Tim Boyle/Getty Pictures Information

My first expertise with Twinkies, as my dad and mom maintain reminding me once in a while, was after I was two years outdated and we have been visiting my uncle who was pursuing graduate research in upstate New York (this was within the Eighties). We had arrived at our motel late at evening and the one meals my dad and mom might discover have been some Twinkies and Coca-Cola at an area comfort retailer. To today, I nonetheless get pleasure from an occasional twinkie deal with.

The corporate behind Twinkies, Hostess Manufacturers Inc. (NASDAQ:TWNK), is a defensive meals staples firm presently firing on all cylinders because it has been capable of develop each volumes and worth/combine regardless of a difficult macro atmosphere. Though the inventory trades at a premium a number of, I believe that is justified as a result of GARP traits of the corporate’s enterprise.

Firm Overview

Hostess Manufacturers, Inc. (TWNK) is a snacking pure-play that manufactures and sells iconic treats reminiscent of Twinkies, Donettes, CupCakes, and Ding Dongs. The present iteration of the corporate was shaped in 2013, when personal fairness agency Apollo World Administration partnered with client meals and beverage billionaire Dean Metropolous to accumulate the Hostess Manufacturers snack cake belongings out of Chapter 11 chapter. Hostess Manufacturers, Inc. got here to the general public markets in 2016 through a merger with a SPAC sponsored by The Gores Group, one other personal fairness agency.

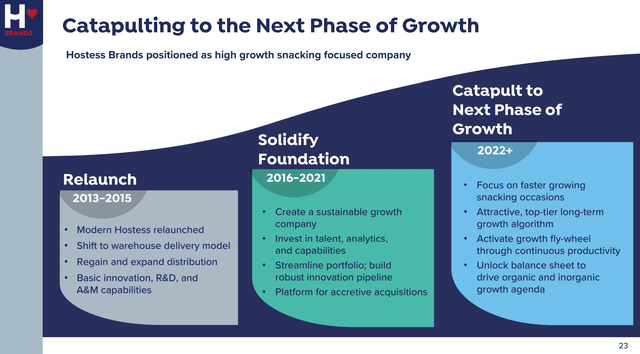

Based on the corporate’s advertising supplies, the primary few years of the brand new Hostess Manufacturers was all about relaunching the merchandise and shifting to a warehouse supply mannequin. Put up the de-SPAC in 2016, the corporate targeted on creating the foundations for sustainable development. Lastly, in the previous couple of quarters, the corporate has begun specializing in rising development via each natural and inorganic channels (Determine 1).

Determine 1 – TWNK Launching Subsequent Part Of Development (TWNK investor day presentation)

Spectacular Monetary Efficiency

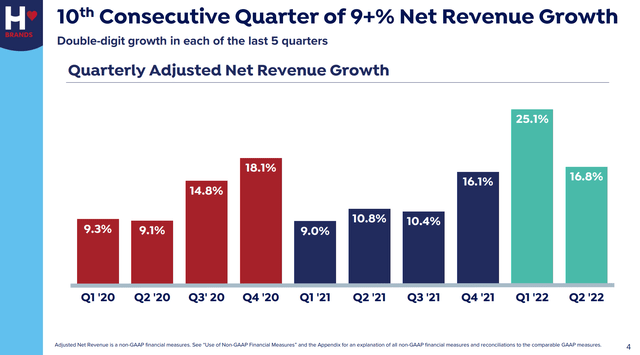

Undeniably, Hostess Manufacturers has delivered extraordinary monetary efficiency in latest quarters. The latest Q2/2022 was the tenth consecutive quarter the place TWNK had reported higher than 9% internet income development (Determine 2).

Determine 2 – TWNK has 10 consecutive quarters of 9%+ income development (TWNK Q2/2022 Presentation)

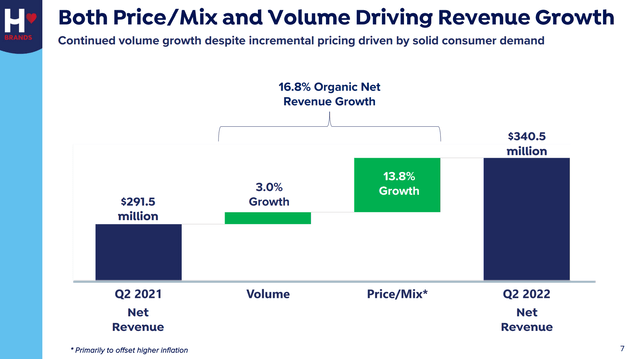

Impressively, Hostess Manufacturers’ development is coming from a mix of quantity and worth/combine, which has allowed the corporate to take care of its industry-leading margins (Determine 3).

Determine 3 – TWNK Q2/2022 YoY Development Breakdown (TWNK Q2/2022 Presentation)

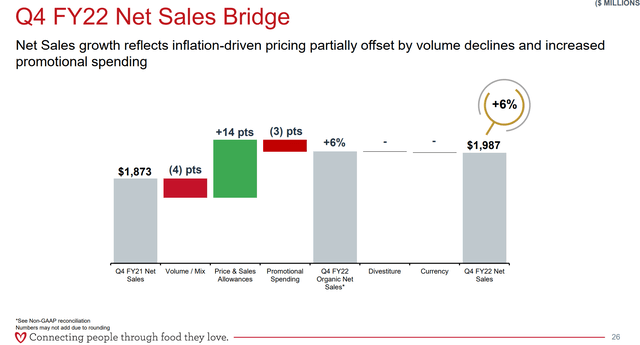

Throughout the patron meals {industry}, it’s exhausting to search out one other firm delivering this stage of economic outperformance within the present difficult macro atmosphere. For instance, if we have a look at Campbell Soup Firm’s (CPB) newest quarter, we will see CPB was capable of take worth actions, however on the expense of volumes (Determine 4). It is a widespread theme throughout the patron meals area, with firms buying and selling off volumes to boost costs and preserve margins.

Determine 4 – CPB This fall/2022 Income Bridge (CPB This fall/2022 Presentation)

Hostess Outperforms By Focusing On Core Snacking Events

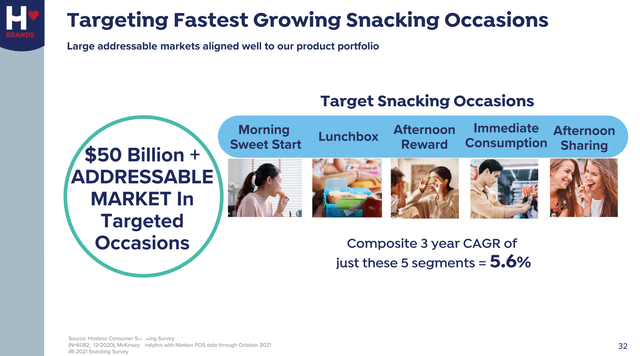

Hostess Manufacturers has been capable of obtain its peer-leading development charges by specializing in the quickest rising snacking events which have a composite 3-yr CAGR development charge of 5.6%. For instance, to focus on the rapid consumption event (i.e. comfort shops), Hostess Manufacturers launched a caffeine-infused ‘Enhance’ Donette. For afternoon sharing, Hostess Manufacturers presents ‘Crispy Minis’ creme wafers.

Determine 5 – TWNK Targets Key Snacking Events (TWNK investor day presentation)

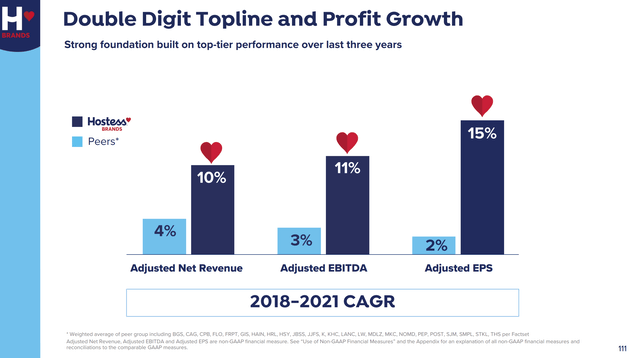

Altogether, Hostess Manufacturers’ targeted product improvements and positioning has allowed it to develop revenues at a 9% CAGR, nearly double the class development charge. Sturdy income development plus working leverage means a ~10% development in revenues can translate into 15% development in EPS (Determine 6).

Determine 6 – TWNK Working Leverage (TWNK investor day presentation)

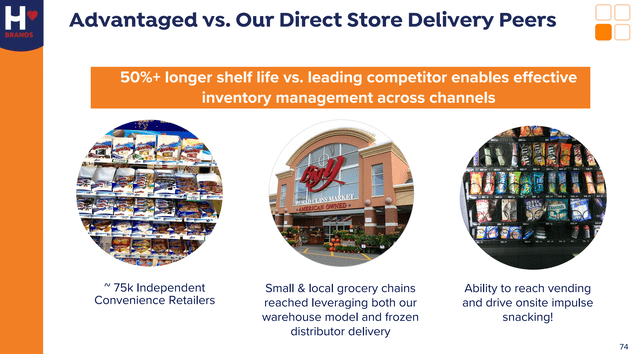

Longer Shelf-Life An Underrated Benefit

An underrated benefit of Hostess Manufacturers merchandise are their 50%+ longer shelf-life vs. friends (city legend has it Twinkies can survive a nuclear battle!). When Hostess Manufacturers relaunched their merchandise in 2013, they made key modifications to the recipes that stretched the shelf-life of a Twinkie from 26 days to 45 days (Determine 7).

Determine 7 – TWNK merchandise have longer shelf life (TWNK investor day presentation)

Longer shelf-life permits Hostess Manufacturers to handle its stock ranges extra successfully than friends and scale back wastage, a big value within the packaged meals {industry}.

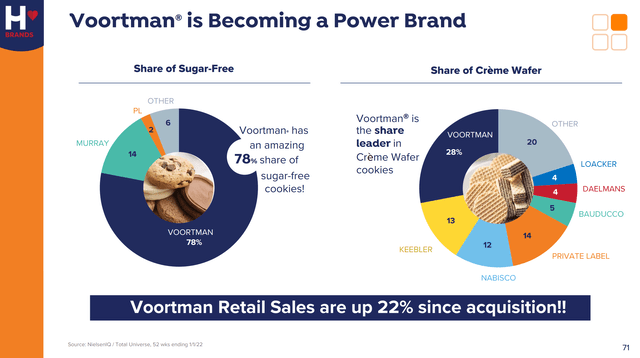

Voortman Is A Development Platform

In December 2019, Hostess Manufacturers acquired Voortman Cookies Restricted for $320 milion. Voortman is understood for making creme wafers and sugar-free cookies. For the reason that acquisition, Voortmans gross sales have elevated 22% underneath the Hostess administration (Determine 8).

Determine 8 – Acquired Voortman cookie enterprise exhibiting robust development (TWNK investor day presentation)

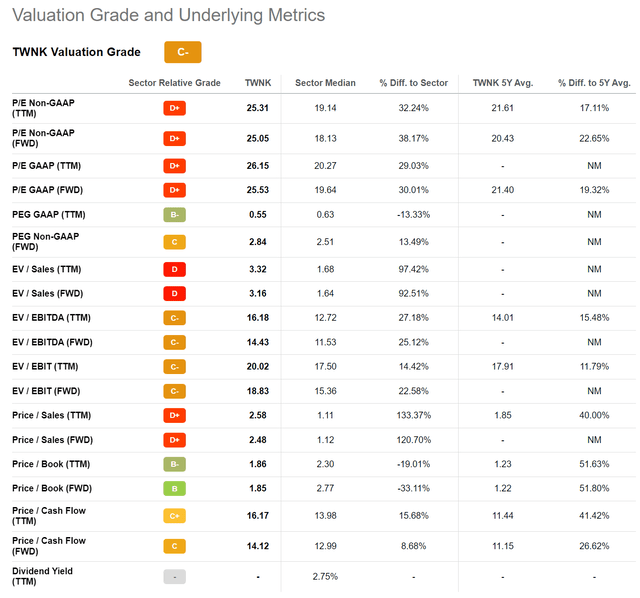

TWNK Trades At A Premium Valuation

By way of valuation, Hostess Manufacturers is presently buying and selling at a Fwd P/E of 25.1x, a premium a number of vs. its client staple friends at 18.1x (Determine 9).

Determine 9 – TWNK Valuation vs. Sector (Searching for Alpha)

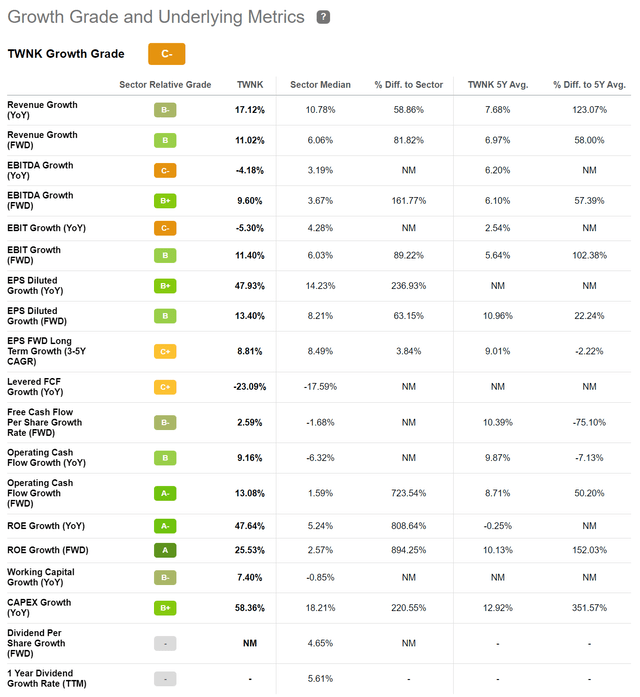

I consider TWNK’s premium a number of might be justified as the corporate has Fwd Revenues and EPS development charges of 11.0% and 13.4%, considerably above the sector’s 6.1% and eight.2% respectively (Determine 10).

Determine 10 – TWNK Development vs. Sector (Searching for Alpha)

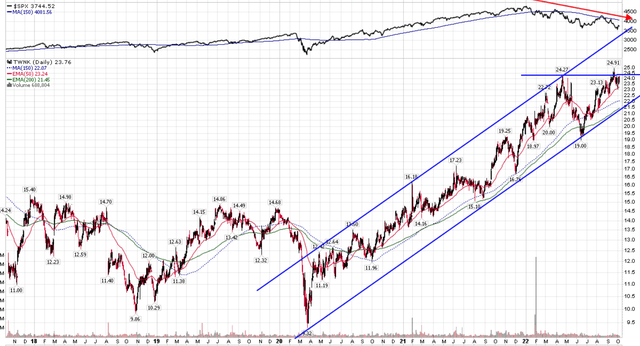

Technicals Present Sturdy Momentum

Technically, TWNK reveals robust relative momentum because the inventory is close to all-time highs whereas the S&P is down over 20% YTD (Determine 11). If TWNK can clear resistance round $24.25, there’s quite a lot of upside within the rising uptrend.

Determine 11 – TWNK inventory reveals robust relative momentum (Creator created with worth charts from stockcharts.com)

Threat

The most important threat to Hostess Manufacturers is a slowdown in client spending impacting gross sales of the corporate’s muffins and snacks. So far, that has not proven up within the knowledge. As proven in Determine 3, TWNK continues to develop volumes and worth/combine. One attainable clarification is that whereas inflation is hovering for all client merchandise, they could be much less noticeable on the typical low worth level of Hostess Manufacturers’ merchandise, or they’ve been hidden through shrinkflation. Moreover, with inflation negatively impacting client procuring habits, maybe shoppers are switching down from buying a dozen Krispy Kreme donuts for $7.99 to purchasing a ten oz bag of Hostess Donettes for $2.50.

One other threat to Hostess Manufacturers is their comparatively excessive ranges of debt. As of June 30, 2022, TWNK has $1.1 billion in time period loans at a 3.6% curiosity value, or 3.3x Web Debt / LTM EBITDA. Excessive ranges of debt could hinder administration’s potential to react to financial situations. Moreover, when the time period mortgage comes up for renewal in 2025, TWNK many not be capable to refinance the mortgage on the identical rock-bottom charges, since rates of interest have elevated considerably previously few months.

Conclusion

Hostess Manufacturers Inc. is a defensive meals staples firm presently firing on all cylinders because it has been capable of develop each volumes and worth/combine regardless of a difficult macro atmosphere. Though the inventory trades at a premium a number of, the a number of could also be sustainable so long as the corporate continues to execute operationally. I’d charge the corporate a purchase based mostly on its growth-at-a-reasonable-price (“GARP”) traits.

:max_bytes(150000):strip_icc()/What-difference-between-standard-Error-means-and-standard-deviation_color-1c203133aca641aca0d03936d9558693.jpg)

/what-difference-between-magnum-cum-laude-and-summa-cum-laude_V2-3ae02babdc714ea9adaeec0f0a6bf1a5.png)

{kind=link}