Printed on August 4th, 2022 by Josh Arnold

Berkshire Hathaway (BRK.B) has an fairness funding portfolio value greater than $360 billion, as of the top of the primary quarter of 2022, making it one of many largest traders on this planet.

Berkshire Hathaway’s portfolio is full of high-quality shares, and customarily ones that pay dividends. Nevertheless, in recent times, Buffett has confirmed prepared to go exterior the standard listing of firms for Berkshire to purchase. Certainly, the corporate now owns some hyper-growth names, and ones that aren’t but worthwhile.

You possibly can study from Warren Buffett’s inventory picks to seek out ones to your portfolio. That’s as a result of Buffett (and different institutional traders) are required to periodically present their holdings in a 13F Submitting.

You possibly can see all Warren Buffett shares (together with related monetary metrics like dividend yields and price-to-earnings ratios) by clicking on the hyperlink beneath:

Notice: 13F submitting efficiency is completely different than fund efficiency. See how we calculate 13F submitting efficiency right here.

As of March thirty first, 2022, Berkshire owned nearly 2.2 million shares of RH (RH), for a market worth exceeding $600 million. That makes Berkshire a large proprietor of RH at nearly 9% of the corporate’s float, though the place is simply 0.2% of the corporate’s whole fairness funding portfolio.

On this article, we’ll look at the enterprise of RH, in addition to its future development prospects and anticipated whole returns.

Enterprise Overview

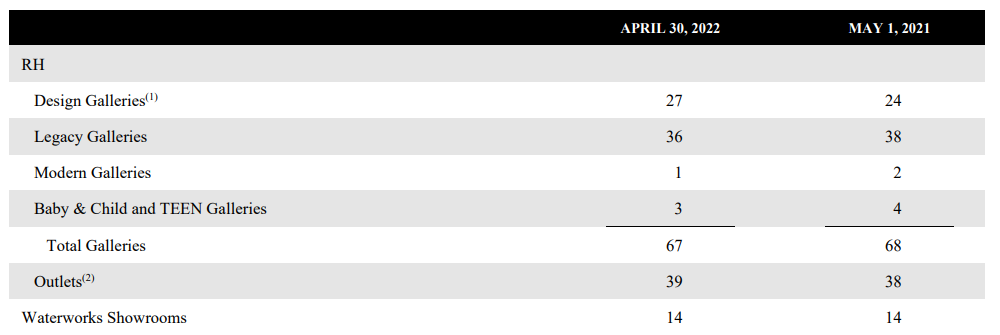

RH is a retailer within the residence furnishings sector, that operates primarily within the US. The corporate sells furnishings, lighting, rugs, bathware, residence décor, out of doors and backyard, and extra by its retail shops, Supply Books, and its digital properties. The corporate has 67 Galleries, that are large-format shops, 39 outlet shops, that are smaller-format, and 14 Waterworks showrooms, that are bathtub and kitchen shops. RH’s shops may be discovered within the US, Canada, and the UK.

Supply: Q1 earnings launch

RH was based in 2011, generates about $3.6 billion in annual income, and trades in the present day with a market cap of $6.9 billion. RH has by no means paid a dividend to shareholders.

RH reported first quarter earnings on June 2nd, 2022, and whereas the corporate beat expectations on each income and revenue by broad margins, shares fell on steerage. Complete income was up 11% year-over-year to $957 million, whereas adjusted earnings-per-share soared 59% to $7.78. Income was $33 million forward of estimates, whereas earnings have been a staggering $2.42 forward of expectations.

Adjusted gross margins have been up 480 foundation factors year-over-year to 52.1%, offering a lot of the gasoline for the earnings beat. Product margins have been up 390 foundation factors, as the corporate resisted the necessity to promote to maneuver product. The corporate famous that whereas its rivals are selling and it might lose share consequently, given its standing as a luxurious model, RH is prepared to cede share briefly to protect the model and long-term pricing energy.

Adjusted working margin rose 210 foundation factors to 24.7% of income. On a greenback foundation, adjusted earnings have been up 50% to $213 million, with the distinction to the per-share achieve of 59% being share repurchases.

RH famous first quarter income was a report for the corporate, and up 98% towards the identical interval in 2020.

RH additionally famous that SG&A prices are briefly larger for the primary three quarters of this 12 months, because it returns to mailing Supply Books after a hiatus, and as its newer shops are opened and start producing income. The corporate famous elevated SG&A prices in Q1, and forecasts for a similar for quarters two and three. This hurts revenue margins, however the firm mentioned it ought to move.

Free money move in Q1 was $107 million, and the corporate ended the quarter with $166 million in web debt, with $2.24 billion in money on the steadiness sheet. In the course of the quarter, RH spent $481 million to repurchase $180 million in excellent convertible notes, terminate all the 3.4 million excellent warrants, and unwind remaining bond hedges. RH has $101 million in convertible notes excellent now because it seeks to scale back potential dilution of shareholders down the highway.

Supply: Q1 earnings launch

This desk reveals the potential affect to the share depend ought to the corporate not repurchase remaining excellent convertible notes and warrants. Because the share value rises, RH is responsible for changing debt and warrants to frequent shares excellent, which might dilute shareholders. This is the reason it’s utilizing money to remove these earlier than they’re exercised.

Subsequent to Q1 outcomes, the corporate pretty rapidly decreased steerage for this 12 months. It now expects to see income development of 0% to 2% this 12 months, and adjusted working margin of 23% to 24%. Nevertheless, administration additionally mentioned these headwinds must be non permanent as demand resets from a blockbuster run prior to now two years.

We anticipate to see $23.25 in earnings-per-share for this fiscal 12 months after the steerage replace.

Progress Prospects

RH’s development prior to now has been nothing in need of exemplary, but in addition extraordinarily risky. The corporate posted its first revenue as a publicly-traded firm in 2014, with a achieve of 45 cents per share. Nevertheless, earnings deteriorated into an annual loss by 2018, earlier than hovering to $22.13 in fiscal 2022, and expectations for the same worth this 12 months. Clearly, this type of development is unsustainable, however we do see a vibrant future for RH nonetheless.

We see earnings development as muted this 12 months given the steerage replace, and the challenges round the truth that earnings greater than doubled from 2020 to 2021. Nevertheless, going ahead we estimate 6% annual earnings-per-share development.

We imagine income can sustainably develop within the low- to mid-single digits yearly. As well as, the corporate continues to make profitability enhancements by trimming unprofitable product strains and sustaining its pricing energy.

We additionally see the corporate’s huge share repurchase program as fueling features to earnings-per-share by way of a decrease float. The corporate had $2.45 billion in share repurchases licensed on the finish of the fiscal first quarter, towards a present market cap of below $7 billion. Ought to these repurchases come to fruition, it might be an enormous tailwind to earnings-per-share within the years to come back.

Aggressive Benefits & Recession Efficiency

RH’s aggressive benefit is definitely in its model title recognition as a luxurious retailer, pushed by its excellent forefront design crew. RH has made a reputation for itself prior to now decade as a premiere luxurious residence furnishings supplier, and it reveals with its world-beating revenue margins. RH’s mannequin is designed round its shops which can be meant to be immersive procuring experiences, in contrast to warehouse-style furnishings shops.

Nevertheless, given RH is – on the finish of the day – a furnishings and residential items retailer, it’s extremely vulnerable to recessions. RH serves high-end shoppers so it’s marginally insulated from client spending declines, however it’s nonetheless fairly susceptible to financial slowdowns, and potential patrons of the inventory ought to concentrate on this threat.

Valuation & Anticipated Returns

Shares commerce for simply over 12 occasions this 12 months’s earnings estimate, which is extraordinarily low-cost by RH’s personal historic requirements, and certainly, for furnishings retailers basically. RH has averaged 19 occasions earnings-per-share prior to now 5 years, and we assess truthful worth at 17 occasions earnings. This conservative estimate is given the present uncertainty round whether or not the slowdown in client spending will persist.

Even so, the valuation might drive a 6.5% tailwind to whole returns within the coming years. RH doesn’t pay a dividend, so the steadiness of returns would come from 6% projected annual earnings development. All informed we see 12%+ whole annual returns, and due to this fact fee the inventory a speculative purchase.

Last Ideas

Whereas RH has its personal set of challenges given its merchandise are extremely discretionary, we see the corporate as a robust grower that could be very moderately priced. RH has the potential to purchase again an unlimited proportion of the float within the years to come back, and its benefit as a luxurious items supplier means its revenue margins are best-in-class. Whereas it’s vulnerable to client spending slowdowns, the inventory is priced such that we anticipate double-digit returns within the years to come back.

Different Dividend Lists

Worth investing is a invaluable course of to mix with dividend investing. The next lists comprise many extra high-quality dividend shares:

Thanks for studying this text. Please ship any suggestions, corrections, or inquiries to [email protected].

:max_bytes(150000):strip_icc()/What-difference-between-standard-Error-means-and-standard-deviation_color-1c203133aca641aca0d03936d9558693.jpg)

/what-difference-between-magnum-cum-laude-and-summa-cum-laude_V2-3ae02babdc714ea9adaeec0f0a6bf1a5.png)

{kind=link}