JHVEPhoto

Large tech shares have fallen out of favor with buyers over the previous 12 months. Nevertheless, the long-term prospects of those shares look vivid as know-how continues to form the lives of tens of millions of individuals each day. Whereas I are likely to favor investing in dividend payers, I do see the worth in a “barbell” strategy, with portfolio weighting on regular payers corresponding to Realty Earnings Corp. (O) and Verizon (VZ) balanced out by excessive development tech shares.

This brings me to tech trade juggernaut (NASDAQ:GOOG) (NASDAQ:GOOGL), which as seen under, is buying and selling effectively off its 52-week excessive of $152. On this article, I spotlight why pessimism could also be overblown, and why now could also be an opportune time to purchase the inventory, so let’s get began.

GOOG Inventory (In search of Alpha)

Robust Fundamentals

Google could now not by the ultra-growth inventory that it as soon as was, however that is okay. Over the previous 2 many years, the corporate has constructed a formidable product portfolio which enjoys unbelievable loyalty amongst its customers. Its iconic search engine is the rationale why many individuals belief Google to energy their most essential laptop wants. And with different merchandise corresponding to Gmail, Android, YouTube, and Google Maps, the corporate maintains all kinds of providers which can be broadly used around the globe.

Furthermore, its cloud division continues to display double-digit income development, and presently instructions 8% share of the overall cloud market, sitting behind 21% for Microsoft’s (MSFT) Azure and 33% for Amazon’s (AMZN) AWS.

In the meantime, Google’s whole income grew by 6% YoY in its third quarter. Whereas this will likely not appear too spectacular on the floor, it’s price noting that Google has a really sturdy worldwide presence that is topic to foreign money dangers, particularly contemplating the sturdy rise within the greenback this 12 months. Excluding foreign money results, Google’s income development was a extra spectacular 11% YoY.

This was pushed by vivid spots in search income, which grew by 4% YoY and by cloud income, which grew by 38% YoY, offset by YouTube and community promoting income declining 1.9% and 1.6%, respectively.

YouTube Shorts and DeepMind AI

Along with its product suite, Google has additionally made some spectacular strikes on the planet of Synthetic Intelligence. Its DeepMind division has achieved a number of unbelievable milestones lately and is now one of many main AI firms on the planet. This, coupled with advances in different areas corresponding to cloud computing and autonomous automobiles, places Google at a singular benefit that few different firms can match.

Whereas YouTube’s income decline was disappointing, I see long-term potential, contemplating that YouTube Shorts has now reached 1.5 million month-to-month energetic customers, serving to to allay considerations that TikTok goes to pose a major threat to the enterprise. Moreover, Google is leveraging its deep bench of AI experience to monetize YouTube Shorts and Google Lens, as famous by administration in the course of the latest convention name:

At our Search On occasion, we shared how we’re utilizing AI advances to ship a extra pure and intuitive search expertise. These developments will quickly assist to floor belongings you may discover useful earlier than you even end typing. We’re additionally making visible search extra pure than ever earlier than.

Individuals now use Google Lens to reply greater than 8 billion questions each month utilizing only a picture or a picture. Now, we’re supercharging our visible search capabilities to assist folks discover what they’re on the lookout for at companies close by.

Steadiness Sheet and Valuation

In the meantime, Google maintains an AA+ rated stability sheet, placing it on par with that of the U.S. Authorities. That is supported by a staggering $116 billion of money and short-term investments on the stability sheet, in opposition to simply $12.9 billion of long-term debt.

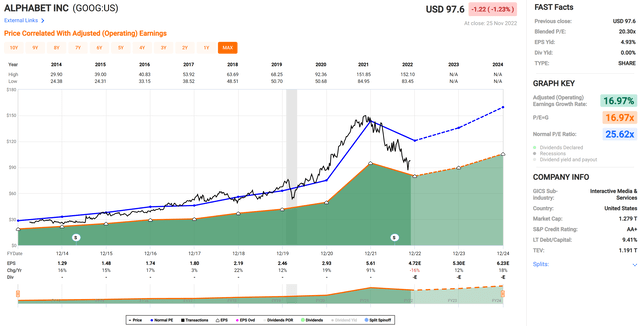

Google additionally trades cheaply relative to historic valuations. On the present worth of $97.60, Google carries a ahead PE of simply 2046, sitting effectively under its regular PE of 25.6, as proven under. Analysts additionally estimate 9 – 12% EPS development yearly over the subsequent 2 years. Morningstar has a $160 honest worth estimate and analysts have a consensus Robust Purchase ranking with a mean worth goal of $126.

Given the fortress stability sheet, wide-moat enterprise mannequin, and ahead EPS development estimates, I’d anticipate GOOG to commerce with a ahead PE within the 25x vary, implying a worth goal of $120. As such, I view Google as being a robust by on the present worth, presenting a 20%+ low cost from my comparatively extra conservative worth estimate.

GOOG Valuation (FAST Graphs)

Investor Takeaway

Google’s broad know-how choices together with its quick rising cloud division, coupled with its fortress stability sheet, extensive attain and comparatively low-cost valuation, makes it a horny funding on the present time. Whereas its YouTube promoting enterprise noticed a slight decline in income, I consider the latest launch of YouTube Shorts holds quite a lot of promise and Google is leveraging its deep bench of AI experience throughout its platforms. As such, development and worth buyers could also be well-served to take a tough take a look at Google at present ranges.

{kind=link}