Discovering the appropriate financial savings account can get you an additional $200 without cost this 12 months.

Relying in your steadiness, it may make you much more cash.

Let’s say you could have $10,000 to place into among the best on-line financial savings account.

How a lot would that flip into at a giant financial institution financial savings account? Most large banks have an APY (annual share yield) of 0.15% or much less. After a 12 months, your account can be value $10,015. Not a lot of a achieve there.

I really like getting cash for nothing, however even I’ve a tough time getting excited over an additional $15.

Now let’s say you are taking that very same $10,000 and put it into a web-based high-yield financial savings account with an APY of two.25%.

After a 12 months, you’ll have $10,225.

That’s $225 for doing completely nothing. Everybody wants some further money available for an emergency fund anyway. Why not get as a lot as you possibly can whereas it sits there? All it takes is opening the appropriate account.

The very best on-line financial savings accounts

We’re going to do a deep dive into what to search for, which accounts are finest, tips on how to get the very best APY, and tips for optimizing your financial savings accounts.

Right here’s a breakdown of what we’ll cowl:

What Issues When Selecting an On-line Financial savings Account:

Consumer Expertise and Firm ReputationFeesConvenienceFDIC InsuranceAPY Charges

On-line Financial savings Account Critiques:

The 4 Step Course of to Selecting an On-line Financial savings Account

If you wish to skip all of that and open an account proper now, these excessive curiosity on-line financial savings accounts had been our high rated:

You’ll be proud of any of them. My private favourite is Ally.

What issues when choosing a web-based financial savings account

Right here’s how we consider these accounts.

Consumer expertise and firm popularity

Good on-line and cell apps make an enormous distinction today, nevertheless it doesn’t matter as a lot whenever you’re searching for a excessive curiosity on-line financial savings account.

It must be adequate however not nice.

Why?

As a result of we not often log into financial savings accounts. They normally have limits of with the ability to withdraw from them as much as 6 instances per 30 days. By definition, they’re not meant for use usually.

Having fast and easy accessibility to your funds is much less vital than working with an organization that has a dependable popularity.

Whereas most prospects can entry their high-interest fee accounts rapidly in an emergency, not all monetary establishments are created equal. We skipped corporations that scored lower than 65 % of the Harris Ballot Company Status Rankings like Wells Fargo, Goldman Sachs, and Financial institution of America. We additionally factored in main scandals over the past 5 years.

Again to High

Charges

For on-line financial savings accounts, it’s completely important that you simply get an account with none upkeep charges. Month-to-month upkeep charges was once frequent. Fortunately, most accounts have executed away with them.

On any good financial savings account, you’ll not often run into charges throughout regular utilization. However even on one of the best accounts, it’s doable to set off charges for sure occasions:

Returned deposit itemsOverdraft gadgets paid or returnsExcessive transaction payment (like going over 6 withdrawals per 30 days)Expedited deliveryOutgoing home wiresAccount analysis charges

We’ve made certain to not embody any banks in our listing which have upkeep charges. However you ought to be conscious of a few of these different payment gadgets that do exist on each account.

Again to High

Comfort

What we contemplate to be “handy” with financial savings accounts falls into two buckets relying on the place you might be in your individual private finance journey.

Once you’re constructing financial savings for the primary time, it’s important to get an account with no minimal steadiness requirement. A $5 required steadiness or one thing like that’s high quality, you simply don’t wish to have to fret a couple of increased one.

Don’t put up with any account that requires a large minimal steadiness. There are such a lot of choices that don’t have any steadiness necessities in any respect. That is the very last thing you ought to be nervous about within the early days, particularly if an emergency comes up and that you must withdraw money.

Afterward, what you contemplate to be handy sometimes modifications.

When you’ve constructed sufficient of a money buffer for your self, you’ll care rather a lot much less about minimal balances. As a substitute, your accounts, playing cards, and banks have all gotten sophisticated sufficient that simplicity issues much more than it used to. At this stage, some people will go for a decrease APY with a purpose to consolidate their accounts and make the whole lot extra manageable.

Is that this the optimum technique to get each ounce of development out of your money? No, it isn’t. However the further piece of thoughts could be properly value the fee. If this sounds interesting to you, verify to see if the financial savings account at your major financial institution has a adequate APY with none upkeep charges. If it does, it could possibly be your only option.

Again to High

FDIC insured

Don’t ever contemplate a web-based financial savings account that’s not FDIC insured. Which means the account is assured by the federal authorities as much as $250,000 per depositor. If one thing horrible ought to occur to the financial institution, the federal authorities ensures you’ll nonetheless get entry to your steadiness, as much as $250,000. That is per depositor, so the $250,000 consists of the mixed steadiness of all of your financial savings accounts on the similar financial institution.

Nearly each financial savings account is FDIC insured. It’s been a typical follow for a very long time. However preserve a detailed eye on this any time you’re contemplating an revolutionary or distinctive method to storing your money.

For instance, some people will retailer their money in a cash market account, which operates rather a lot like a financial savings account. Cash market accounts are normally FDIC insured. However cash market funds, which you place money into from a brokerage account, usually are not FDIC insured. A refined but vital distinction throughout tenuous instances.

One other instance: Robinhood tried to roll out a checking account that promised a 3% APY. That’s a checking account paying increased curiosity than any financial savings account that was out there on the time, by nearly 1%. Sounds superb proper?

It got here with quite a lot of catches, certainly one of which was that it wasn’t FDIC insured. With out the FDIC insurance coverage, we don’t contemplate the upper APY definitely worth the danger.

Our stance is that each greenback of our financial savings needs to be lined by the FDIC, even when the steadiness is excessive sufficient that we’ve got to separate it up between a number of financial savings accounts.

The entire accounts that we overview under are FDIC insured. Simply preserve a watch out for this in case you’re exploring an atypical method to storing your money.

Again to High

APY charges

APY charges — the annual share yield — are the principle distinction between financial savings accounts. The upper your APY fee, the more cash that you simply get routinely each month.

APY charges throughout saving accounts typically fall into 3 tiers.

Large financial institution financial savings account APYs

For the overwhelming majority of massive financial institution financial savings accounts, the APY is horrible. Large banks assume that you really want a financial savings account alongside together with your checking account, so that they don’t do something to entice you for the financial savings account itself. Even when loads of on-line high-yield financial savings accounts are providing an APY of two%, large banks may solely provide a 0.15% APY. On a financial savings steadiness of $10,000, that’s a distinction between making $200 a 12 months versus $20 a 12 months.

This doesn’t apply to ALL large banks, however most of them do fall into this class. So preserve a watch out for these. Until you actually wish to maximize comfort by consolidating accounts and taking a decrease APY, it’s value discovering an account with a better APY.

Excessive yield financial savings account APYs

Excessive yield financial savings accounts have turn into extraordinarily common. These banks don’t have branches, they’re 100% on-line. Since save rather a lot from not having bodily places, they cross the financial savings onto you with a better APY.

Ally and American Categorical are two of the preferred banks on this class.

The APY additionally stays up to date over time. Again in the course of the monetary disaster, the Federal Reserve dropped rates of interest to 0% and most excessive yield financial savings accounts had APYs of 0.5-0.7%. Because the Federal Reserve elevated rates of interest, these similar accounts additionally elevated their APY. Each time rates of interest improve, you’ll get these will increase routinely from these accounts. No have to always change between accounts and chase one of the best fee.

Innovative APYs

At any given second, there are a number of banks which might be pushing the APYs increased than anybody else. They’re doing this as a promotional technique to draw extra prospects. A few of these banks preserve tempo with altering rates of interest, a few of them don’t.

Whereas we don’t contemplate it definitely worth the effort to chase an additional 0.1% on our APY, these banks are an possibility in case you’re seeking to maximize the APY in your financial savings.

On-line financial savings account opinions

Right here’s the lowdown on the preferred on-line financial savings accounts.

Axos financial savings account

FDIC insured: YesMinimum steadiness: NoneMaintenance charges: NoneAPY: 1.30%

The APY is far decrease than different high-yield financial savings accounts — it’s common at finest. There’s no purpose to open an Axos account until you’ve already maxed the FDIC limits on each different high-yield financial savings account and must get a decrease APY to horde all of your money.

I like to recommend choosing one of many different accounts from this listing.

Uncover on-line financial savings account

FDIC insured: YesMinimum steadiness: NoneMaintenance charges: NoneAPY: 1.60%

Uncover’s APY is fairly sturdy. Not fairly the highest, nevertheless it’s actually shut.

And in case you occur to have a Uncover card or checking account, conserving your accounts in a single place makes the whole lot rather a lot easier.

You probably have one other Uncover account, undoubtedly get a Uncover financial savings account.

HSBC

HSBC has a number of completely different financial savings accounts.

HSBC Premier Financial savings

FDIC insured: YesMinimum steadiness: $100,000 throughout your deposit accounts and funding balances. If you happen to go under this steadiness, there’s a $50 month-to-month payment.Upkeep charges: NoneAPY: 0.15%

The HSBC Premier accounts are for shoppers who’ve giant deposits at HSBC. Sadly, the APY is terrible. An APY that low with a minimal steadiness of $100,000 is type of insulting.

This can be a good instance of a basic large financial institution financial savings account. A bunch of constraints with a horrible APY. Skip these accounts completely.

HSBC Direct Financial savings

FDIC insured: YesMinimum steadiness: $1Maintenance charges: NoneAPY: 1.85%

HSBC does have a high-yield financial savings account with a aggressive APY. Usually, I’d suggest this account as a major contender.

However HSBC is only a horrible financial institution. Each interplay with them is tougher than it must be. The one purpose I’d ever contemplate opening an HSBC account if I wanted an enormous, worldwide financial institution for some purpose.

Despite the fact that this account appears nice on paper, you’ll remorse it in case your expertise is something like ours.

Ally financial savings account

FDIC insured: YesMinimum steadiness: NoneMaintenance charges: NoneAPY: 1.6%

We’re enormous followers of Ally. They’ve turn into one of many main high-yield financial savings accounts.

Sure, Ally doesn’t technically have the very best APY, nevertheless it’s darn shut. They usually replace their APY usually. So if rates of interest proceed to rise, you’ll get a better APY with out having to do something.

Their account UI is fairly slick too, and it’s all the time bettering.

I’ve an Ally account myself.

Be happy to cease studying right here and open an Ally account proper now. You received’t remorse it.

Capital One 360 Financial savings

FDIC insured: YesMinimum steadiness: NoneMaintenance charges: NoneAPY: 1.7%

Capital One used to have an APY that lagged the remainder of the market, making it a sub-standard alternative. You’d have to make use of one other financial institution or their Capital One 360 Cash Market account to get a aggressive APY.

Now they’ve an APY that’s simply pretty much as good as most banks. It’s one of many high contenders.

Particularly if in case you have Capital One bank cards, it’s very nice to maintain the whole lot at one financial institution.

Marcus by Goldman Sachs

FDIC insured: YesMinimum steadiness: None, however there’s a deposit restrict of $1,000,000 for all of your financial savings account and CDsMaintenance charges: NoneAPY: 1.7%

Goldman Sachs jumped into the high-yield financial savings account house with one of many highest APYs.

They do restrict deposits to a complete of $1,000,000, however that’s not a significant concern. You’ll wish to break up up your money balances throughout a number of banks to get all of it FDIC insured anyway.

If you happen to’re searching for your first high-yield financial savings account, this can be a incredible possibility.

American Categorical financial savings account

FDIC insured: YesMinimum steadiness: NoneMaintenance charges: NoneAPY: 1.7%

American Categorical was one of many first to introduce a high-yield financial savings account, and it’s been round for awhile now.

Nowadays, the APY is barely decrease than among the rivals. Whereas American Categorical does replace their yields ceaselessly, they’re all the time 0.10-0.20% off the very best charges. Whereas it’s nonetheless an amazing possibility, I’d select one of many different accounts because of this alone.

One different caveat: the American Categorical financial savings account isn’t built-in into the identical login account because the American Categorical bank cards. Even if in case you have each, it looks like having two completely different banks. There’s no further simplicity from making an attempt to consolidate.

Barclays financial savings account

FDIC insured: YesMinimum steadiness: NoneMaintenance charges: NoneAPY: 1.7%

One other nice possibility. Nice APY, no upkeep charges or minimal balances — you possibly can’t go flawed with a Barclays on-line financial savings account.

Synchrony financial savings account

FDIC insured: YesMinimum steadiness: NoneMaintenance charges: NoneAPY: 1.7%

Synchrony can also be an amazing possibility. The APY is likely one of the highest and has no minimums or upkeep charges.

Vio Financial institution

FDIC Insured: YesMinimum Deposit: $100Maintenance Charges: NoneAPY: 1.85%

This account presents increased returns as a result of the financial institution has no bodily places. They provide a aggressive APY with a low minimal deposit. You’ll wish to look out for the $5 payment to obtain paper statements and a $10 payment for any withdrawal over the allotted six transactions per 30 days.

Comenity Direct Financial institution

FDIC Insured: YesMinimum Deposit: $100Maintenance Charges: NoneAPY:1.90%

Comenity Financial institution has aggressive charges and doesn’t cost a upkeep payment. Purchasers additionally get free ACH transfers, free on-line statements, free incoming transfers, and limitless deposits on their cell app or through ACH switch. They do cost for outgoing wire switch, official verify requests, and paper assertion charges. Comenity has an interest-earning restrict on balances of $10 million.

Residents Entry

FDIC Insured: YesMinimum Deposit: $5,000Maintenance Charges: NoneAPY: 1.85%

Whereas Citizen’s Entry does have a better minimal steadiness to earn curiosity, the APY could be very aggressive, and so they rank excessive for his or her CDs as properly. Citizen’s Entry doesn’t have a cell app and so they don’t provide any checking accounts, so that you’ll have to separate your funds between two monetary establishments.

The 4-step course of to choosing one of the best on-line financial savings account

Verify the banks that you simply at present have accounts with and see if they’ve a aggressive financial savings account. If the APY is similar to the accounts we listed above, stick together with your present financial institution.In any other case, decide an account from this listing:

Uncover On-line Financial savings Account

Ally financial savings account

Marcus by Goldman Sachs

American Categorical financial savings account

Barclays financial savings account

Synchrony financial savings account

Attempt to decide an account from a financial institution that you simply foresee doing different enterprise with. For instance, Ally has automotive loans and Uncover has their bank cards.If you happen to’re nonetheless unsure, go together with Ally.

What about sub-savings accounts?

One in all our favourite financial savings account tips is to open “sub-accounts.” This permits us to simply finances for greater purchases by saving slightly bit every month. We are able to additionally monitor the whole lot by separating all of the accounts.

For instance, I’ve these classes in my very own financial savings account:

Emergency fundHouse downpaymentMini-retirementChristmas giftsAnnual trip

Every month, cash goes into every of those separate accounts with the automated transfers that I arrange. And I can simply see how a lot I’ve saved in the direction of my targets.

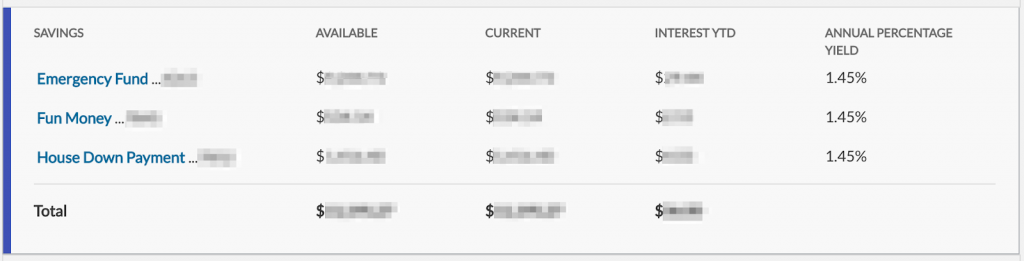

Ramit’s financial savings accounts used to appear like this again earlier than ING Direct was purchased by Capital One:

Right here’s a extra present instance in Ally:

Some financial savings accounts will name these “sub-accounts,” and the whole lot shall be a part of the identical financial savings account. This can be a uncommon function to seek out although.

For everybody else, merely open up a number of financial savings account below the identical financial institution login. You possibly can simply have 5-10 accounts on the similar financial institution. Then deal with every account for no matter saving class that you simply like.

This implies you will get “sub-accounts” at any financial institution, even when they don’t have a “sub-account” function.

Don’t chase yields

Look, there’s all the time a financial institution that has a barely increased APY. Banks use it as a promotion technique to get extra accounts, so it’s all the time altering.

Frequently researching new APY charges, searching for that further 0.05% APY, opening accounts, and transferring cash in every single place wastes extra time than it’s value.

Don’t be a fee chaser.

Bear in mind IWT’s philosophy of massive wins. Give attention to the key wins that actually transfer the needle and neglect in regards to the small stuff. Chasing increased APYs on financial savings accounts undoubtedly falls into the “small stuff” class.

Decide a financial savings account that has a aggressive APY from a financial institution that you simply belief for the long run. Then keep on with that call and work on bettering different areas of your life.

Cash market accounts vs financial savings accounts

The distinction between cash market accounts and financial savings accounts could be fairly complicated.

That’s as a result of there’s no sensible distinction.

Listed below are the similarities:

The APY tends to be the identical between each varieties of accounts.You possibly can withdraw as much as 6 instances per 30 days.Some have ATM playing cards, some don’t.Some have minimums, some don’t.Each are FDIC insured.

Principally they’re the identical account. In case your financial institution occurs to supply a cash market account with no upkeep charges, no minimal, and a aggressive APY, be at liberty to make use of it.

Now for the complicated half: cash market funds are fully completely different. They’re a part of brokerage accounts and help you place money when you wait to take a position it. Since cash market funds usually are not FDIC insured, so it’s not an excellent behavior to retailer lots of money in them.

When to get financial savings accounts from a number of banks

If you happen to ask excessive web value people which financial savings accounts they’ve, typically they’ll listing off half a dozen completely different banks.

At first, this is unnecessary. Why all the additional complexity and completely different accounts?

There’s one purpose: FDIC insurance coverage limits.

Most individuals are restricted to $250,000 value of insurance coverage at any given financial institution. Joint accounts and accounts throughout completely different classes (like retirement accounts) can improve this restrict, however that solely goes up to now. You probably have a considerable amount of money, the one solution to preserve it insured is to open up financial savings accounts throughout a number of banks.

That’s why people will begin opening up financial savings accounts throughout a number of banks.

You probably have a number of financial savings accounts to handle, Max will routinely transfer balances round your accounts to optimize for the very best APY whereas conserving all of your money insured. They do cost a 0.08% annual payment for the service.

As for which accounts to open, we suggest beginning with these:

Any mixture of accounts which have sturdy APYs will work.

:max_bytes(150000):strip_icc()/What-difference-between-standard-Error-means-and-standard-deviation_color-1c203133aca641aca0d03936d9558693.jpg)

/what-difference-between-magnum-cum-laude-and-summa-cum-laude_V2-3ae02babdc714ea9adaeec0f0a6bf1a5.png)

{kind=link}