Spencer Platt/Getty Pictures Information

With the inventory market sliding as soon as once more, some attention-grabbing names are popping up on the 52-week lows lists. One such potential discount is V.F. Corp. (NYSE:VFC), which has dropped by half as a result of provide chain points and worries round client spending.

Folks is perhaps scared off since it’s an attire firm, and clothes is understood for being a cyclical trade. Nonetheless, VF collects tons of manufacturers, often shopping for at low costs, after which operates them till they will promote or in any other case monetize them at extra enticing valuations. This drastically reduces the boom-and-bust issue that’s usually seen within the trade the place firms depend on only one or two mainstay manufacturers.

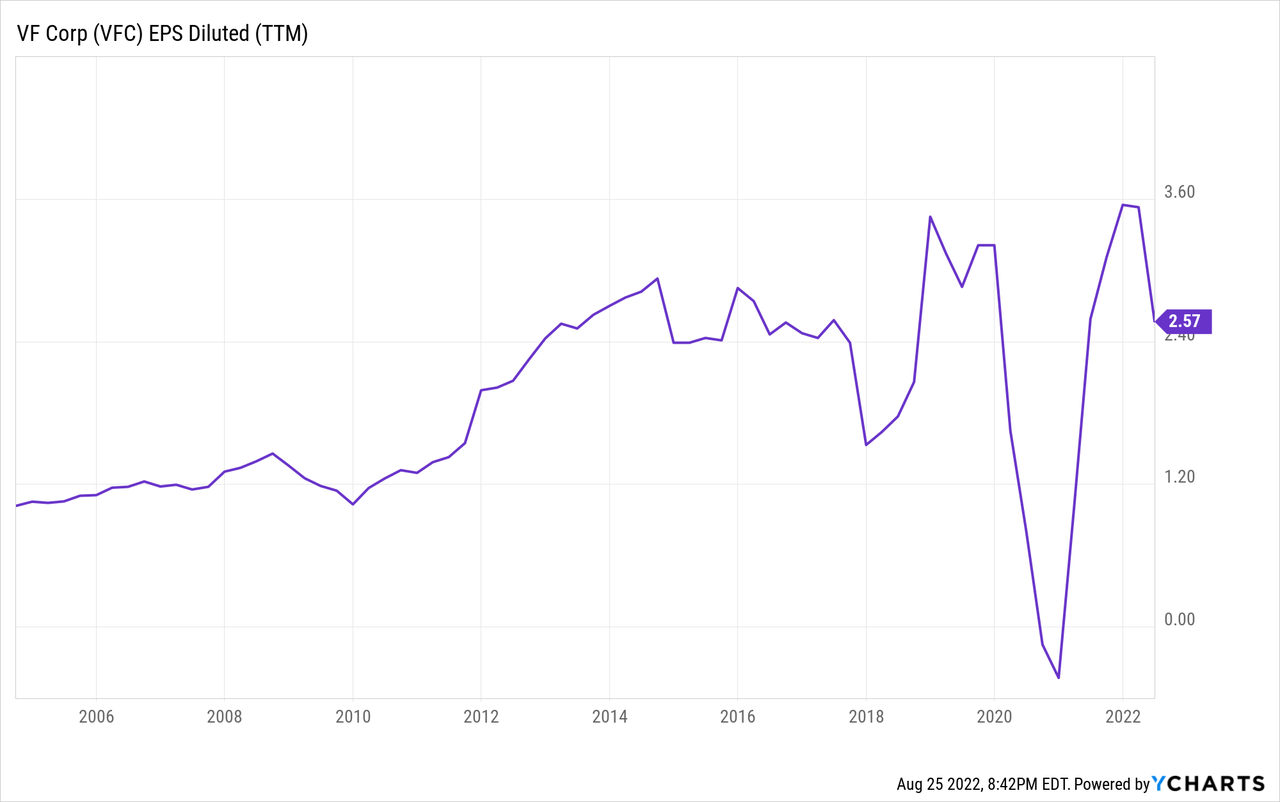

In any case, given its holdings throughout a ton of various attire strains, V.F. Corp. has produced constant earnings development for many years and was again to report excessive earnings at the beginning of 2022:

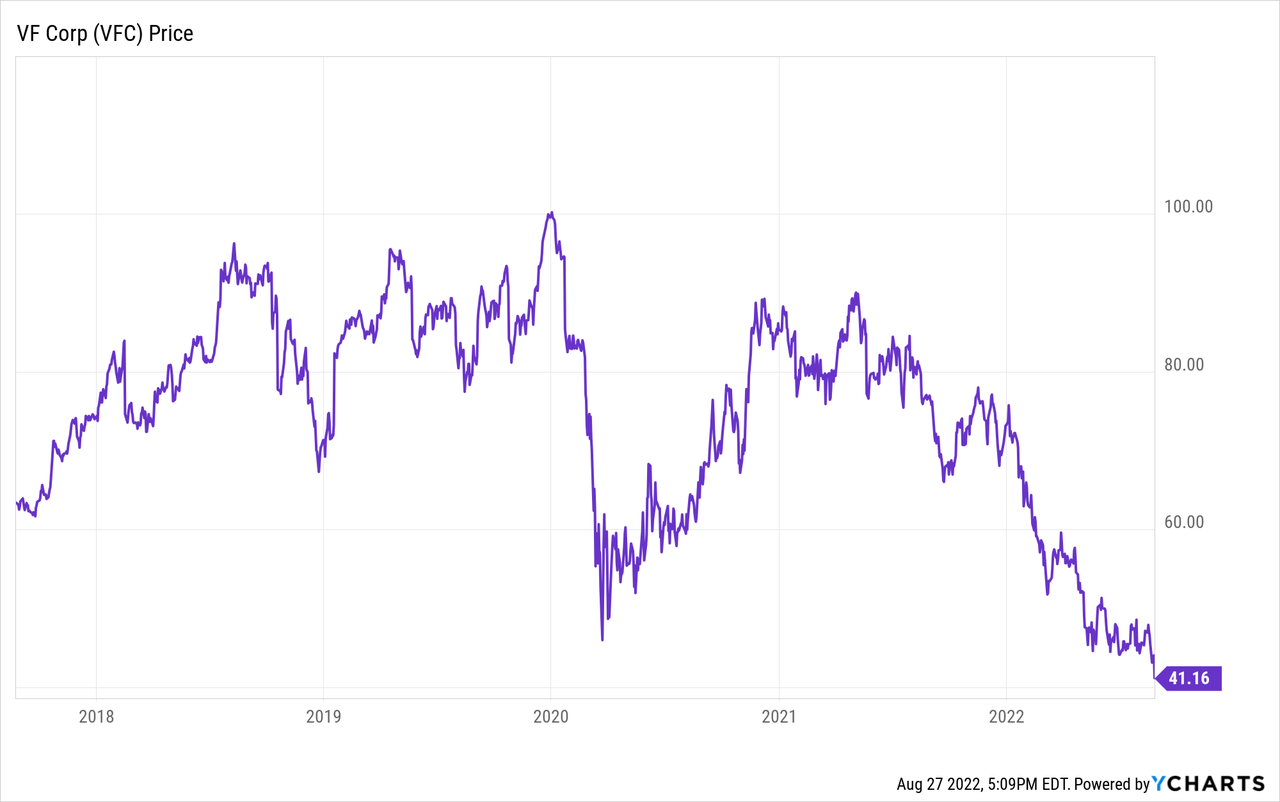

But, the inventory worth has gone off a cliff and is now promoting under pandemic lows:

Previously, we needed to pay not less than 20x and infrequently nearer to 25x earnings for V.F. Corp. inventory. Now it is promoting for 13x earnings. That is an enormous low cost to regular. Might it get even cheaper? Positive, it might. If the S&P 500 drops to new lows later this yr, as I feel within reason probably, VFC inventory would most likely go along with it.

The S&P 500 is at the moment round 23x earnings with V.F. Corp. at 13. In a world the place the S&P pulls again to, say, 18x earnings, it is not out of the query that VFC inventory might fall to 10 or 11 instances earnings. Sooner or later, nonetheless, valuation ought to kick in as a strong flooring.

Shares are already means down right here even with little underlying purpose for struggling greater than the S&P 500 particularly. Regardless of earnings being round flat for now and set to development again up quickly, shares are off 50% from final yr already.

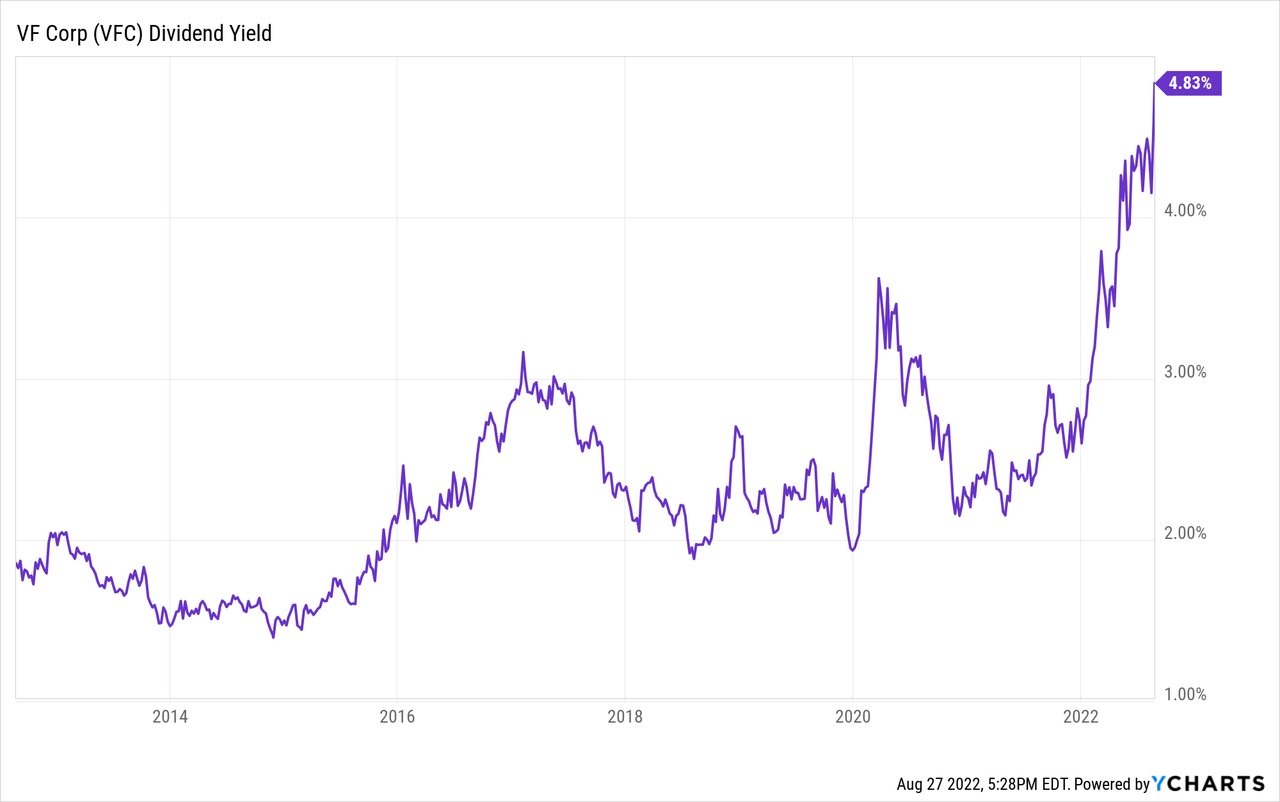

The corporate can also be a Dividend Aristocrat with a protracted observe report of constant dividend hikes. Now, the yield has blown out from its ordinary 2-3% vary as much as 4.8%:

Why Is The Market So Involved?

There’s one particular damaging that has hit solely V.F. Corp recently. That’s {that a} decide discovered that V.F. Corp. underpaid taxes associated to the acquisition of Timberland, and thus is on the hook for as a lot as $850 million in relation to that. This works out to lower than $3/share for VFC inventory which isn’t an enormous drawback within the grand scheme of issues. Nonetheless, it has brought about debt score downgrades and restricted the agency’s potential to execute a share buyback now when costs are most advantageous.

Extra broadly, the damaging financial and inflationary atmosphere is having an impact on the entire attire sector and VF particularly. The corporate simply trimmed its FY ’23 earnings steerage from $3.35 per share to $3.10. This is able to nonetheless symbolize year-over-year development and is hardly consistent with a inventory that’s down by greater than half. Nonetheless, VF is seeing some headwinds now and issues might worsen earlier than they get higher.

Moreover, there have been considerations about V.F. Corp.’s development charge even previous to the pandemic.

The corporate paid out extra in mixed dividends and share buybacks than it generated in free money circulate over the previous decade. That is fantastic for a mature steady firm, nevertheless it’s not one thing you anticipate to see from a agency that’s rising a lot. And, as is, V.F. Corp.’s dividend development charge has trailed off markedly, which is not too shocking given the slowdown within the momentum of its enterprise operations.

A few of that is clouded by the spin-off of Kontoor Manufacturers (KTB), which was the corporate’s denims enterprise. Not solely was did that cut back V.F. Corp.’s general profitability and money circulate, Kontoor was a very low-growth and excessive money circulate section of the enterprise. Kontoor manufacturers initially spun off at a 7% dividend yield, highlighting simply how a lot of a money circulate machine it was and is.

So that you may give V.F. Corp. one thing of a move for the particular wrestle in elevating the dividend at greater than a nominal charge recently. Nonetheless, if administration goes to return to the extra strong development days of outdated, it must make extra shrewd acquisitions or in any other case unlock new upside potentialities.

I give firms with a differentiated enterprise mannequin and many years of confirmed success the advantage of the doubt throughout a down interval. That being the case, the skeptics have an inexpensive argument right here. If the numbers do not begin wanting higher through the subsequent financial enlargement, we’ll must revisit this level.

VF’s Earnings Might Not Even Fall That Far

With VFC’s inventory worth down 60% from its all-time excessive, you’d think about that the corporate was going by means of a serious disaster. And but, the numbers simply do not mirror that. In any respect.

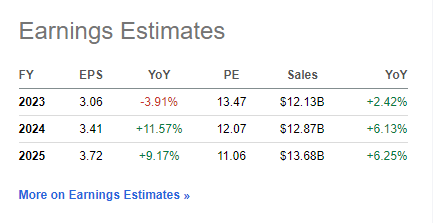

Listed here are earnings estimates for the corporate going ahead:

VFC earnings estimates (Looking for Alpha)

For fiscal yr 2023, analysts see revenues rising 2% whereas earnings dip a mere 4%. In 2024, analysts see gross sales development returning to the mid-single digits whereas earnings development strikes again to 10% yearly. This isn’t what you’d anticipate to see given the abysmal motion in V.F. Corp.’s inventory worth.

The promoting has accelerated in latest days because the market has turned downward once more, together with analysts elevating considerations over VF’s near-term outlook. I do not fault the analysts for doing their job; the corporate faces headwinds within the short-term. There is not any denying that. However for development and earnings buyers that need to purchase Dividend Aristocrats, a lot of the flexibility to get good costs comes from shopping for throughout instances like this when short-term merchants react sharply to financial swings.

V.F. Corp.’s Backside Line

The inflation scenario is inflicting issues for all kinds of client discretionary merchandise, and attire is not any exception. In a time of penny-pinching, a agency like VF may have short-term points in passing alongside the complete impact of inflation to customers.

Nonetheless, as its Dividend Aristocrat standing proves, V.F. Corp has proven itself to be remarkably able to enduring financial swings with out ruining its backside line. The corporate’s broad steady of various manufacturers provides it a giant benefit right here because it has a wide range of totally different kinds, developments, and worth factors with which to fulfill altering client conduct.

I would additionally notice that the dividend is well-supported. With the annual dividend at $2.00 per share, there may be important wiggle room between earnings and the present dividend charge as nicely.

V.F. Corp. shares had been arguably fairly overvalued once they hit $100 in January of 2020. I doubt we’ll see that worth once more for a while. That mentioned, the pendulum has swung too far within the different course. Determine an 18x a number of on fiscal yr 24’s projected $3.41 of earnings, and that will get to a inventory worth of $61, or 50% upside from right here. Throw in a 4.8% dividend yield with annual will increase, and VFC inventory must be a robust performer for the typical development and earnings portfolio.

:max_bytes(150000):strip_icc()/What-difference-between-standard-Error-means-and-standard-deviation_color-1c203133aca641aca0d03936d9558693.jpg)

/what-difference-between-magnum-cum-laude-and-summa-cum-laude_V2-3ae02babdc714ea9adaeec0f0a6bf1a5.png)

{kind=link}