peshkov

MoneyLion (NYSE:ML) simply accomplished a banner yr with the corporate almost doubling whole prospects whereas the inventory trades close to the lows under $1. The previous SPAC seems within the penalty field for no logical motive. My funding thesis stays extremely Bullish on the fintech set to maintain adjusted EBITDA earnings in 2023.

Supply: Finviz

Sturdy Finish to 2022

MoneyLion reported that This fall’22 adjusted revenues jumped 71% to achieve $92.4 million. The corporate ended the yr with document revenues and closed out the yr with an adjusted EBITDA revenue through the month of December.

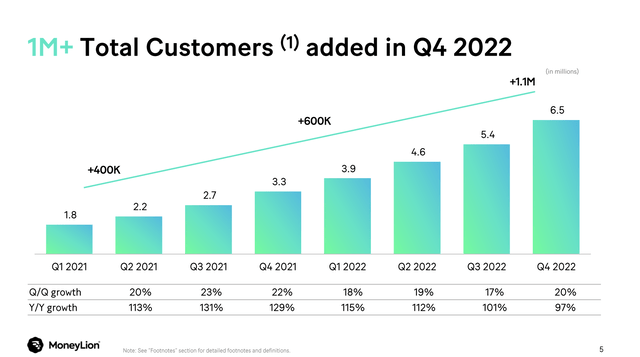

The fintech added a really spectacular 1.1 million prospects throughout This fall, almost double from the 600k added This fall’21. MoneyLion even added 1.6 million merchandise through the quarter to achieve 12.9 million merchandise in an indication of how current prospects are leveraging further merchandise from the net platform.

Supply: MoneyLion This fall’22 presentation

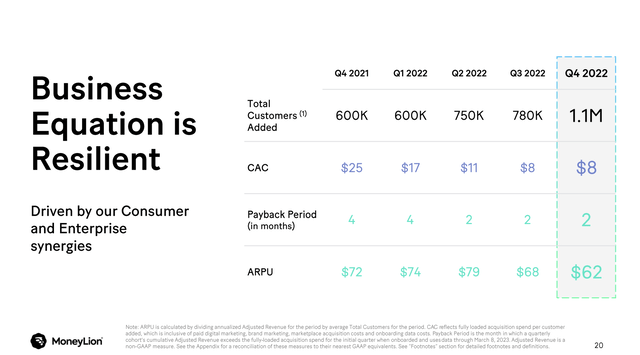

The corporate now has a robust Tremendous App ecosystem the place new buyer acquisition prices are as little as $8 now. The enterprise ecosystem is absolutely useful with tons of monetizable moments from auto or dwelling loans to insurance coverage and tax preparation.

Supply: MoneyLion This fall’22 presentation

MoneyLion added an incredible 1.1 million prospects in This fall’22 at a value of simply $9 million in advertising and marketing bills. These new prospects now have a minimal payback interval of solely 2 months because the fintech really minimize advertising and marketing spend throughout 2022 by 14%.

The CAC is down considerably from a nonetheless very acceptable $25 again in This fall’21 when the payback interval was a nonetheless sturdy 4 months. MoneyLion has seen the ARPU dip, however the profitability of the corporate has improved with the CAC down $18 per person whereas solely dropping out on $10 in ARPU. Because of the increased stage of recent prospects in This fall, the corporate really expects ARPU to rebound in future years as these new prospects mature.

The enterprise phase even struggled through the finish of 2H’22 because of the macro weak spot as companions pulled again from their advertising and marketing spend. MoneyLion solely reported This fall’22 enterprise revenues of $32.7 million, down from the $34.3 million stage in Q3’22.

Since MoneyLion supplies a digital monetary platform, largely utilizing banking companions, focused at low-income prospects, the corporate does not face the identical danger because the regional banks hit with fleeing uninsured deposits. The fintech is extra targeted on serving to customers with below-average credit enhance their monetary image through inner monetary choices and enterprise companions. These prospects do not sometimes have accounts with balances in extra of FDIC insurance coverage of $250,000.

SPAC Penalty Field

Contemplating the corporate’s outcomes, MoneyLion’s low inventory worth and market valuation of solely $160 million appear unwarranted, for my part. The corporate has as money steadiness of $154 million now to cushion any draw back danger.

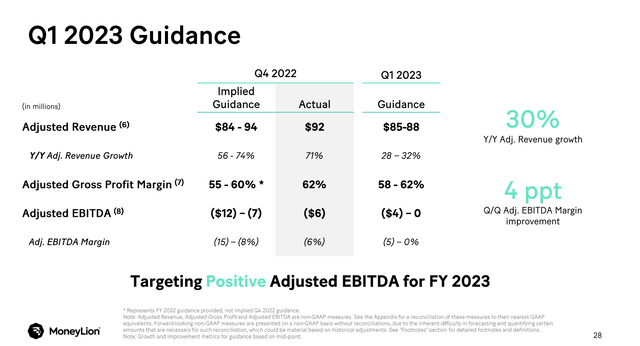

The corporate offered strong steering for Q1’23 with revenues guided for $85 to $88 million on this quarter. Whereas the goal is down from the booming This fall’22 income whole of $92 million, MoneyLion did simply soar previous the focused This fall midpoint of $89 million.

Supply: MoneyLion This fall’22 presentation

Most significantly, the flinch guided to being adjusted EBITDA constructive after burning substantial money to begin 2022. With the macro weak spot and the banking sector disaster, MoneyLion must be in a greater monetary place to protect the present money steadiness and keep away from any dilutive capital raises with the inventory buying and selling far under $1.

On the Investor Day again in December, the corporate guided to 35% to 50% CAGR. Merely utilizing a 35% income development goal for 2023 pushes revenues to a goal of $443 million. The inventory solely has a market cap of $160 million whereas revenues might prime $600 million in 2024 per the steering of administration.

Elevated Dangers

The market presumably does not just like the outcomes with the big $140 million goodwill impairment cost hiding the large adjusted EBITDA enhancements over the yr or presumably traders worry a reverse break up. Fellow fintech Paysafe (PSFE) accomplished a 1-for-12 reverse break up and the inventory promptly rallied, although Paysafe did initially dip heading into the break up.

Both means, MoneyLion would not commerce under $1, if elevated dangers did not exist. An upcoming recession might begin impacting low-income members resulting in the corporate failing to satisfy monetary targets.

The corporate has already minimize estimates previously and additional cuts to monetary targets would injury investor confidence in administration. In the end, the large danger to the inventory is continuous money burn charges resulting in very dilutive capital raises sooner or later all the time inherent in a inventory buying and selling under $1.

Takeaway

The important thing investor takeaway is that MoneyLion is not priced for the enhancing earnings story and the sturdy income development of the enterprise, in our view. The fintech trades far under 1x gross sales targets now and the corporate guided to being adjusted EBITDA worthwhile this yr with a chance of hitting constructive EBITDA in Q1.

The inventory positively has dangers highlighted by the value dipping under $1, however MoneyLion has constructed a powerful ecosystem and has loads of money to put money into the enterprise to reward shareholders. Our opinion is that traders ought to use the weak spot to purchase extra shares previous to the analyst neighborhood catching onto the story with solely 2 attending the This fall’22 earnings name.

Editor’s Notice: This text covers a number of microcap shares. Please pay attention to the dangers related to these shares.

:max_bytes(150000):strip_icc()/GettyImages-1282868177-b7ad0055c459422db19148e4e52a3798.jpg)

{kind=link}