/gettyimages-591404039-c297fce7598946ba9fcccdf2414277db.jpg)

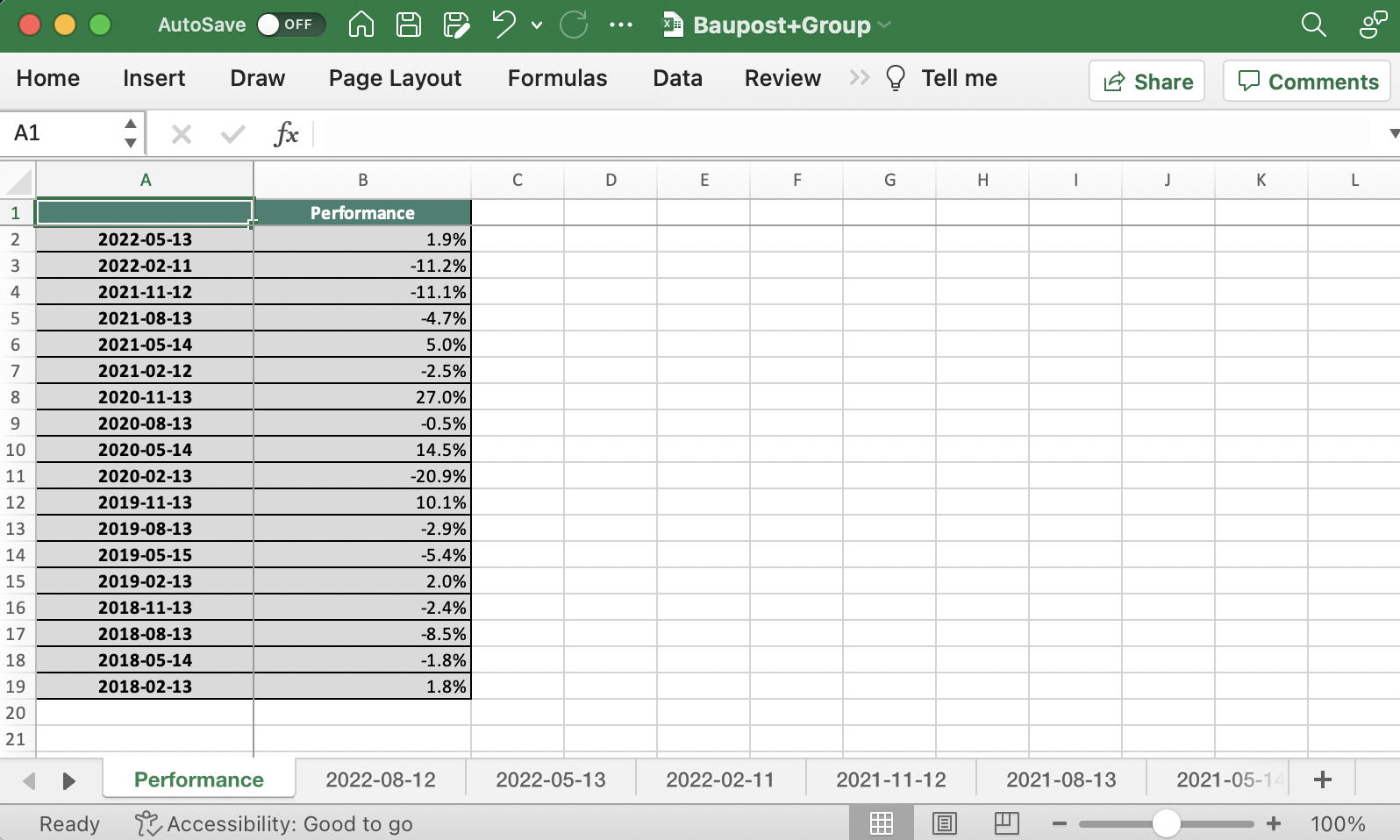

The recognition of cryptocurrencies has grown among the many lots in recent times. It even has some individuals pondering that they’re a very good funding for retirement. In truth, in accordance with the 2022 Investopedia Monetary Literacy Survey, about one-third of buyers beneath the age of 55 plan to depend on cryptocurrency throughout retirement.

This would possibly sound like a dangerous plan, contemplating the volatility of the crypto market, and it’s.

Terra blockchain’s luna, a once-popular stablecoin cryptocurrency, was worn out early in 2022, taking greater than $17 billion in crypto worth with it. The coin’s worth fell from $116 to a fraction of a penny in a matter of days, making it among the many most dramatic crypto crashes on document. That’s, partially, as a result of crypto will not be authorized tender backed by the U.S. authorities, and thus will not be topic to Federal Deposit Insurance coverage Corp. (FDIC) safety.

The U.S. Division of Labor has warned the retirement business to train “excessive care” when investing in crypto, mentioning that plan fiduciaries have a authorized obligation beneath the Worker Retirement Earnings Safety Act (ERISA) to guard individuals’s retirement financial savings. However some persons are extra comfy with danger than others, and the established gamers, like Constancy Investments, are taking discover.

This yr, Constancy Investments, the biggest retirement plan supplier in america, turned the primary so as to add Bitcoin as an funding possibility in its 401(ok) plans. Beneath their plan, buyers will be capable of allocate as much as 20% of their retirement financial savings to bitcoin. However the person fiduciaries might set up their very own worker contribution limits and allocation maximums.

Nevertheless, simply because it’s doable to put money into an asset like crypto for retirement doesn’t essentially make it a good suggestion.

Key Takeaways

Is Cryptocurrency a Good Lengthy-Time period Funding?

The trendy age of cryptocurrencies started with the launch of Bitcoin in 2009. Since then, Bitcoin has seen a imply annual return of 93.8%, which is fairly spectacular over the lengthy haul, however that doesn’t imply there weren’t bumps within the highway. In 2018, the return was -72.6%. And whereas early buyers who’ve held on realized large returns, not all cash have fared so properly. With hundreds of cryptocurrencies to select from, buyers have had blended outcomes, to say the least.

That mentioned, crypto topped the listing of greatest anticipated returns amongst these ages 18 to 55 within the 2022 Investopedia Monetary Literacy Survey. Amongst millennials, 30% anticipate that crypto returns will prime shares, actual property, and mutual funds.

However time will inform if these expectations are based in actuality. For now, it’s too early to know if cryptocurrency can be a very good long-term funding. For many buyers beneath age 55, their retirement is extra years away than any cryptocurrency is years outdated. If you add to that the truth that those self same buyers who anticipate large returns don’t absolutely perceive the place they plan to place their cash, it may be a bit alarming.

In Investopedia’s survey, throughout age teams, greater than 40% of respondents mentioned cryptocurrency is simply too dangerous or too complicated. Amongst millennials, particularly, 44% say that cryptocurrency is simply too complicated or dangerous for his or her cash. In the meantime, 58% of child boomers say that cryptocurrency is simply too complicated. Lower than half of millennials said that they might clarify how cryptocurrencies work, whereas solely 5% of child boomers can clarify cryptocurrencies, and solely 3% perceive non-fungible tokens (NFTs) properly sufficient to share how they work with another person.

So whereas it’s clear that cryptocurrency could be a novel and typically stylish new asset class, it’s additionally extraordinarily dangerous and risky. It’s possible you’ll need to assume twice, and seek the advice of a monetary planner, earlier than leaning on crypto to your retirement planning.

Cryptocurrency markets can comply with patterns just like these of inventory markets, with up and down cycles. However a down market, or a crypto winter, may have lasting impacts.

What to Look For When Selecting Retirement Investments

As you’re constructing your retirement portfolio, it’s important to think about a number of important elements, corresponding to:

Anticipated development fee: An necessary funding elementary is the anticipated development fee. Inventory market and bond buyers depend on numerous valuation fashions to foretell development. That’s trickier with cryptocurrencies.

Threat and volatility: Each inventory and bond markets have a long time of historic knowledge and danger measurement frameworks. Not solely are cryptocurrencies riskier and extra risky than shares or bonds, however measuring their danger can be extra complicated. The variety of fashions obtainable to measure cryptocurrency danger is proscribed.

Money move: Many investments provide predictable dividends, bond coupon funds, and different types of money move. Right here, a number of cryptocurrencies present an edge over extra conventional investments because of staking and yield farming. It’s doable, nonetheless, that these newer programs will now not operate the identical method 10 to twenty years down the highway when an individual retires.

After all, simply because one thing is new and untested doesn’t essentially imply it’s a nasty funding. The ultimate choice on the place to place cash is as much as the investor, so they need to weigh the professionals and cons each time earlier than making a call.

How one can Construct a Core Retirement Technique

What’s the applicable funding quantity for an investor? It is dependent upon numerous elements. First, calculate your monetary wants for retirement. Then, decide the allocation of investments and contributions wanted to get there.

Conventional funding methods targeted on a mix of shares and bonds to succeed in this aim for the everyday investor, typically relying closely on tax-advantaged 401(ok) plans and particular person retirement accounts (IRAs). Along with crypto-specific and completely self-directed conventional and Roth IRAs, some conventional brokerage corporations are starting so as to add cryptocurrency to conventional retirement accounts. So in the event you’re set that that is your path ahead, seek the advice of a monetary advisor earlier than placing your cash into such a dangerous asset.

Of all investments in anyone’s life, retirement accounts are arguably crucial. And in the event you go large on crypto—or in the event you solely make investments solely in cryptocurrency to your retirement, and that asset class goes bust, as we’ve got seen in latest crypto winters—you could be pressured to rethink your present or future plans with little discover.

The place Crypto Suits into An Funding Plan

Because of the danger, volatility, and problem predicting the way forward for cryptocurrency, many buyers ought to keep away from together with crypto of their retirement investments altogether. In case you resolve to incorporate cryptocurrencies, preserving them as a smaller portion of your total portfolio could also be smart.

Until you’re a agency believer in cryptocurrency who desires to benefit from the tax financial savings of a cryptocurrency IRA, you could be higher off preserving cryptocurrency as a comparatively small portion of your total portfolio and out of your retirement.

Many funding specialists counsel preserving the majority of your retirement property within the inventory market, ideally in low-fee, numerous exchange-traded funds (ETFs). Excessive-risk different investments are nonetheless honest recreation however reserved for a portion of your investments that aren’t important to your livelihood sooner or later.

Is it doable to plan retirement with Bitcoin?

Cryptocurrencies are in style nowadays, however placing bitcoins right into a 401(ok) is a brand new thought. Constancy Investments lately introduced that it will start providing bitcoin funding choices in its 401(ok) plans by the center of 2022.

The Backside Line

When constructing your cryptocurrency funding technique, take into account this situation. In case you invested $5,000 in cryptocurrency and it went up by 10×, you’d have $50,000. That’s an important return. But when it went to zero, wouldn’t it be sufficient to damage your retirement plans? Most likely not.

Whereas the $5,000 instance works for some people or households, your funding portfolio, danger tolerance, and monetary targets are distinctive. By understanding your investments and the way each asset that you simply personal works, you’ll be able to resolve on the best allocation to your retirement portfolio and different investments. Cryptocurrency might slot in one or each of these funding methods. However in the event you’re planning on counting on property for retirement, make investments with care.

/gettyimages-591404039-c297fce7598946ba9fcccdf2414277db.jpg&description=Ought%20to%20Buyers%20Put%20Crypto%20in%20Their%20Retirement%20Accounts%3F){kind=link}