Jose Luis Pelaez Inc

I reviewed Zoetis (NYSE:ZTS) practically a yr in the past and gave the corporate a “Purchase” ranking. I appreciated that the corporate was targeted on continued innovation and is a world chief in a distinct segment market.

Since that article, the inventory is sort of flat, definitely underachieving in comparison with the S&P 500. Regardless of these lackluster outcomes, I’m nonetheless a believer in Zoetis and stay bullish on the enterprise.

Let’s dig into present occasions and the corporate’s latest monetary efficiency.

Security Issues?

I imagine Zoetis’s lackluster efficiency within the first half of 2024 is in some half as a result of Wall Road Journal article printed final April, which accused Zoetis’s arthritis medication (Librela and Solensia) of getting dangerous results to homeowners’ pets.

On the corporate’s Q1 2024 convention name, CEO Kristin Peck adamantly defeated the corporate’s arthritis remedy medication, saying this about Librela, “…I actually wish to underscore that now we have the utmost confidence within the security and efficacy of Librela. It has been used for over three years throughout the globe and over 14 million canines, and it is accredited in over 50 nations. And in the event you total have a look at the speed of reported adversarial occasions, it is about 18% per 10,000 or 0.18% globally.”

Concerning each medication and Zoetis’s security requirements, Peck went on to state, “We’re unwavering in our dedication to rigorous security and high quality requirements, which has earned us the belief and confidence of veterinarians worldwide. Backed by that dedication, Librela and Solensia are protected and efficient. They’re anchored in 10 years of science and have been utilized in Europe for greater than three years. Within the U.S., 78% of veterinarians who’re on the middle of care are very happy with Librela. That is pushed by actual world expertise and in keeping with the suggestions we hear in different markets. And our analysis signifies that 46% of vets globally will deal with OA earlier and 65% will deal with extra canines now that Librela is obtainable.”

Security issues are at all times a threat with a healthcare firm, nevertheless it appears to me these accusations might need overstated. The corporate’s administration nonetheless believes osteoarthritis ache (OA) would be the subsequent billion-dollar alternative for Zoetis.

Within the first quarter, Librela gross sales grew 189% proportion globally, with $40 million in U.S. gross sales. Regardless of, the detrimental media consideration, administration didn’t alter income steering for Librela. Till steering is modified, or the adversarial unwanted side effects turn into extra of a pronounced concern, I’m inclined to imagine the funding thesis for Zoetis is firmly on monitor.

Individuals Love Their Pets

A guess on Zoetis is a guess on people persevering with to care about their pets. The info definitely helps the human-animal bond is robust, as 86% of pet homeowners said they’d pay “no matter it takes” if their pet wanted in depth veterinary care. Moreover, a examine discovered even with a 20% lower in a household’s price range, pet homeowners wouldn’t spend much less on their pets.

Furthermore, the “loneliness epidemic” has been gaining consideration after the COVID-19 pandemic. In a previous survey carried out by the U.S. Well being Sources and Companies Administration, “Two in 5 People report that they often or at all times really feel their social relationships will not be significant, and one in 5 say they really feel lonely or socially remoted.”

Many research have been carried out which present that pet possession may help alleviate loneliness. One specific examine carried out by BMC Geriatrics discovered that in an evaluation of roughly 5,000 older adults, those that owned pets had been much less prone to report being lonely.

As I don’t see the human-pet connection fading, nor do I foresee the “loneliness epidemic” going away (though I perceive it is a extra complicated concern than merely getting a pet). People will proceed to have pets, and that’s why Zoetis’s deal with companion animals pays dividends sooner or later.

Financials

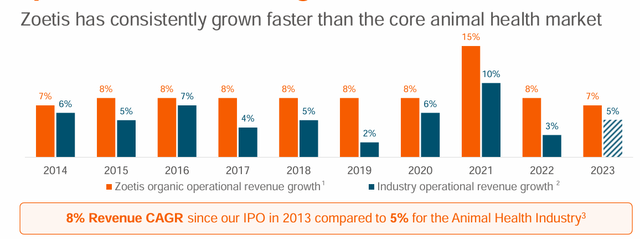

Since Zoetis went public again in 2013, the corporate has outpaced the S&P 500 regardless of the corporate’s subpar efficiency this yr.

As you’ll be able to see beneath, Zoetis has an 8% income CAGR since that point:

Investor Presentation

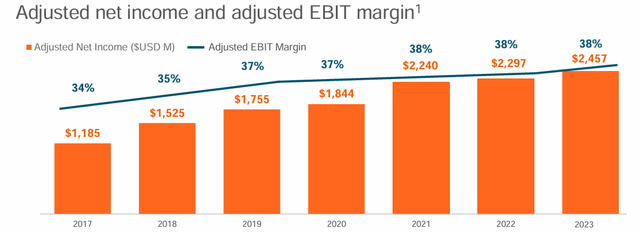

The corporate’s adjusted internet earnings and adjusted EBIT margin have continued to climb as effectively:

Investor Presentation

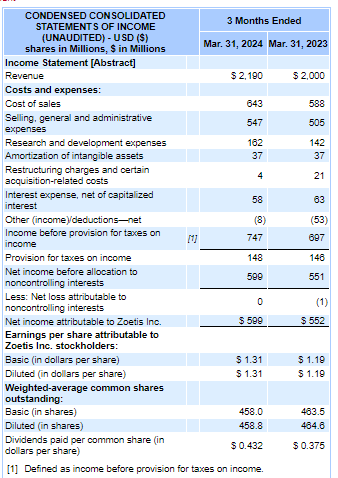

Within the newest quarter Zoetis delivered gross sales of roughly $2.2 billion, which is a rise of 10% in comparison with the prior yr quarter. U.S. gross sales for the quarter had been $1.2 billion, a rise of 16% in comparison with Q1 2023. Worldwide gross sales had been $1 billion for the quarter, which is a rise of three% in comparison with Q1, 2023.

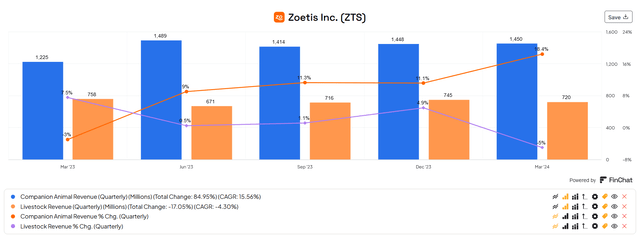

Zoetis’s companion animal portfolio was the principle driver of income development for the quarter, as gross sales of companion animal merchandise grew 25% in the US and 10% internationally.

As you’ll be able to see from this graphic, companion animal income has continued to guide livestock income over the previous couple of quarters and income development is considerably increased for companion animal in comparison with livestock:

Finchat.io

This income development led to Zoetis reporting increased internet earnings and better earnings per share, as you’ll be able to see beneath:

SEC.gov

Given the power of the corporate’s companion animals merchandise, Zoetis elevated their full yr 2024 steering as they now count on income between $9.05 billion to $9.2 billion and internet earnings between $2.45 billion and $2.495 billion.

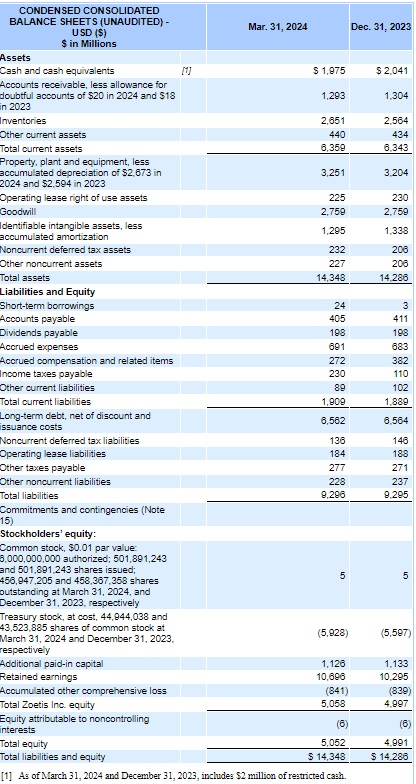

From a steadiness sheet perspective, Zoetis does have extra long-term debt than I usually prefer to see, nevertheless the corporate nonetheless has amble present property to cowl all of their present liabilities as you’ll be able to see beneath:

SEC.gov

Valuation

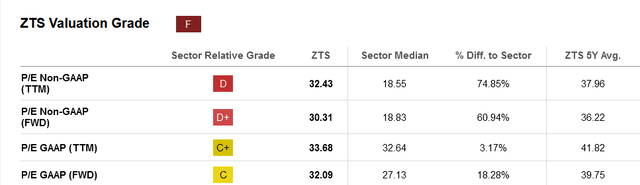

As a frontrunner in a world area of interest market, Zoetis trades at a premium valuation, as a number of the metrics beneath illustrate:

Searching for alpha

Nevertheless, I believe Zoetis’s valuation is cheap given its development prospects and place as a frontrunner throughout the pet healthcare business.

I believe P/E ratio is an effective valuation metric for Zoetis. Final yr Zoetis was buying and selling at a P/E GAAP (FWD) ratio of 34.05 which, as you’ll be able to see above, is beneath the present P/E GAAP ratio of 32.09. That is additionally effectively beneath the corporate’s five-year common of 39.75.

Given the corporate’s development prospects, particularly the famous billion-dollar alternative with osteoarthritis ache and Wall Road’s perception that earnings per share will proceed to rise as income grows at a charge between 8% to 10% over the following few years, I believe traders really feel snug shopping for that these ranges. Though, the inventory’s worth was extra enticing in April close to $150, it’s nonetheless beneath the $190 worth again in January of this yr. Thus, I really feel snug including to my place within the $175-$180 worth vary.

Dangers

Zoetis lists quite a few dangers with the corporate’s threat components part inside their 10K, however I’m going to cowl two primary dangers I foresee for the corporate.

As I famous with Wall Road Journal, I believe security issues with merchandise will at all times be a long-term threat related to Zoetis. Other than a decline in income, litigation could be a priority as effectively ought to a top-selling product, equivalent to Librela, produce dangerous unwanted side effects.

Second, as Zoetis is a world firm and their worldwide gross sales are a major quantity of the corporate’s total gross sales, I believe Zoetis is topic to extra international financial and political dangers. Continued international battle in locations like Israel, Russia/Ukraine and the Center East might definitely negatively influence the corporate’s backside line.

Conclusion

I believe Peck said Zoetis’s funding thesis completely when she mentioned this on the most recent convention name, “…For greater than 70 years, Zoetis has been main the business with our dedication to innovation. We have invested over $5 billion in R&D since our IPO, which has introduced greater than 300 product strains to the market. Science is and at all times has been the nice disruptor and on the core of our success in delivering the improvements that veterinarians, livestock producers and pet homeowners count on from us.

Regardless of some latest security issues, I nonetheless imagine Zoetis is a top quality enterprise. Zoetis has continued to develop income and create new medication for each companion animals and livestock.

I believe the bond between people and pets is robust, and pet homeowners are extra keen than ever to deal with their pets.

Though Zoetis isn’t an inexpensive inventory, I imagine this firm will reward affected person long-term traders.

{kind=link}