Printed on October twenty fourth, 2022 by Samuel Smith

Actual Property Funding Trusts (i.e., “REITs”) are tax-advantaged revenue automobiles which have turn into more and more well-liked with buyers and establishments lately. The explanation for that is that they don’t have to pay any revenue tax on the company degree, however as an alternative function cross by way of entities.

In trade for this profit, they’re required to satisfy sure tips, together with paying out no less than 90% of taxable revenue to shareholders within the type of dividends. Consequently, excessive yield and dividend progress buyers usually love REITs and dedicate a substantial portion of their portfolios to them.

You possibly can obtain your free 200+ REIT listing (together with essential monetary metrics like dividend yields and payout ratios) by clicking on the hyperlink under:

Definitely, excessive dividend REITs are engaging for dividend buyers on the lookout for revenue proper now.

Nevertheless, not all REITs are excessive yielding and in reality, a few of them boast spectacular progress observe information. This makes them a better of each worlds sort funding, the place buyers can take pleasure in a quickly rising dividend alongside excessive capital appreciation potential.

On this article, we’ll take a look at seven REITs which have strong progress potential for the foreseeable future.

Desk of Contents

#1. Progressive Industrial Properties Inc. (IIPR)

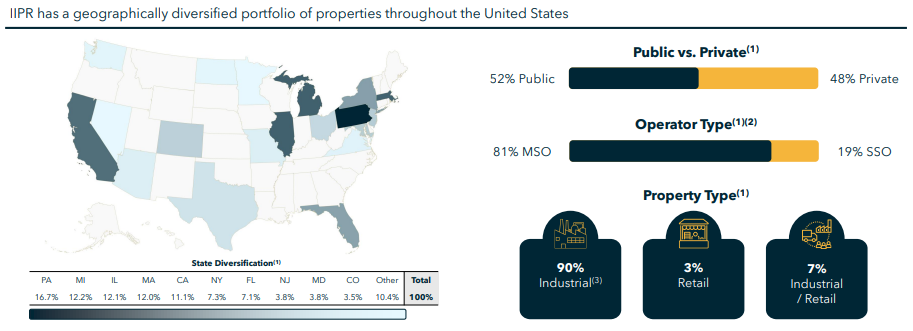

IIPR focuses on proudly owning marijuana cultivation and manufacturing properties, the place it offers essential entry to capital for marijuana companies.

Associated: 2022 Marijuana Shares Listing | The Greatest Marijuana Shares To Make investments In Now

IIPR advantages from being the only real publicly traded REIT of its type in america and has loved strong progress consequently. It at the moment owns nicely over 100 properties throughout 19 states.

Supply: Investor Presentation

Its enterprise mannequin is sort of profitable and offers engaging risk-adjusted returns because of the 15-20 preliminary lease phrases which can be 100% triple internet and usually include sturdy preliminary rental yields and annual escalations.

The REIT has a formidable progress observe document as its AFFO per share has soared from $0.67 in 2017 to $5.55 in 2021 and an anticipated AFFO per share tally of $8.00 in 2022. Its dividend has additionally grown quickly, growing from $0.55 in 2017 to $5.72 in 2021 and a present annualized payout price of $7.00 per share. NOI has elevated at a whopping 137% CAGR over this time interval whereas economies of scale have improved immensely as mirrored in its G&A as a proportion of NOI plummeting from 89% in 2017 to a mere 11.5% in 2021.

Shifting ahead, it continues to have an unbelievable progress profile, with the principle constraint being the authorized/regulatory surroundings. The authorized and regulatory uncertainties however, analysts are total nonetheless bullish on IIPR’s potential to proceed rising. They anticipate the REIT to develop dividends per share at a 6% CAGR by way of 2024 and FFO per share at a 9.6% CAGR over the identical time span. Nevertheless, if the regulatory surroundings improves quicker than anticipated, IIPR may doubtlessly ship a lot quicker progress than this already sturdy forecast.

#2. Rexford Industrial Realty, Inc. (REXR)

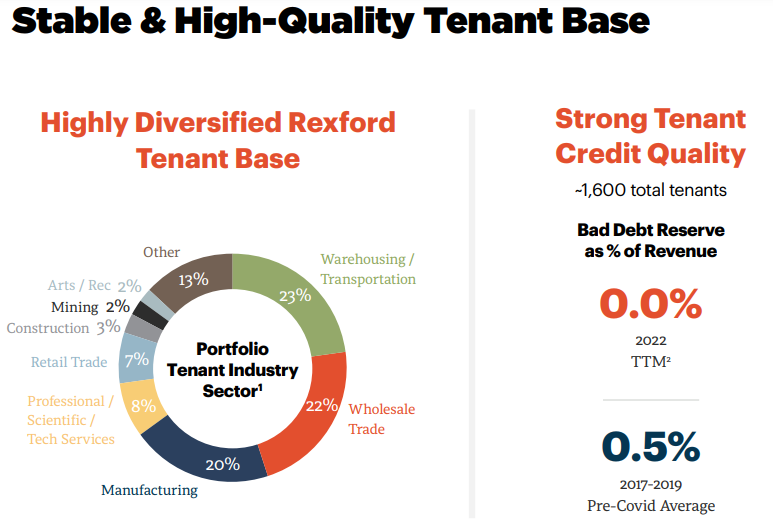

REXR focuses on proudly owning and working industrial properties positioned in Southern California. Its portfolio at the moment consists of almost 42 million sq. ft. The REIT was based in 2001 and has generated very sturdy progress lately. Since 2018 it has generated a 32% NOI CAGR and a 15% FFO per share CAGR. Since 2017, its dividend has grown at an 18% CAGR and since 2017 the REIT has generated a 15% whole return CAGR. Over the previous three years, it has posted a 32% consolidated NOI CAGR, a 22% FFO per share CAGR, and a 17% dividend per share CAGR.

Its Q3 numbers got here in very sturdy as nicely, with 98.6% portfolio occupancy, 40.1% consolidated NOI progress, 44.5% core FFO progress, and 16.3% FFO per share progress. In the meantime, its stability sheet stays in strong form, with about $1.2 billion in whole liquidity a BBB+ credit standing from S&P and a mere 15.9% internet debt to whole enterprise worth ratio.

Trying forward, analysts anticipate REXT to proceed producing sturdy progress numbers. Via 2026, analysts forecast a 13.2% AFFO per share CAGR, a 12.8% FFO per share CAGR, and a 15.5% dividend per share CAGR.

This bullish outlook is partly because of its nicely diversified and high-quality tenant base that ought to result in decrease draw back threat and quite a few progress alternatives.

Supply: Investor Presentation

On high of that, REXR additionally implements a value-add strategy to its asset administration so as to drive superior leasing spreads. Final, however not least, REXR advantages from its singular concentrate on the most important U.S. industrial market and the fourth largest total industrial market on the planet as Southern California has the most important ports within the nation, representing 40% of all U.S. containerized imports.

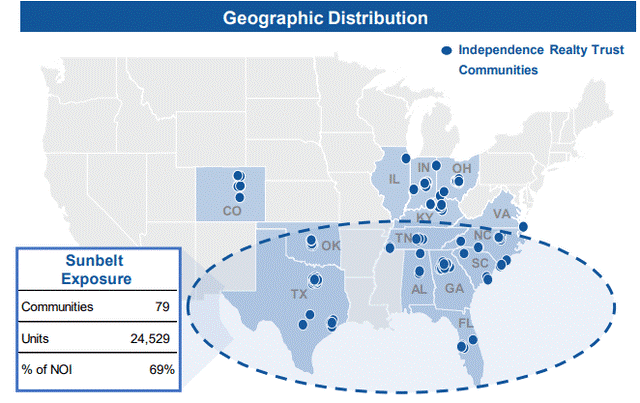

#3. Independence Realty Belief, Inc. (IRT)

IIRT focuses on multifamily condo communities in sunbelt markets. Whereas the REIT was affected by its decrease high quality asset portfolio and better leverage in its early years after going public in 2013, administration has since then remodeled the enterprise. It has acquired quite a few increased high quality condo communities, considerably deleveraged the stability sheet, and included value-add operations to its software equipment so as to increase returns on funding.

Supply: Investor Presentation

Whereas its previous observe document has been lower than stellar with FFO per share solely enhancing to $0.84 in 2021 relative to its $0.81 quantity in 2013, the ahead outlook for the enterprise is significantly better. FFO and AFFO per share are anticipated to develop at a ten% CAGR by way of 2026 whereas dividends per share are anticipated to extend at an 11% CAGR over that very same interval.

This sturdy progress will seemingly be fueled by IRT’s mixture of considerable retained money flows, sturdy same-store NOI progress price, and worth add enterprise, making it one of the crucial intriguing multifamily funding alternatives in the meanwhile.

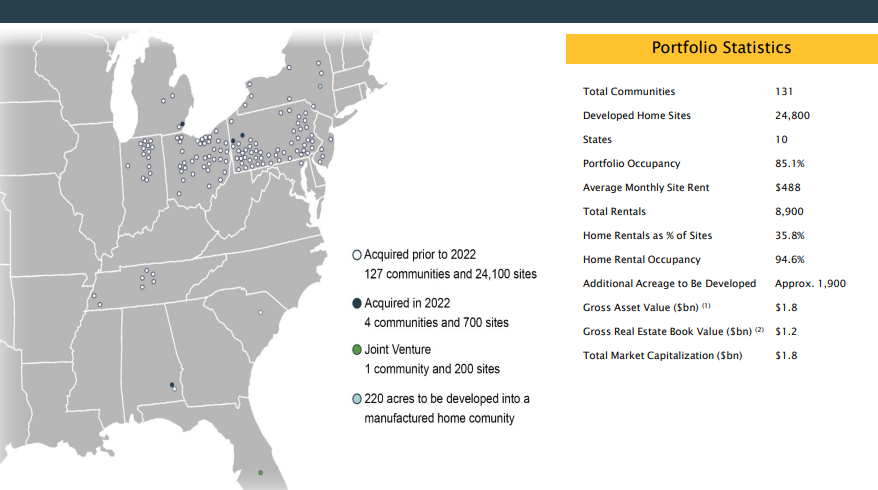

#4. UMH Properties, Inc. (UMH)

UMH focuses on proudly owning manufactured housing communities throughout america and at the moment owns tens of 1000’s of properties in over 100 communities within the Midwest and Northeast. ‘

Supply: Investor Presentation

For a few years UMH struggled to develop its dividend and FFO per share, with FFO per share growing solely barely on an annualized foundation from 2012 to 2019 (from $0.62 per share in 2012 to $0.63 per share in 2019). Moreover, the annualized dividend per share remained flat at $0.72 the complete time and was usually not coated absolutely by money flows over that interval.

Nevertheless, since 2020 the corporate’s progress engine has lastly kicked into excessive gear. FFO per share elevated from $0.63 in 2019 to $0.87 in 2021 and the dividend per share lastly started to develop together with it. In 2021, UMH paid out $0.76 per share in dividends and is at the moment paying out a $0.80 annualized dividend.

Shifting ahead, this strong progress momentum is anticipated to proceed. Wall Road analysts mission FFO per share to develop at a 23.3% CAGR by way of 2024, AFFO per share to develop at a 20.4% CAGR, and the dividend per share to develop at a ~5% CAGR. Whereas the dividend per share progress may definitely be increased than what it’s projected to be, UMH is anticipated to retain extra capital so as to gasoline additional profitable progress investments. What this does imply, nonetheless, is that UMH’s mid-single digit dividend CAGR will seemingly be sustainable for a long-time to return and the speed of progress might even speed up.

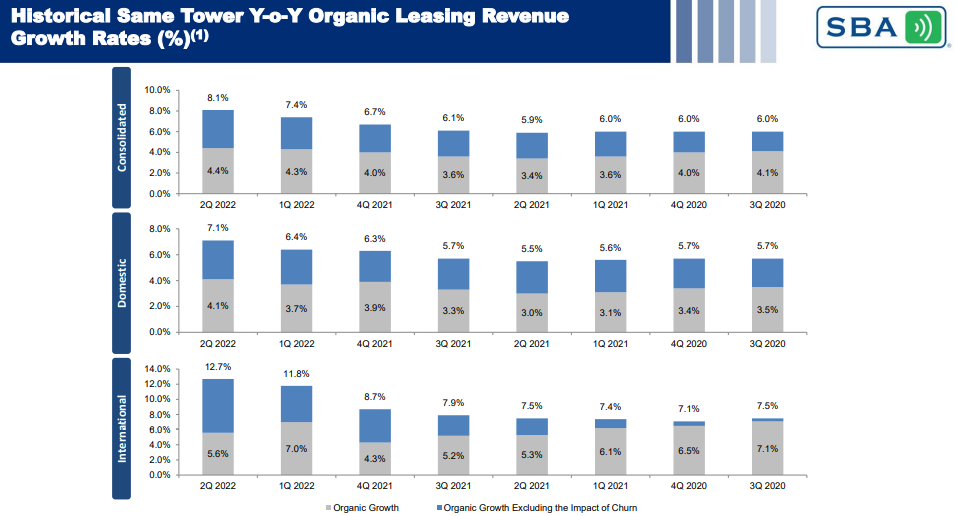

#5. SBA Communications Company (SBAC)

SBAC owns and operates wi-fi communications infrastructure similar to tower constructions for wi-fi antennas. In truth, it owns over 36,000 of those towers which it then leases out to wi-fi telecommunications firms.

The REIT has generated spectacular progress previously and has in actual fact seen it speed up in current quarters because the graphic under illustrates:

Supply: Investor Presentation

In 2012, SBAC generated $3.09 in AFFO per share and didn’t pay a dividend. In 2021, it generated $10.74 per share in AFFO and paid out $2.32 in dividends per share. This 12 months the REIT is anticipated to generate $12.06 in AFFO per share whereas paying out $2.84 per share in dividends.

Shifting ahead, SBAC is anticipated to proceed its unbelievable progress momentum. Dividends per share are anticipated to develop at a 21.1% CAGR by way of 2026 whereas AFFO per share is anticipated to develop at an 11.2% CAGR over the identical time interval. Consequently, SBAC is among the most tasty progress REITs out there immediately.

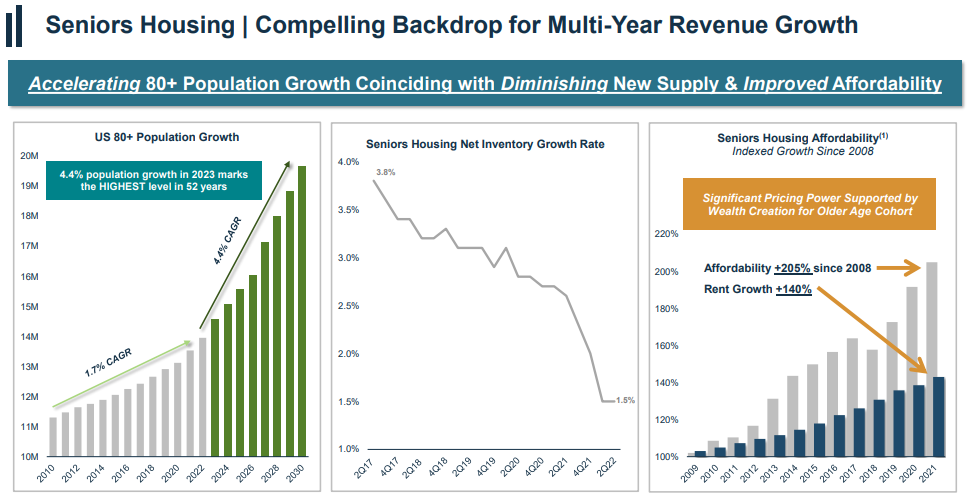

#6. Welltower Inc. (WELL)

WELL is a healthcare REIT that focuses on Senior Housing Operations, Senior Housing Triple-net, Outpatient Medical, Well being System, and Lengthy-Time period/Submit-Acute Care. Its revenue is pretty nicely diversified throughout these segments, with its 2021 internet working revenue damaged down as following: 39.3% in Seniors Housing Working (“SHO”), 23.5% in Seniors Housing Triple-net, 23.2% in Outpatient Medical (“OM”), 8.8% in Well being System, and 5.2% in Lengthy-Time period / Submit-Acute Care.

WELL’s observe document over the previous decade is lower than spectacular provided that its FFO per share and dividend per share have really declined barely over that interval. In 2012, FFO per share was $3.52 and dividends per share have been $2.96. In 2021, FFO per share was $3.21 and dividend per share have been $2.44.

Nevertheless, transferring ahead, analysts anticipate WELL’s progress trajectory to select up significantly, making it a compelling progress story. Via 2026 WELL is anticipated to develop its dividend per share at a 12% CAGR, its FFO per share at an 11.6% CAGR, and its AFFO per share at a 13.2% CAGR.

The elements behind this progress are the truth that the U.S. 80+ 12 months outdated inhabitants is anticipated to see its annualized progress price improve from 1.7% over the previous decade to 4.4% within the coming decade. The senior housing internet stock progress price has plummeted lately from 3.8% in 2017 to 1.5% this 12 months.

In the meantime, the huge buildup in house owner fairness and inventory market returns over the previous a number of a long time implies that aged people trying to extra to senior housing can far more simply afford it.

Supply: Investor Presentation

Consequently, administration expects its occupancy price and its pricing energy to soar within the coming years, boosting money flows and dividend progress together with it.

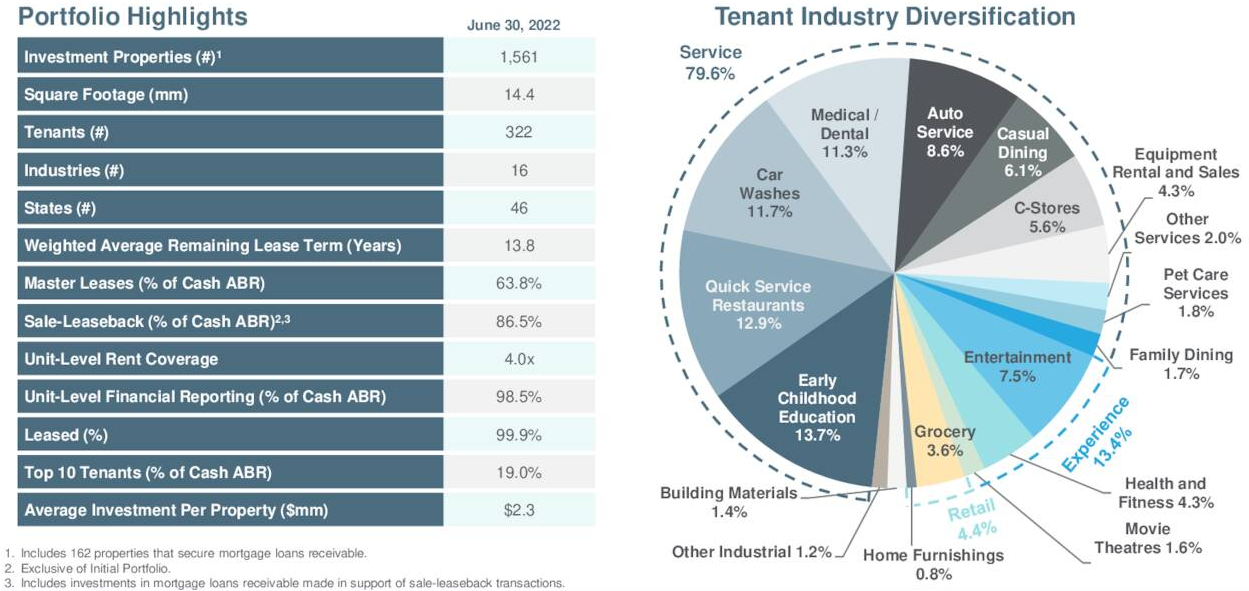

#7. Important Properties Belief (EPRT)

EPRT is a triple internet lease REIT with focuses on single-tenant properties leased out to center market firms that function service-oriented or experience-based companies similar to eating places, automobile washes, automotive and medical providers, comfort shops, health facilities, and early childhood schooling. It has a well-diversified portfolio of over 1,500 properties unfold throughout 16 industries.

One in every of its greatest focuses is to buy properties that may simply be repurposed and launched to a distinct tenant within the occasion that considered one of its current tenants defaults on their lease. Consequently, its enterprise mannequin is sort of low threat, particularly when mixed with its triple internet lease construction.

Supply: Investor Presentation

EPRT went public just lately (2018) however has already compiled a formidable observe document for producing strong progress alongside paying out a gorgeous dividend. In 2018, EPRT generated $0.78 in AFFO per share and paid out $0.43 in dividends per share. In 2021, it generated $1.34 in AFFO per share and paid out $0.98 in dividends per share. This 12 months, EPRT is anticipated to proceed its spectacular progress momentum by producing $1.53 in AFFO per share whereas paying out $1.08 in in dividends per share.

Via 2026, it’s anticipated to generate a ~6% AFFO per share CAGR alongside a dividend per share CAGR of ~5%. Whereas these numbers are usually not fairly as spectacular as among the others on this listing, its recession resistance, predictable and scalable progress technique, and present dividend yield of over 5.5% make it a compelling dividend progress REIT.

Conclusion

Whereas REITs are usually not usually identified – nor bought – for his or her progress however somewhat as passive revenue machines, there are exceptions on the market. One of many beauties of shopping for excessive progress REITs like those mentioned on this article is that buyers can obtain large tax-advantaged compounding. Since REITs don’t pay company revenue taxes, taxes are solely paid by buyers on the dividends that they obtain.

Consequently, high-growth REITs that retain a substantial proportion of money flows and might reinvest it at excessive returns get an added increase since continued progress in revenue on the REIT degree is tax free.

At a time when many growth-oriented investments just like the REITs shared on this article have been crushed down by rising rates of interest, now could possibly be time to spend money on these thrilling wealth compounders and dividend progress machines.

Positive Dividend maintains comparable databases on the next helpful universes of shares:

Thanks for studying this text. Please ship any suggestions, corrections, or inquiries to [email protected]

/gettyimages-591404039-c297fce7598946ba9fcccdf2414277db.jpg)

{kind=link}