ablokhin

Citigroup Inc. (C) and Financial institution of America Company (NYSE:BAC) have turn out to be investor favorites in latest days after each banks reported better-than-expected second-quarter outcomes.

Even if each banks have benefited from rising web curiosity earnings courtesy of the central financial institution, I imagine this can be very harmful to spend money on cyclical banks at a time when development is declining. Financial institution of America is more likely to face even stronger headwinds sooner or later, as provisions for credit score losses have begun to climb.

I proceed to imagine that Financial institution of America’s inventory will commerce at a reduction to ebook worth inside the subsequent 12 months.

A Robust Quarter However Headwinds Are Rising

Citigroup and Financial institution of America inventory rose 13% and seven% on Friday, respectively, after Citigroup reported good 2Q-22 earnings that confirmed robust commerce outcomes and better earnings amid increased rates of interest.

By way of gross sales and earnings per share, Citigroup’s second-quarter efficiency additionally beat analysts’ forecasts. EPS was considerably increased than anticipated ($2.19 vs. $1.68 projected), whereas income of $19.64 billion exceeded the typical analyst forecast of $18.22 billion.

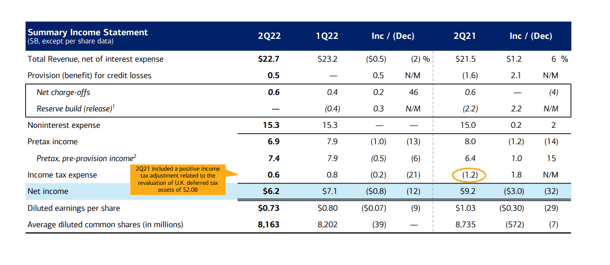

Financial institution of America earned $0.73 per share versus a consensus expectation of $0.78 per share, on income of $22.69 billion versus a consensus of $22.67 billion.

Financial institution of America skilled a robust second quarter. Financial institution of America’s Shopper Financial institution continued to carry out nicely in 2Q-22, with web curiosity earnings rising and a complete revenue of $6.25 billion remaining on the finish of the day. Regardless of billions in second-quarter revenues, Financial institution of America’s earnings fell 32% 12 months on 12 months.

Abstract Earnings Assertion (Financial institution of America)

There are two areas of Financial institution of America’s second-quarter earnings that I imagine require additional dialogue.

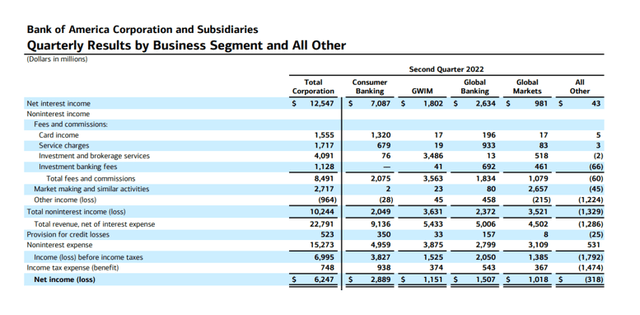

First, Financial institution of America’s second-quarter efficiency had been as soon as once more bolstered by a strong displaying from the Shopper Financial institution. Financial institution of America’s Shopper Financial institution is the customer-facing division that accepts deposits, makes private loans to debtors, consults prospects in Financial institution of America’s monetary facilities, and points bank cards.

Throughout final 12 months’s financial growth, Financial institution of America’s efficiency was largely pushed by the Shopper Financial institution. The division earned $2.89 billion in earnings in 2Q-22, the most important of any enterprise phase. Income from shopper banks accounted for almost half of Financial institution of America’s complete second-quarter revenue of $6.25 billion.

Quarterly Outcomes By Enterprise Section (Financial institution of America)

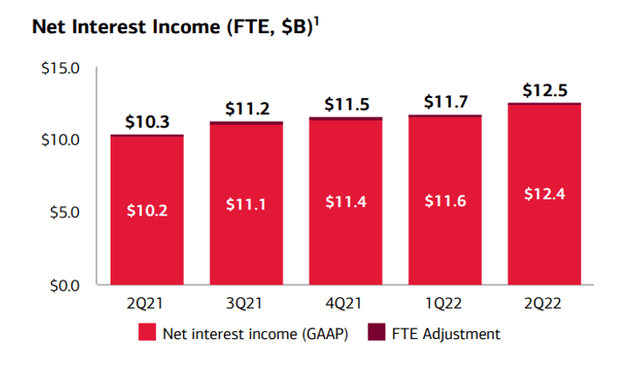

The rise in web curiosity earnings was the second motive for Financial institution of America’s robust earnings report. Banks profit within the close to time period from rising rates of interest as a result of they’ll lend cash at higher charges.

Financial institution of America benefited from the rise in rates of interest within the second quarter, with web curiosity earnings rising $800 million QoQ to $12.5 billion in 2Q-22.

Internet curiosity earnings is a big supply of earnings for banks that’s straight influenced by the central financial institution’s financial coverage. Financial institution of America’s web curiosity earnings climbed by $2.2 billion within the final 12 months.

Internet Curiosity Earnings (Financial institution of America)

Nonetheless, current web curiosity earnings positive factors don’t seize the entire story as a result of increased rates of interest cool the financial system. The central financial institution boosts rates of interest to forestall the financial system from overheating, which is mostly interpreted as an indication of a recession.

Extremely cyclical, economy-dependent companies, akin to Financial institution of America’s Shopper Financial institution, are poised to undergo from a recession, which regularly leads to decreased mortgage volumes, decreased bank card use, and higher defaults.

Asset High quality Is Deteriorating

Robust Shopper Financial institution earnings and rising web curiosity earnings are each good issues, however Financial institution of America’s deteriorating asset high quality is a priority, particularly if current tendencies proceed into the second half of the 12 months.

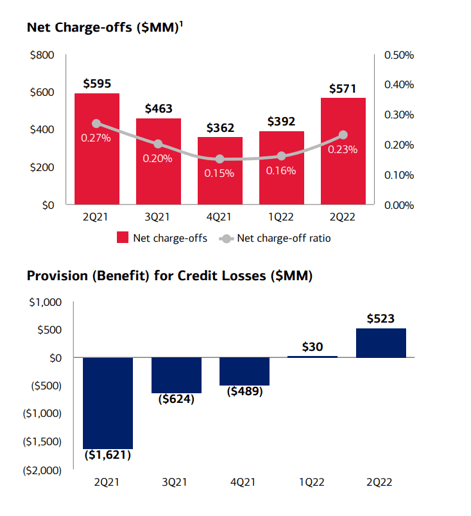

The financial institution’s web charge-off ratio climbed from 0.16% in 1Q-22 to 0.23% in 2Q-22 which is a reasonably substantial improve. On the similar time, Financial institution of America’s provision for credit score losses elevated from $30 million to $523 million. Bigger web charge-off ratios and provisions point out increased predicted mortgage losses sooner or later because of the financial institution’s prospects’ deteriorating monetary well being.

Internet Cost-Offs (Financial institution of America)

Why Financial institution of America May See A Larger Inventory Worth

Analysts are nonetheless debating when, not if, a recession will happen. Nonetheless, if a recession is prevented and the central financial institution controls inflation, the best way could also be cleared for Financial institution of America’s shares to surge increased. The identical could also be stated for asset high quality tendencies. Financial institution of America could be a winner sooner or later if its credit score troubles don’t worsen and credit score provisions don’t rise.

Count on Financial institution of America To Commerce At A Low cost To E-book Worth

In my view, the U.S. financial system is on the verge of getting into a recession, which could happen within the second a part of the 12 months or in 2023. Investing in cyclical shares akin to banks in a deflating financial system with rising inflation carries extraordinarily excessive dangers for buyers.

Financial institution of America is buying and selling at 1.09x ebook worth, representing a 9% premium. Financial institution of America has traded at massive low cost to ebook worth in harder financial occasions, and I imagine that is the place we’re headed.

My Conclusion

Financial institution of America’s 2Q-22 earnings report was optimistic, however I do not imagine the euphoria for financial institution shares generally is justified given the state of the financial system. Earnings had been robust, and web curiosity earnings elevated.

Provisions for credit score losses, alternatively, point out that asset high quality points are rising on Financial institution of America’s steadiness sheet. Lengthy-term, increased rates of interest translate into cyclical earnings dangers for shopper banks.

Due to cyclical and financial headwinds, I imagine Financial institution of America will start to commerce at a reduction to ebook worth inside the subsequent 12 months.

/what-difference-between-magnum-cum-laude-and-summa-cum-laude_V2-3ae02babdc714ea9adaeec0f0a6bf1a5.png)

/HabitsThatWillHelpYouPayOffDebtMay202021-51f5539c69cf4a7ba82f9f7059c10f5c.jpg)

{kind=link}