Printed on August eighth, 2022, by Felix Martinez

There isn’t any precise definition for blue chip shares. We outline it as a inventory with at the least ten consecutive years of dividend will increase. We imagine a longtime observe report of annual dividend will increase going again at the least a decade exhibits an organization’s skill to generate regular development and lift its dividend, even in a recession.

Because of this, we really feel that blue chip shares are among the many most secure dividend shares buyers should purchase.

With all this in thoughts, we created an inventory of 350+ blue-chip shares, which you’ll be able to obtain by clicking beneath:

Along with the Excel spreadsheet above, we are going to individually assessment the highest 50 blue chip shares right now as ranked utilizing anticipated whole returns from the Positive Evaluation Analysis Database.

This text will analyze Leggett & Platt (LEG) as a part of the 2022 Blue Chip Shares In Focus sequence.

Enterprise Overview

Leggett & Platt is a diversified manufacturing firm. It was based in 1883 when an inventor named J.P. Leggett created a bedspring that was superior to the present merchandise at the moment. The corporate designs and produces engineered elements and merchandise present in most houses and cars.

It operates its enterprise by way of three segments: Bedding Merchandise, Specialised Merchandise, Furnishings, Flooring, and Textile Merchandise. Serving a broad suite of shoppers worldwide, Leggett & Platt’s merchandise embrace bedding elements, automotive seat help and lumbar techniques, specialty bedding foam, and personal label completed mattresses, elements for house furnishings and work furnishings, flooring underlayment, adjustable beds, and varied different merchandise.

Supply: Investor Presentation

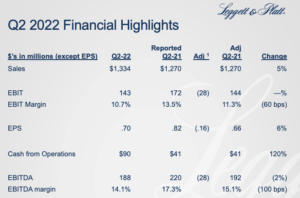

Leggett & Platt reported its second quarter and 6 months earnings outcomes on August 1st. Quarterly income of $1.33 billion rose 5% year-over-year. Adjusted earnings-per-share of $0.70 fell 15% from the identical quarter the earlier 12 months. Quantity was down 6%, primarily from demand softness in residential finish markets, partially offset by industrial finish markets and automotive development. Uncooked material-related promoting value will increase added 13% to gross sales.

Income is up 10% for the six months of the fiscal 12 months, however web earnings is down 7% in comparison with the primary six months of 2022. General, earnings per share are down 7% for the six months year-over-year, from $1.46 to $1.36 per share. Additionally, the corporate repurchased 1.0 million shares at a median value of $35.01

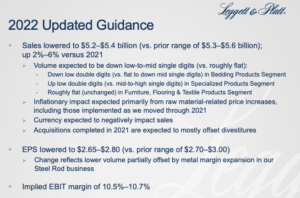

Administration additionally offered steering for the present fiscal 12 months, forecasting revenues of $5.2 billion to $5.4 billion, which shall be up 2% to six% in comparison with 2021. Additionally, they anticipate EPS of $2.65 to $2.80. Based mostly on the midpoint, this could signify a 2.1% lower versus 2021.

Supply: Investor Presentation

Progress Prospects

Progress at Leggett & Platt will depend on a multi-faceted method, together with common annual income development (each natural and thru acquisitions), new merchandise and packages, increasing addressable markets, and making certain that acquisitions are strategic. Additional, share repurchases and price controls might additionally increase the underside line.

Probably the most strategic acquisition was when the corporate spent $1.25 billion to buy Elite Consolation Options. Elite Consolation Options’ foam bedding operations complement Leggett & Platt’s present mattress capabilities and infrastructure. In 2021, LEG made three small acquisitions that expanded its capabilities in Worldwide Bedding, Aerospace, and Work Furnishings.

Over the previous ten years, the corporate’s earnings have been rising at a Compound Annual Progress Price(CAGR) of seven.3%. Over the previous 5 years, earnings have had a CAGR of two.9%. So, earnings development has been reducing lately. Nonetheless, total, earnings are rising.

We anticipate the corporate to proceed to develop earnings at a barely larger price in comparison with its five-year nice price of 5% over the following 5 years.

Supply: Investor Presentation

Aggressive Benefits & Recession Efficiency

Leggett & Platt has established a large financial “moat,” that means it has a number of operational benefits which maintain rivals at bay. First, the corporate enjoys a management place within the business, which permits for scale.

Leggett & Platt additionally profit from working in a fragmented business, which makes it simpler to determine a dominant place. There are few or no, massive rivals in most of its product markets. And when a smaller competitor does obtain vital market share, Leggett & Platt can merely purchase them, because it did with Elite Consolation Options.

Leggett & Platt additionally has an in depth patent portfolio, which is important in maintaining competitors at bay.

These aggressive benefits assist Leggett & Platt preserve wholesome margins and constant profitability. That stated, the corporate didn’t carry out properly in the course of the Nice Recession.

You’ll be able to see a rundown of Leggett & Platt’s earnings-per-share from 2007 to 2011 beneath:

2007 earnings-per-share of $1.20

2008 earnings-per-share of $0.88 (27% lower)

2009 earnings-per-share of $0.86 (2% lower)

2010 earnings-per-share of $1.16 (35% improve)

2011 earnings-per-share of $1.20 (3% improve)

The corporate has a suitable stability sheet. The corporate sports activities a debt-to-equity ratio of 0.9 and a long-term debt-to-capital ratio of 42.8. Additionally, the curiosity protection ratio is 5.0, which is an efficient ratio, that means that the corporate covers the curiosity on its debt properly. General, the corporate sports activities an S&P credit standing of BBB, an funding grade ranking.

Valuation & Anticipated Returns

As beforehand talked about, LEG inventory has a powerful dividend historical past. The corporate has elevated its dividend for half a century. Leggett & Platt has traditionally generated loads of money movement to distribute vital money to buyers and put money into development initiatives.

It additionally has a strong present dividend yield of 4.2%. That is greater than triple the ~1.3% common yield of the broader S&P 500 Index.

Leggett & Platt is anticipated to generate earnings-per-share of $2.70 for 2022. Based mostly on a present inventory value, shares are presently buying and selling at a price-to-earnings ratio of 14.8x earnings.

Whereas the corporate has been a gradual grower over a few years, with an extended dividend historical past, we imagine one thing nearer to fifteen occasions earnings is truthful worth for LEG inventory. As such, this might point out the potential for a significant valuation tailwind over the intermediate-term, to the tune of 1.5% per 12 months if the present P/E expands to fifteen.

For those who mix the 5% anticipated EPS development price, 4.2% beginning dividend yield, and 1.5% potential valuation tailwind, you come to an anticipated annualized whole return of 10.7% over the following 5 years.

Closing Ideas

Leggett & Platt is an organization that has carried out very properly previously, each when it comes to producing earnings development and its decades-long dividend development observe report. As we advance, we imagine that Leggett & Platt’s earnings-per-share development price shall be considerably decrease, however the firm’s earnings-per-share ought to proceed to develop in the long term.

In line with our current estimates, Leggett & Platt will supply compelling whole returns over the approaching years. We price the inventory a purchase at present costs beneath our truthful worth estimate.

The Blue Chips listing shouldn’t be the one approach to rapidly display for shares that often pay rising dividends.

Thanks for studying this text. Please ship any suggestions, corrections, or inquiries to [email protected].

:max_bytes(150000):strip_icc()/What-difference-between-standard-Error-means-and-standard-deviation_color-1c203133aca641aca0d03936d9558693.jpg)

/what-difference-between-magnum-cum-laude-and-summa-cum-laude_V2-3ae02babdc714ea9adaeec0f0a6bf1a5.png)

{kind=link}