4kodiak

Thesis

Intel (NASDAQ:INTC) has been tormented by each lackluster outcomes and share costs recently. The enterprise has been affected by each its personal points and a macroeconomic slowdown. The technological lag of its merchandise, the heavy funding concerned in its IFS initiatives, the supply-chain challenges, and the inflationary pressures all plagued outcomes and eroded margins. It is usually price noting that company-specific execution points harm profitability as nicely.

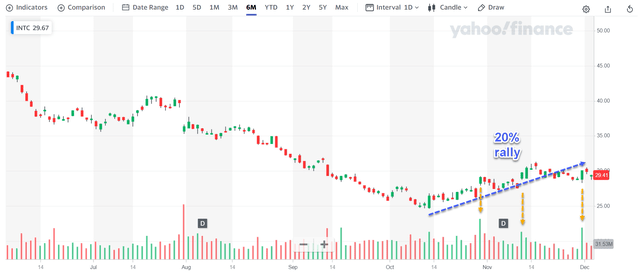

In opposition to this backdrop, the thesis of this text is to indicate that the inventory just lately confirmed robust indicators, each technical and elementary, of getting bottomed in Q3. As you’ll be able to see from the next chart beneath, its inventory costs staged a 20% rally since touching a backside of $24.5 in mid-October. Extra importantly, on a number of buying and selling days (highlighted by the orange arrows), the robust rallies have been on massive volumes too, a classical technical rebounding signal.

Supply: creator primarily based on Yahoo Finance knowledge.

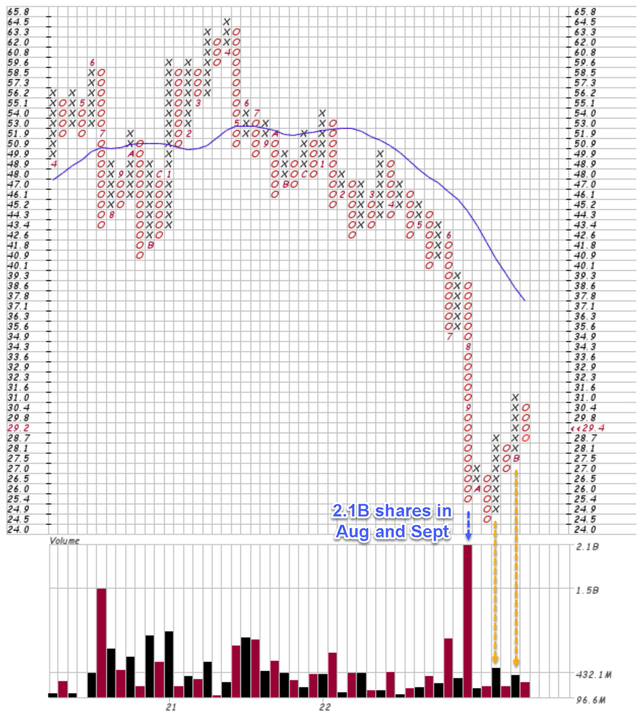

For traders with a longer-term timeframe, the so-called Level & Determine Chart (“PFC”) is extra useful. In case you are , this tutorial supplies the fundamentals for studying PFC. The essence of the PFC is to filter out a lot of the every day noises so the long-term pattern is displayed extra clearly. Now again to INTC, a number of highlights from this chart:

The PFC beneath shows ~3 years’ price of INTC’s value and quantity data (2019~2022). The crimson Os present value declines and the black Xs present value advance. Therefore, you’ll be able to clearly view the course and buying and selling quantity over an extended timeframe and procure an total sense of the dominating market forces. To wit, throughout August and September, INTC suffered the worst selloff in years. A complete of two.1 billion shares modified fingers throughout these two months (about 50% of excellent shares) on a value decline from $39.3 to $26.0 (i.e., a decline of greater than 1/3), and the quantity quieted down considerably afterward (a technical signal of exhaustion). Then the buying and selling in October and November is extra dominated by volumes on rising inventory costs as highlighted by the orange arrows, a classical technical signal for rebounding.

The PFC is a really helpful device for long-term traders – a bridge between technical evaluation and elementary evaluation in my thoughts. And that’s what we’ll discover subsequent – the implications of those buying and selling patterns when it comes to its enterprise fundamentals.

Supply: creator primarily based on stockcharts.com knowledge.

Valuation Implications

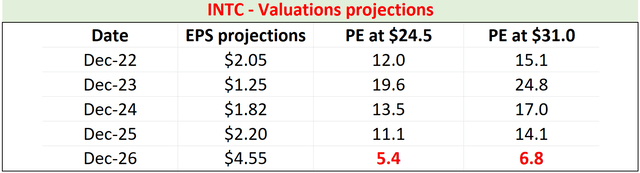

As simply talked about above, the buying and selling in October and November is extra dominated by volumes on rising inventory costs in a variety between about $24.5 and $31.0. The desk beneath exhibits the valuation for INTC inside this vary. The EPS projections are taken from the SA consensus estimates. As seen, the consensus estimates mission its EPS to contract to $1.25 subsequent yr and recuperate to $4.55 in 2026. All advised, the implied PEs on this value vary are within the mid to low teenagers aside from 2023. And I view such valuations as very cheap for the expansion potential and high quality of the inventory. Then in 2026, the time when its IFS is predicted to be totally on-line, the implied PE would drop to the only digits, between a variety of 5.4x to six.8x, illustrating the outsized upside return potential.

And subsequent, I’ll argue that these EPS projections are too conservative due to the extraordinarily pessimistic margin assumptions embed within the consensus estimates.

Supply: creator primarily based on Looking for Alpha knowledge.

Progress and margin projections

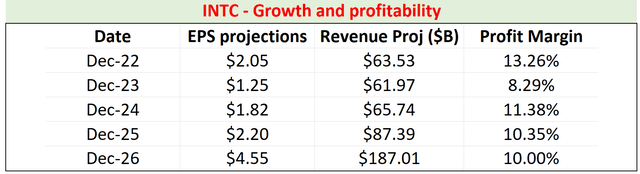

The chart beneath exhibits the consensus estimates of its revenues too. As seen, the consensus estimates mission its revenues to say no to $61.9B in 2023, then regularly recuperate, and at last be adopted by a sudden enlargement in 2026 once more due to the IFS. Assuming its share counts stay on the present degree of 4.11B, I computed its complete revenue primarily based on the EPS projections so I can get hold of the implied margins, that are proven within the 4th column. As you’ll be able to see, the consensus estimates implied a revenue margin hovering round a mean of 10% within the subsequent few years.

Supply: creator primarily based on Looking for Alpha knowledge.

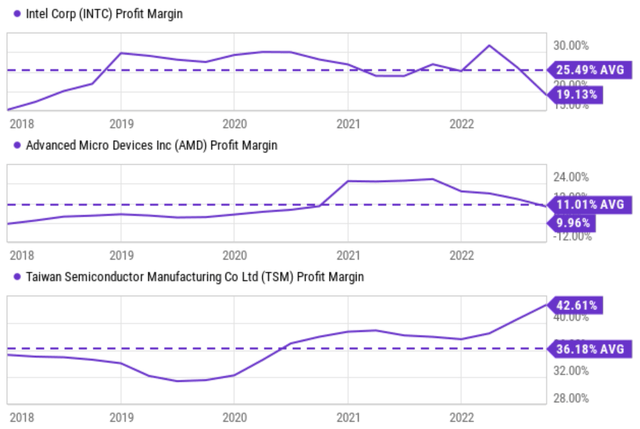

Such an implied margin is just too pessimistic in my thoughts primarily based on its historic report and likewise its friends’ revenue margins (“PM”). The chart beneath exhibits its PM up to now 5 years along with these from Superior Micro Units (AMD) and Taiwan Semiconductor (TSM). As seen within the prime panel, INTC’s PM has been on common 25.5%. Its present PM of 19.1% is admittedly far beneath its historic common as a result of varied headwinds we talked about above. Nevertheless, it’s virtually double the ten% degree consensus estimates implied. The mid panel exhibits that AMD’s common PM is about 10%, and TSM’s common PM is about 36%. Contemplating that A) AMD is a pure chip designer, B) TSM is a pure chip producer, and C) Intel goes to be a hybrid, I believe it is logical to anticipate Intel’s PM to be some kind of weighted common of the PM of AMD and TSM, which might put it above the implied 10% additionally.

Supply: Looking for Alpha knowledge.

Dangers and remaining ideas

To recap, INTC has been tormented by a large number of points, starting from macroeconomic elements to company-specific execution points. In consequence, virtually of all its segments (the Consumer Computing Group, Knowledge Middle and AI Group, and Intel Foundry Providers) suffered revenue declines on a YoY foundation. Trying ahead, a few of these points could persist longer, such because the technological catch-up of its merchandise, the heavy funding concerned in its IFS initiatives, the supply-chain challenges, and likewise inflationary pressures.

Nevertheless, I see robust indicators, each technical and elementary indicators, that the inventory has bottomed in Q3 at a value close to $25. Going ahead (baring a full-scale financial recession), I see the supply-chain challenges, the inflationary pressures, and likewise international PC slowdown have already handed their worst. When it comes to its IFS CAPEX necessities, I anticipate a assist of round $4B from EU and Brookfield Asset Administration contribution in CY22 alone. Then I additionally anticipate substantial subsidies from the US CHIPS Act funding in CY23, additional easing its CAPEX requirement.

Contemplating these developments, its valuation is just too compressed to disregard. Its PE is barely within the single digits (5.4x to six.8x) as soon as its IFS turns into on-line even below extraordinarily pessimistic margin assumptions implied by the consensus estimates. These implied revenue margins are on common solely about 10%, whereas I believe its revenue margin needs to be no less than 20% on common contemplating its historic report and friends’ profitability.

/what-difference-between-magnum-cum-laude-and-summa-cum-laude_V2-3ae02babdc714ea9adaeec0f0a6bf1a5.png)

:max_bytes(150000):strip_icc()/What-difference-between-standard-Error-means-and-standard-deviation_color-1c203133aca641aca0d03936d9558693.jpg)

{kind=link}