be larger.

1 Like

thanks for sharingso my understanding on how the strike value strikes per delta is appropriate proper it’s simply that right here i’m evaluating the itm to otm that’s the reason there’s a distinction

{kind=link}