Revealed on July thirtieth, 2022 by Nikolaos Sismanis

If one thinks of their favourite blue chip shares, the primary names that come to thoughts are normally large firms that generate tens of billions of {dollars} in income per 12 months. Whereas it’s true that typically larger firms get pleasure from a lot of aggressive benefits, together with an amazing moat and scaling economics, amongst others, the scale of an organization is just not essentially a essential issue to its high quality.

On this article, we’re Group Belief Bancorp, whose annual revenues are hardly over $225 million. For a inventory to be categorised as a blue chip one, our situation is that it numbers at the very least 10 years of consecutive annual dividend will increase. We imagine that such a observe document displays an organization’s skill to generate regular development and lift its dividend, even in a recession.

With 41 years of consecutive annual dividend will increase, Group Belief Bancorp has definitely confirmed its skill to develop its dividend by way of numerous durations of harsh financial situations. Thus, we contemplate it a real blue chip inventory regardless of its admittedly small market cap of simply $775 million.

To browse a whole bunch of high quality firms, we created a listing of 350+ blue-chip shares which you’ll obtain by clicking beneath:

Along with the Excel spreadsheet above, we are going to individually assessment the highest 50 blue chip shares as we speak as ranked utilizing anticipated complete returns from the Certain Evaluation Analysis Database.

This installment of the 2022 Blue Chip Shares In Focus collection will analyze Group Belief Bancorp, Inc. (CTBI).

Enterprise Overview

Group Belief Bancorp is a neighborhood financial institution, operating 84 department areas in 35 counties in Kentucky, Tennessee, and West Virginia. It’s the second-largest financial institution holding firm in Kentucky, with a market cap of simply $775 million at the moment.

The corporate engages in a broad vary of economic and private banking and belief and wealth administration actions. These embody accepting time and demand deposits, originating loans to companies and people, offering money administration providers, issuing letters of credit score, renting secure deposit packing containers, and offering funds switch providers, amongst others.

Group Belief Bancorp operates with a $5.4 billion stability sheet. As of June thirtieth, complete shareholders’ fairness stood at $653.3 million, and belief property beneath administration have been $3.6 billion, together with CTB’s funding portfolio totaling $1.5 billion.

As a result of its small market cap, Group Belief Bancorp doesn’t belong to the S&P 500 index, and therefore, it’s not thought-about a Dividend Aristocrat regardless that it has raised its dividend for 41 consecutive years.

Group Belief Bancorp’s newest outcomes demonstrated the financial institution’s potential to publish reslilent numbers even throughout a troublesome buying and selling setting. Its Q2-2022 internet curiosity earnings edged up 2.0%, because of mortgage development. The financial institution’s non-interest earnings decreased -by 7% over the prior 12 months’s quarter, however the decline was largely attributable to modifications within the valuation of mortgage servicing rights.

Furthermore, the financial institution elevated its provision for credit score losses by $0.1 million, whereas it had recovered provisions of $4.3 million within the prior 12 months’s quarter. General, similar to within the earlier quarter, the financial institution confronted a troublesome comparability over its blowout outcomes final 12 months, and thus, its earnings-per-share dipped by 15%, from $1.34 to $1.14. However, it exceeded the analysts’ consensus by $0.04. It’s vital to notice that many of the development final 12 months resulted from the reversion of provisions for mortgage losses, and therefore traders ought to anticipate decrease earnings in 2022. Accordingly, we anticipate EPS to land near $4.40 in fiscal 2022, implying a year-over-year decline of 10.9%.

This doesn’t translate to a deterioration within the firm’s efficiency, nonetheless.

Supply: SEC filings, Creator

Progress Prospects

Excluding the document 12 months 2021, wherein Group Belief Bancorp posted blowout earnings because of the reversal of mortgage loss provisions recorded in 2020, the financial institution has grown its earnings-per-share at a 4.3% common annual fee over the previous decade and at a 4.7% common annual fee over the past 5 years.

The financial system has recovered from the pandemic, and the Fed has began to boost rates of interest aggressively this 12 months. This ought to be confirmed a tailwind to Group Belief Bancorp. Nevertheless, the non-recurring declines within the tax fee of the financial institution, which fueled an amazing portion of the underside line development in 2018 and 2019, is not going to be significant development drivers anymore.

Consequently, we don’t anticipate the corporate to speed up its development sample within the upcoming years. By taking a prudent strategy, we anticipate Group Belief Bancorp to develop its earnings per share at a 2.0% common annual fee over the subsequent 5 years.

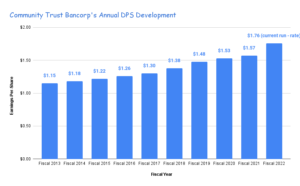

Relating to its dividend, Group Belief Bancorp has grown its dividend-per-share for 41 consecutive years because of prudent capital administration and of constant give attention to shareholder returns. The ten-year dividend-per-share compound annual development fee stands at 2.61%. This isn’t a passable development fee, and albeit, it barely counterbalances the long-term inflation common. Nevertheless, traders can discover consolation within the rising payouts and anticipate that the dividend can continue to grow for many years to come back if the financial institution retains its present prudent administration.

Supply: SEC filings, Creator

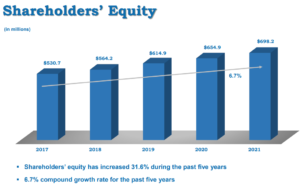

It’s additionally value noting that the dearth of extra aggressive dividend development doesn’t imply that shareholder worth creation is just not maximized. With the corporate retaining a considerable portion of earnings, it has been in a position to develop shareholders’ fairness (e book worth) at a momentous fee through the years.

Supply: Investor Presentation

Aggressive Benefits & Recession Efficiency

Group Belief Bancorp proved that it was nicely managed within the Nice Recession. Within the worst monetary disaster of the final 80 years, when most banks reduce their dividends, this financial institution remained worthwhile and continued elevating its dividend. The COVID-19 pandemic in 2020 brought on an -8% lower within the earnings-per-share of Group Belief Bancorp. Nonetheless, this enterprise efficiency is superior to that of most different banks, because of the conservative mortgage portfolio. To offer a perspective, the financial institution has reported common internet mortgage charge-offs of solely 0.02% within the final 4 quarters, additional demonstrating its total qualities.

You’ll be able to see a rundown of Group Belief Bancorp’s earnings-per-share from 2007 to 2011 beneath:

2007 earnings-per-share of $2.20

2008 earnings-per-share of $1.40

2009 earnings-per-share of $1.51

2010 earnings-per-share of $1.97

2011 earnings-per-share of $2.31

Whereas earnings-per-share fell by 36.4% in 2008, the corporate shortly recovered. By 2011, earnings-per-share have been nicely above the 2007 stage.

General, we imagine that Group Belief Bancorp’s dividend ought to stay secure even throughout a chronic recession. In the course of the previous 5 years, the corporate’s dividend payout ratio has averaged near 40%.

Primarily based on our anticipated earnings-per-share for fiscal 2022 and the present dividend-per-share run-rate, the payout ratio stands at exactly 40% as nicely. Regardless of the ample room to develop the dividend at a a lot quicker tempo, we imagine that the financial institution will keep the payout ratio near the present ranges as a part of its prudent technique, nonetheless.

Valuation & Anticipated Returns

Group Belief Bancorp is presently buying and selling at a price-to-earnings ratio of 9.5, which is decrease than its 10-year common price-to-earnings ratio of 12.6. Regardless of its constant profitability and total qualities, the market possible expects minimal development within the coming years, which explains the low cost. Nonetheless, we imagine that income-oriented traders are prone to respect the corporate’s 4.0%, particularly in the course of the present shaky macroeconomic setting. Together with the truth that rising charges ought to profit the corporate, we imagine that the inventory might expertise valuation tailwinds to a P/E of 12.

If the price-to-earnings a number of expands from 9.5 to 12, future returns could be boosted by4.7% per 12 months over the subsequent 5 years. Mixed with our EPS & DPS development charges, in addition to the present dividend yield, we challenge annualized returns might quantity to 9.8% by way of 2027.

Accordingly, we fee Group Belief Bancorp a purchase.

Remaining Ideas

Group Belief Bancorp is a well-managed financial institution. It accelerated its development sample in 2018 and 2019 because of increased rates of interest and its diminished tax fee. It additionally posted document earnings final 12 months because of the reversion of provisions for mortgage losses because the financial system recovered from the pandemic. Whereas internet earnings will decelerate this 12 months because of the absence of final 12 months’s development driver, fiscal 2022 ought to mark one other 12 months of fantastic backside line numbers.

The corporate additionally incorporates a wholesome payout ratio, which ought to maintain dividend funds and presumably dividend development even when earnings have been to be materially affected. Group Belief Bancorp thus qualifies as a blue chip inventory to depend on for income-oriented traders, notably given its distinctive dividend development document.

The Blue Chips checklist is just not the one method to shortly display for shares that commonly pay rising dividends.

Thanks for studying this text. Please ship any suggestions, corrections, or inquiries to [email protected].

:max_bytes(150000):strip_icc()/What-difference-between-standard-Error-means-and-standard-deviation_color-1c203133aca641aca0d03936d9558693.jpg)

/what-difference-between-magnum-cum-laude-and-summa-cum-laude_V2-3ae02babdc714ea9adaeec0f0a6bf1a5.png)

{kind=link}