blackdovfx/iStock through Getty Photos

John B. Sanfilippo & Son, Inc. (NASDAQ:JBSS) is a really nicely run branded meals firm. Managers are correctly incentivized to pursue shareholder pursuits, they usually have achieved so, rising the agency’s financial profitability, producing rising free money flows, and bettering the corporate’s capital effectivity. Nonetheless, evaluation reveals that the corporate is barely overvalued, lacking out on a purchase suggestion from me.

The Enterprise Mannequin

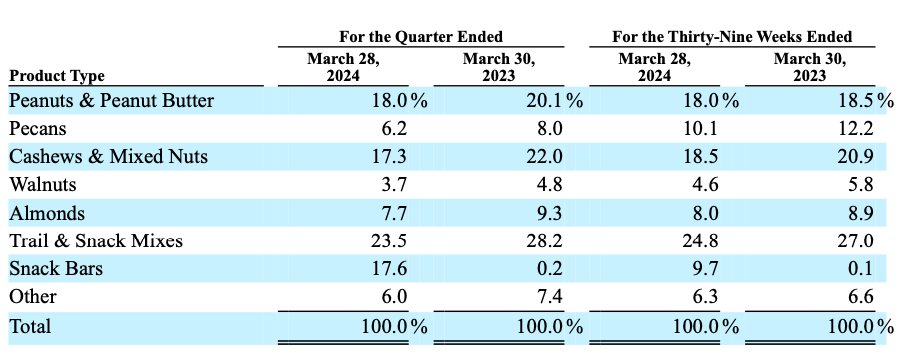

Sanfilippo is a number one processor and distributor of peanuts, pecans, cashews, walnuts, almonds and different nuts in america. These nuts are packaged below the corporate’s Fisher, Orchard Valley Harvest, Squirrel Model and Southern Fashion Nuts manufacturers and below personal manufacturers as nicely. The corporate additionally manufactures, processes, markets and distributes a variety of meals and snack merchandise, comparable to peanut butter, almond butter, cashew butter, sweet and confections, snack and path mixes, diet bars, snack bites, sunflower kernels, dried fruit, corn snacks, chickpea snacks, sesame sticks and different sesame snack merchandise below its personal model names and below personal manufacturers. As well as, since its acquisition of the Simply the Cheese model, it now additionally affords baked cheese snack merchandise below its personal and personal label manufacturers. As of the third quarter fiscal 2024 report, path and snack mixes had been the corporate’s most essential product by income, adopted by peanuts and peanut butter and snack bars and cashew and combined nuts.

Supply: 3Q 2024 Report

The corporate has three major distribution channels: the buyer, shopper ingredient customers and contract packaging prospects channels. The buyer channel is well an important channel for the corporate, contributing 83.1% of revenues as of the third quarter of the fiscal 12 months.

Supply: 3Q 2024 Report

The buyer market comes with clear advantages: profitable manufacturers flip one thing that’s undifferentiable, peanuts, into one thing that’s differentiable and offers the corporate pricing energy. Pricing energy provides Sanfilippo a platform to enhance NOPAT margins and shield itself towards inflationary pressures from rising gold costs.

Govt Compensation Aligns Administration and Shareholder Incentives

Agent-principal conflicts are rife within the inventory markets. These conflicts come up the place govt compensation doesn’t incentivize administration to work within the pursuits of its shareholders. Shareholder pursuits are superior when financial revenue is created. We all know that financial revenue is outlined as:

Financial Revenue = Return on invested capital (ROIC) – Price of Capital (WACC).

That is mathematically equal to:

Financial Revenue = Internet Working Revenue After Tax (NOPAT) – Capital Cost

…the place capital cost is the same as weighted common value of capital instances invested capital.

Sanfilippo’s Worth Added Plan (SVA Plan), which is 30% to 40% of complete compensation, efficiently aligns administration’s pursuits with these of shareholders. Administration is given a money fee primarily based on the next method:

Participant’s Wage = Participant’s Goal Wage Proportion x SVA Enchancment A number of = SVA Cost Declared

In line with Sanfilippo’s 2023 Proxy Assertion:

“The SVA Plan rewards plan individuals with money incentive compensation for year-over-year enchancment in financial revenue. Financial revenue is our internet working revenue, as adjusted for share primarily based compensation and internet rental and miscellaneous expense, after taxes minus a cost for capital. The cost for capital is set by multiplying the weighted common value of capital (9%) by the invested capital within the enterprise (adjusted internet working capital plus internet property, plant, and gear and goodwill), excluding any extra money and money equivalents in extra of $2 million (such year-over-year enchancment hereinafter known as “SVA”), as illustrated under:

SVA = NOPAT – 9% Capital Cost.”

Development With Profitability

Since 2020, Sanfilippo has grown revenues from $880.09 million to $1.03 billion, compounding at 3.22% a 12 months. In that point, Sanfilippo’s NOPAT has grown from $54.83 million in 2020 to $67 million within the trailing twelve months (TTM), compounding at 4.1% a 12 months. To be clear, that is my measure of its NOPAT, which I derived by stripping away the impression of non-operating and non-recurring objects, within the method proven under:

Worth in hundreds of thousands

2020

2021

2022

2023

TTM

GAAP Internet Revenue

$54.11

$59.74

$61.79

$62.86

$64.91

Complete Internet Non-Working Expense Hidden in Working Earnings

$ (3.77)

$ (5.02)

$ (3.42)

$ (1.37)

$ (1.39)

Reported Internet Non-Working Objects

$5.84

$5.36

$3.39

$4.87

$4.39

Change in Complete Reserves

$ –

$ –

$ –

$ –

$ –

Implied Curiosity for Standardized of Working & Variable Leases

$0.19

$0.15

$0.10

$0.29

$0.33

Non-Working Tax Adjustment

$ (1.54)

$ (1.39)

$ (1.43)

$ (1.66)

$ (1.20)

Internet After-Tax Non-Working Expense/(Revenue)

$ –

$ –

$ –

$ –

$ –

NOPAT

$54.83

$58.84

$60.44

$65.00

$67.03

Click on to enlarge

Supply: Firm filings and creator calculations

This improve in NOPAT has been achieved because of rising NOPAT margins, which have gone from 6.23% in 2020 to six.5% within the TTM.

A Free Money Move Machine

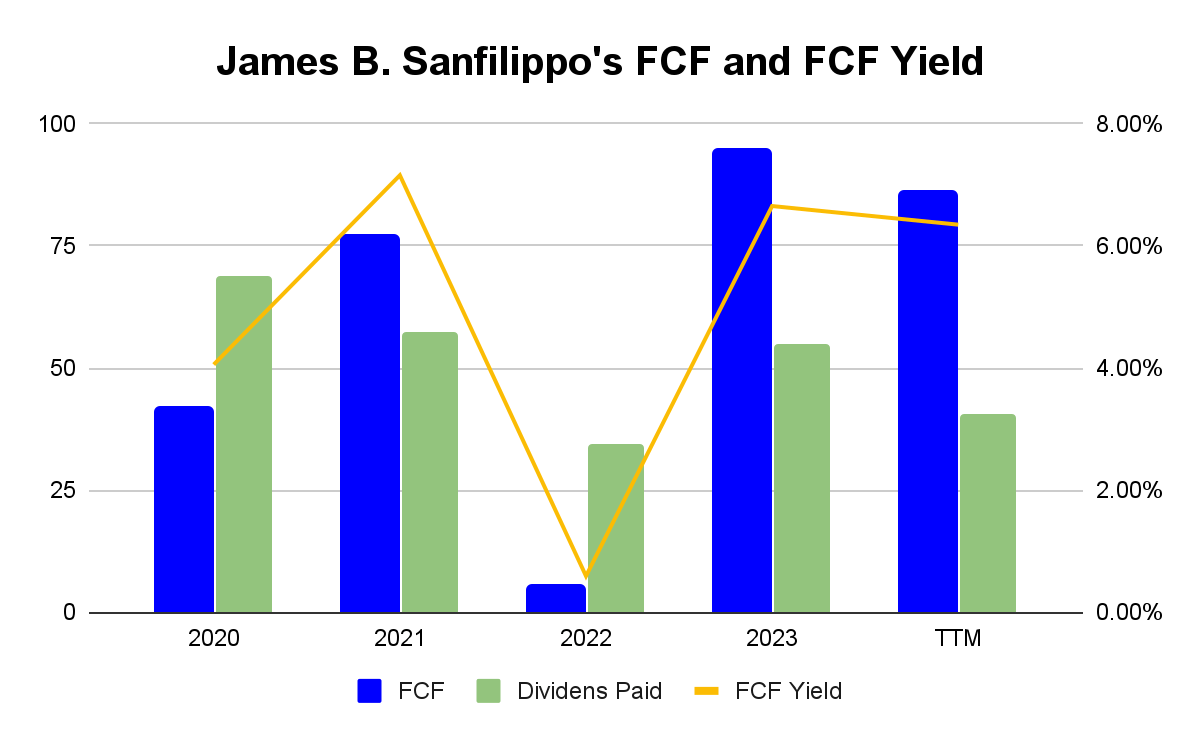

Since 2020, Sanfilippo has compounded free money flows (FCF) at a charge of 15.51% a 12 months, rising them from $41.76 million in 2020 to $85.87 million within the TTM. The full FCF the corporate has generated in that point is the same as $304.84 million, or round 27% of its market capitalization. Not solely has the corporate generated huge sums of FCF, that FCF is accessible at engaging ranges, with a present FCF yield of 6.35%. As well as, cumulatively, the corporate has paid out 256.22 million in dividends within the final 5 years, nicely under the cumulative $304.81 million it generated in FCF. That demonstrates the protection of the dividends and implies room for will increase in dividends paid.

Supply: Firm filings and creator calculations

Capital Effectivity is Rising

ROIC has risen from 16.61% in 2020 to 17.69% within the TTM, which is additional proof of how the SVA Plan has aligned administration with shareholder pursuits, and incentivized them to extend ROIC. Rising ROIC has been pushed by bettering invested capital turns, a measure of steadiness sheet effectivity calculated by dividing income by common invested capital. Invested capital turns have risen from 2.65 in 2020 to 2.72 within the TTM.

Sanfilippo is Barely Overvalued

Sanfilippo’s intrinsic worth, which may be estimated utilizing Financial Guide Worth (EBV), a measure utilized by funding analysis agency, New Constructs, and which represents the pre-strategy worth of the enterprise, as seen within the desk under:

Financial Class (Worth in hundreds of thousands, besides per share quantities)

2020

2021

2022

2023

TTM

NOPAT

$54.83

$58.84

$60.44

$65.00

$67.03

WACC

3.48%

2.75%

3.87%

5.73%

6.70%

Extra Money

$ –

$ –

$ –

$ –

$ –

Internet Belongings from Discontinued Operations

$ –

$ –

$ –

$ –

$ –

Internet Deferred Tax Legal responsibility

$ –

$ –

$ –

$ –

$ –

Internet Deferred Compensation Belongings

$ –

$ –

$ –

$ –

$ –

Truthful Worth of Unconsolidated Subsidiary Belongings (non-op)

$ –

$ –

$ –

$ –

$ –

Truthful Worth of Complete Debt

$56.05

$30.15

$55.87

$20.37

$54.71

Truthful Worth of Most well-liked Capital

$ –

$ –

$ –

$ –

$ –

Truthful Worth of Minority Pursuits

$ –

$ –

$ –

$ –

$ –

Worth of Excellent ESO After-Tax

$ –

$ –

$ –

$ –

$ –

Pensions Internet Funded Standing

$ (32.20)

$ (35.55)

$ (29.51)

$ (28.02)

$ (28.02)

Financial Guide Worth (EBV)

$1,551.64

$2,145.18

$1,535.29

$1,141.99

$973.82

Cut up Adjusted Shares Excellent (hundreds)

11,419.00

11,468.00

11,527.00

11,556.00

11,570.00

EBV per Share

$135.88

$187.06

$133.19

$98.82

$84.17

Closing Inventory Worth

$82.62

$88.40

$72.49

$119.36

$104.02

Worth to Financial Guide Worth (PEBV)

0.61

0.47

0.54

1.21

1.24

Click on to enlarge

As you possibly can see, with a share worth of $96.54 at time of writing, Sanfilippo is buying and selling at almost 15% of its EBV, implying that the market expects a larger charge of financial profitability than is indicated by Sanfilippo’s present money flows.

Conclusion

By any measure, Sanfilippo is a nicely run, worthwhile enterprise whose managers are correctly incentivized to pursue shareholder pursuits. Sadly, the market has caught as much as this actuality, and since 2023, the corporate has been buying and selling at above its intrinsic worth. I cap purchase suggestions at a PEBV of 1.2, and Sanfilippo simply misses out. For holders of the inventory, I say, stay invested, however for everybody else, put Sanfilippo in your watch listing.

:max_bytes(150000):strip_icc()/nikola_badger2-28963695a2fae6f2920734d1af0bdf3f1917c5d6e1826ad26d2bfe2cd6686ec9-c201b13fd17a462fa091b2cd28882980.jpg)

:max_bytes(150000):strip_icc()/GettyImages-1419556699-99a5c70b53f6443ba3c200c5e37d2239.jpg)

{kind=link}