JulPo/E+ through Getty Pictures

Funding Thesis

Alpine Earnings Property Belief (NYSE:PINE) is an actual property funding belief specializing in web leasing properties to industry-leading tenants in Metropolitan Statistical Areas. The corporate has lately reported robust third-quarter outcomes primarily pushed by continued acquisitions and engaging provide and demand dynamics which might maintain for an extended interval, additional accelerating its progress by diversifying its portfolio in high-growth markets. The corporate additionally pays a excessive quarterly dividend, making it a sexy funding alternative for risk-averse and retired buyers.

About PINE

Alpine Earnings Property Belief primarily offers in proudly owning and working a portfolio that consists of economic web lease properties throughout the USA. The corporate primarily leases its properties to industry-leading tenants working primarily in industries proof against the impression of e-commerce. The tenants are from numerous sectors, comparable to pharmacy, sports activities items, grocery, house furnishings, basic merchandising, shopper electronics, well being and health, and leisure. Its portfolio includes 146 web leased properties in markets of 35 states. These properties are situated in favorable financial and demographic progress markets and close to main Metropolitan Statistical Areas (MSA). These engaging places characterize the corporate’s portfolio of three.7 million gross rentable sq. ft. 63% of the annual base hire was derived from properties in MSAs for the yr 2021. The web lease property market has skilled regular progress over time, and investor demand for web leased properties has continued to achieve vital momentum, which has considerably contributed to the corporate’s progress. It’s a extra versatile enterprise, in contrast to gross leasing, as web leases don’t embrace monetary duty for bills comparable to insurance coverage, property taxes, upkeep, and capital expenditures. The corporate presently targets tenants with engaging credit score traits, correct hire protection ranges, and wholesome working historical past.

Financials

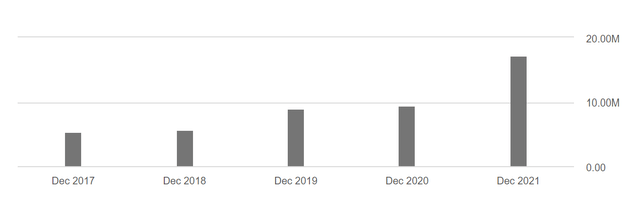

Income Pattern (Searching for Alpha)

As we are able to see within the above chart, the corporate has managed to attain strong progress within the final 5 years. The income has grown from $8.45 million in FY2017 to $30.13 million in FY2021 leading to a considerable 5-year CAGR of 28.95%. Additionally, the corporate has skilled robust FFO progress up to now 5 years. The FFO has grown from $5.3 million in FY2017 to $17.2 million in FY2021 leading to a 5-year CAGR of 26.55%

FFO Pattern (Searching for Alpha)

Not too long ago, Alpine has reported robust Q3 FY2022 outcomes. The corporate has reported income of $11.52 million, a 41% soar in comparison with Q3 2021 income of $8.17 million. The income progress was supported by lease earnings from the brand new acquisition of 9 high-quality retail web lease properties, representing a complete acquisition quantity of $36.7 million and reflecting a weighted common going-in money cap charge of seven.1%. These acquired properties had been leased to tenants of 4 rising sectors, which embrace greenback shops, sporting items, house enhancements, and residential furnishings. The corporate has shocked the market with excellent web earnings progress of 957.8% YoY, which is 9.60% greater than the market consensus. Web earnings of the third quarter is $11.17 million in comparison with $1.05 million within the earlier yr’s third quarter. The corporate reported AFFO per diluted share of $0.42, up 13.5% from $0.37 in Q3 2021. The outcomes beat the market’s expectations of AFFO per diluted share and offered a constructive outlook for This fall 2022. The corporate ended its third quarter with $2.24 million in money & money equivalents and web debt of $271.9 million. At a weighted common exit money cap charge of 5.5%, six web lease properties had been offered for $50.5 million, producing $11.6 million in features. There was a rise to $350 million within the credit score facility, which consists of a $250 million unsecured revolving credit score facility and $100 million in current unsecured time period loans.

The robust outcomes of the corporate are a mirrored image of engaging provide and demand dynamics and likewise its portfolio growth in high-growth markets. I imagine this progress of the corporate will be sustainable because the Southeast and Southwest portfolio can proceed to learn the corporate from inhabitants shifts. After analyzing all the expansion elements, I believe the corporate has an upside potential, and I’m estimating a strong quarter within the coming years. Even the administration may be very optimistic about it. That is why the corporate has raised its earlier steerage. The corporate is estimating AFFO per diluted share to be within the vary of $1.53-$1.63. I believe the corporate’s expectations are conservative. Trying on the present progress elements, I believe AFFO per share for FY2022 will be between $1.80-$1.95. I estimate the income for FY22 will be within the vary of $44.9 million, up 49.1% from the earlier yr, which will be primarily fueled by the corporate’s constantly rising web leasing operations within the Metropolitan Statistical Areas. This improve in income can additional assist the corporate develop its revenue margins and push the inventory upside.

Excessive Dividend Yield

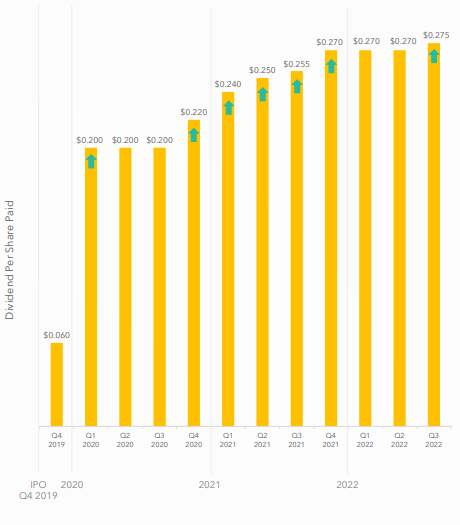

We will see vital progress within the firm’s dividend payout over time, which displays its well-positioning within the aggressive market. For the reason that starting of 2020, we are able to see a wholesome upside of 37.5% within the quarterly money dividends. Within the present yr, the corporate has distributed a dividend of $0.2700 per quarter within the first two quarters and lately declared a dividend of $0.2750 for the third quarter. The corporate has recorded robust third-quarter outcomes and is contemplating different progress elements, comparable to advantages from inhabitants shifts and the brand new acquisition of 9 high-quality retail web lease properties, which I believe can gasoline the corporate’s efficiency. That’s the reason I imagine this dividend of $0.2750 will be fixed for the final quarter, which makes a full-year dividend of $1.09. This dividend represents a dividend yield of 5.84%, which makes it a sexy funding alternative for risk-averse and retired buyers.

Dividend Cost Pattern (Investor Shows: Slide No: 16)

What’s the Major Danger Confronted by PINE?

Dependency on Demand of Retail House

92% of the straight-line annual hire of the corporate’s preliminary portfolio was leased to tenants operating retail institutions. PINE plans to purchase extra properties sooner or later that are actually leased to a single tenant that runs a retail operation there. Because of this, the corporate could also be extra negatively impacted by declines out there for renting retail area than it might be if it had much less of an funding in retail buildings. The leasing marketplace for retail area has traditionally been negatively impacted by weak nationwide, regional, and native economies, the poor monetary well being of some main retailers, retail {industry} consolidation, an extra of retail area in some places, and rising e-commerce strain. If unfavorable circumstances develop or persist, they’re prone to have a unfavorable impression on market leases for retail area and will have a significantly unfavorable impression on the enterprise.

Valuation

The corporate has recorded robust third-quarter outcomes. I imagine it might preserve this progress within the coming years attributable to robust provide and demand dynamics, diversification in high-growth markets, and focusing on industry-leading tenants. After contemplating all of the above elements, I’m estimating an FFO per share of $1.95 for FY2023, giving the ahead P/FFO ratio of 9.56x. After evaluating the ahead P/FFO ratio of 9.56x with the sector median of 13.54x, I believe the corporate is undervalued. After contemplating the robust demand for retail area, I believe the corporate would possibly commerce on the sector median. Therefore, I estimate the corporate would possibly commerce at a P/FFO ratio of 13.54x, giving the goal worth of $26.40, which is a 42% upside in comparison with the present share worth of $18.65.

Conclusion

Alpine Earnings Property is an actual property funding belief which offers within the web leasing of properties, primarily specializing in Metropolitan Statistical Areas. The corporate has lately reported robust third-quarter outcomes, which had been pushed by leasing incomes from vigorous acquisitions carried out by the corporate within the third quarter. I imagine this progress will be sustainable as the corporate is specializing in high-growth markets, well-operating sectors, diversification in Metropolitan Statistical Areas, and emphasizing robust provide and demand dynamics. After evaluating the ahead P/FFO ratio of 9.56x with the sector median of 13.54x, I believe the corporate is undervalued. After contemplating all of the above elements, I assign a purchase ranking for PINE.

:max_bytes(150000):strip_icc()/What-difference-between-standard-Error-means-and-standard-deviation_color-1c203133aca641aca0d03936d9558693.jpg)

/what-difference-between-magnum-cum-laude-and-summa-cum-laude_V2-3ae02babdc714ea9adaeec0f0a6bf1a5.png)

/HabitsThatWillHelpYouPayOffDebtMay202021-51f5539c69cf4a7ba82f9f7059c10f5c.jpg)

{kind=link}