gremlin

After my latest article on Dolphin Leisure (NASDAQ:DLPN) shares went on to understand by virtually 50% solely to dump once more to new 52 week lows round $2.50. Whereas I’m sustaining a long run bullish stance on the corporate, I do discover many different alternatives extra compelling on this market. On this piece, I wish to present readers with the latest decidedly blended developments.

As a reminder, Dolphin is a number one impartial leisure advertising and premium content material growth firm. It consists of the supergroup of firms together with 42West, Shore Hearth, Viewpoint, Be Social and The Door for advertising popular culture. Moreover, there’s Dolphin 2.0 the place the corporate is utilizing popular culture to market belongings that it owns stakes in.

Dolphin Tremendous Group (Firm slide deck)

In my earlier piece, I made the case on a sum of the components foundation that DLPN was doubtless undervalued:

There’s main upside in each single a part of the enterprise, be it Dolphin 1.0 or the person bets inside 2.0. My conservative estimates see little draw back at this worth with as much as 100% upside primarily based on 2022 projections and the possession stakes DLPN has amassed.

Financials heading in the right direction however uninspiring

At the start, DLPN has regained compliance with the SEC and NASDAQ itemizing necessities by publishing its 10-Ok and different financials. Because it seems, the corporate quickly after dismissed and changed its auditor BDO USA with Grant Thornton. Individuals accustomed to the auditing course of informed me that Grant Thornton was a a lot better match for Dolphin. I’m fairly assured the late filings over the corporate’s historical past will likely be behind Dolphin now after the transfer to Grant Thornton.

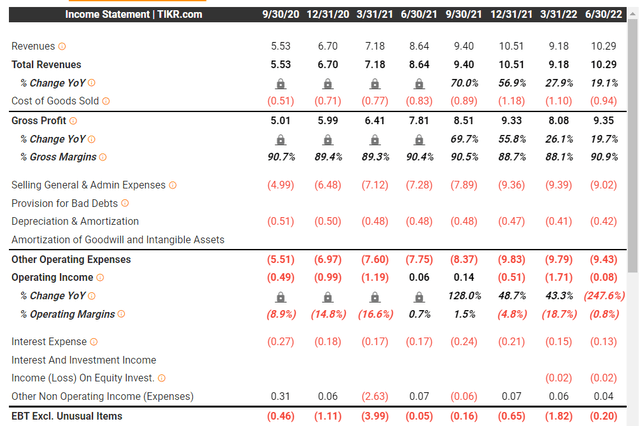

Furthermore, the corporate is making good progress in direction of profitability. I had assumed 25% income progress for 2022, which is roughly right up to now in H1. EBITDA was additionally first time optimistic in Q2 at round $0.5M. Nonetheless, the CEO said “we’re on tempo to cross $40.0 million in annual income this yr”, which might solely symbolize about 15% progress and with bills rising equally, I can’t keep my EBITDA projections of $3-4M for this yr. An enormous a part of that’s the delay in stay occasions and the corporate needs to current its technique for 2023 by year-end.

DLPN earnings stmt (TIKR)

On the LD Micro Invitational XII the corporate offered some extra info relating to these numbers. Notably, adjusted EBITDA of round $2M for 2022 and income exceeding $50M in 2023. I view these as fairly doubtless though I really feel just like the changes do some heavy lifting for 2022. Nonetheless, preserving prices on an analogous trajectory adjusted EBITDA for subsequent yr might comfortably exceed $5M, which compares to the present EV of round $30M. Whereas this alone just isn’t inspiring, Dolphin 2.0 comes on high.

The corporate issued about 1.5m shares or about 18% of excellent shares at costs between $3.47 and $5.15 with a median of about $4.20. Hopefully these funds will likely be put to good use as a result of the dilution at these costs not solely hurts however has actually aggravated shareholders. In complete, Dolphin is allowed to promote $25M value of inventory or about 3M shares. The corporate has further modified the phrases of the convertibles to maintain Invoice above 50% of voting management within the occasion they promote too many shares at too low cost a worth.

Dolphin 2.0 updates

In my prior piece I listed the initiatives and possession stakes as follows:

Fan Jolt, a platform creating memorable interactions between followers and a curated listing of premier expertise to assist their favourite causes: 5% to 10%

Crafthouse Cocktails, a pioneering model of ready-to-drink, all-natural traditional cocktails: 5% to 10%

NFT market: 10%

Flower women, a female-led NFT assortment: 30%

Midnight Theater: 13% (on $1M funding) with choice to extend to 25%

I’m delighted to see Midnight Theater, a state-of-the-art up to date selection theater and restaurant within the coronary heart of Manhattan, having its official opening week and being a hit up to now. It is likely one of the most “tangible” 2.0 initiative, particularly in comparison with NFTs the place Dolphin is creating its pipeline as nicely. They now have 8 collections which can be wholly owned or in partnership with others. Whereas the area has cooled considerably, there may very well be a variety of outcomes for Dolphin right here. Definitely $2M appears doubtless as a low estimate by way of fairness worth to DLPN?

These 3 are charge solely Dolphin 1.0 enterprise.

These 3 are Dolphin 1.0 charge + an undisclosed % of income sharing in any upside.

Dolphin is a accomplice on this model, with presumably a 50/50 break up.

The Flower Women ― A Nice Artwork NFT Assortment by Varvara Alay (flowergirlsnft.com) Dolphins owns 100% of the quickly to be re-released Creature Chronicles.

However the Flower Women and Creature Chronicles launches have been moved from the summer time to the autumn. This isn’t signal up to now, however hopefully administration is correct in assuming “that the native crypto neighborhood will likely be stronger within the coming months”.

Fan Jolt appears lifeless up to now however Crafthouse appears to be going simply high-quality. Then again, the latest Dolphin 2.0 initiative is a multi-year co-production distribution settlement with IMAX for slate of documentary options. The primary venture known as Blue Angels, presently in manufacturing and is anticipated to hit IMAX theatres within the second half of 2023.

Abstract

Clearly the corporate is making good progress in getting worthwhile and cleansing up the steadiness sheet from all types of debt, places and earn-out contingent concerns. Primarily based on some tough estimates the inventory can also be under no circumstances costly on 2023 numbers and the two.0 initiative present extra upside. That being stated, valuing these remains to be a problem and till the corporate is able to disclose extra particulars on them and has confirmed sustainable profitability and earnings progress, it’s in “present me mode”.

A few of the initiatives simply take extra time to return to fruition however seem extraordinarily promising to me, together with Midnight Theater and Blue Angels. Others are extra disappointing, like Fan Jolt advert NFTs.

As highlighted in my prior article, some yellow flags additionally stay just like the Lincoln Park settlement and the truth that the corporate dilutes its shareholders at all-time low costs whereas guaranteeing Invoice’s tremendous voting rights. The jury remains to be out if this can show to be transfer or not, however up to now it appears not beneficial and this is the reason shares are near 52 week lows.

Thus I keep my long run bullish outlook for the corporate particularly since Invoice additionally talked about on the latest name that their 1.0 enterprise wouldn’t be affected by financial slowdown. Nonetheless I’m pairing down my pleasure till I see sturdy working leverage, excessive margin income from Dolphin 2.0 and working metrics of key fairness investments like Midnight Theater.

/what-difference-between-magnum-cum-laude-and-summa-cum-laude_V2-3ae02babdc714ea9adaeec0f0a6bf1a5.png)

:max_bytes(150000):strip_icc()/What-difference-between-standard-Error-means-and-standard-deviation_color-1c203133aca641aca0d03936d9558693.jpg)

{kind=link}