Printed on December thirty first, 2022 by Nikolaos Sismanis

Dividend Aristocrats comprise an elite group of 65 S&P 500 shares with 25+ years of consecutive dividend will increase. These shares are celebrated amongst dividend development buyers, as they’re thought of dependable automobiles for rising one’s earnings in a extra predictable method.

Nevertheless, it’s essential to notice that not all Dividend Aristocrats are created equal. Whereas most shares within the group have a tendency to extend their payouts meaningfully, others accomplish that solely marginally as a approach to retain their Dividend Aristocrat standing. In some circumstances, this can be a means for a Dividend Aristocrat to protect liquidity or enhance their monetary place earlier than extra noteworthy dividend hikes resume.

That mentioned, it’s price contemplating whether or not decelerating dividend will increase may very well be a signaling monetary pressure and whether or not it raises the chance of a dividend reduce sooner or later. As such, these Dividend Aristocrats needs to be evaluated twice earlier than making any funding selections.

We have now compiled an inventory of all 65 Dividend Aristocrats, together with related monetary metrics like dividend yield and P/E ratios. You possibly can obtain the complete listing of Dividend Aristocrats by clicking on the hyperlink under:

Desk of Contents

Examples of Dividend Cuts Following a Declining Dividend Development Tempo

Whereas it’s not a certain signal of monetary pressure, a Dividend Aristocrat slowing its tempo of dividend will increase might be an indication that the corporate is going through monetary challenges. This might probably result in a reduce in dividends. Listed here are some such examples which have beforehand occurred:

Pitney Bowes Inc. (PBI)

Pitney Bowes had grown its dividend yearly between 1983 and 2013, boasting 30 years of consecutive annual dividend will increase. In 2013, the corporate was pressured to chop its dividend after monetary misery, ending its multi-decade streak. Right here’s how Pitney Bowes’ dividend development tempo seemed previous to the reduce:

1993 – 1998 DPS CAGR: 14.9%

1998 – 2003 DPS CAGR: 5.9%

2007 – 2012 DPS CAGR: 2.6%

AT&T Inc. (T)

Earnings-oriented buyers’ darling AT&T was pressured to chop its dividend by the tip of 2021 after 37 years of consecutive annual dividend will increase. With its indebtedness reaching unsustainable ranges, a dividend reduce was the one means for the corporate to start out deleveraging meaningfully and pursue recent development initiatives. Right here’s how AT&T’s dividend development tempo seemed previous to the reduce:

2003 – 2008 DPS CAGR: 6.8%

2008 – 2013 DPS CAGR: 2.4%

2016 – 2021 DPS CAGR: 1.5%

Mercury Basic Company (MCY)

Small-cap insurer Mercury Basic finally needed to finish its 35-year dividend development streak in 2022 after years of over-distributing its earnings. The corporate’s payout ratio would usually exceed 100%. Right here’s how Mercury Basic’s dividend development tempo seemed previous to the reduce:

2002 – 2007 DPS CAGR: 11.6%

2007 – 2012 DPS CAGR: 3.3%

2016 – 2021 DPS CAGR: 0.4%

The 8 Dividend Aristocrats With The Smallest Dividend Will increase

In addition to AT&T’s unlucky reduce, Dividend Aristocrats continued to develop their dividends at slightly passable charges. The typical dividend hike in 2022 by all 64 Dividend Aristocrats was 6.5%. Notably, 11 Dividend Aristocrats delivered double-digit hikes, whereas 28 Aristocrats grew their dividends by lower than 5% for the 12 months.

That mentioned, eight corporations, particularly, grew their dividends by a fee equal to or under 1%. May their decelerating tempo of dividend will increase sign a possible reduce transferring ahead?

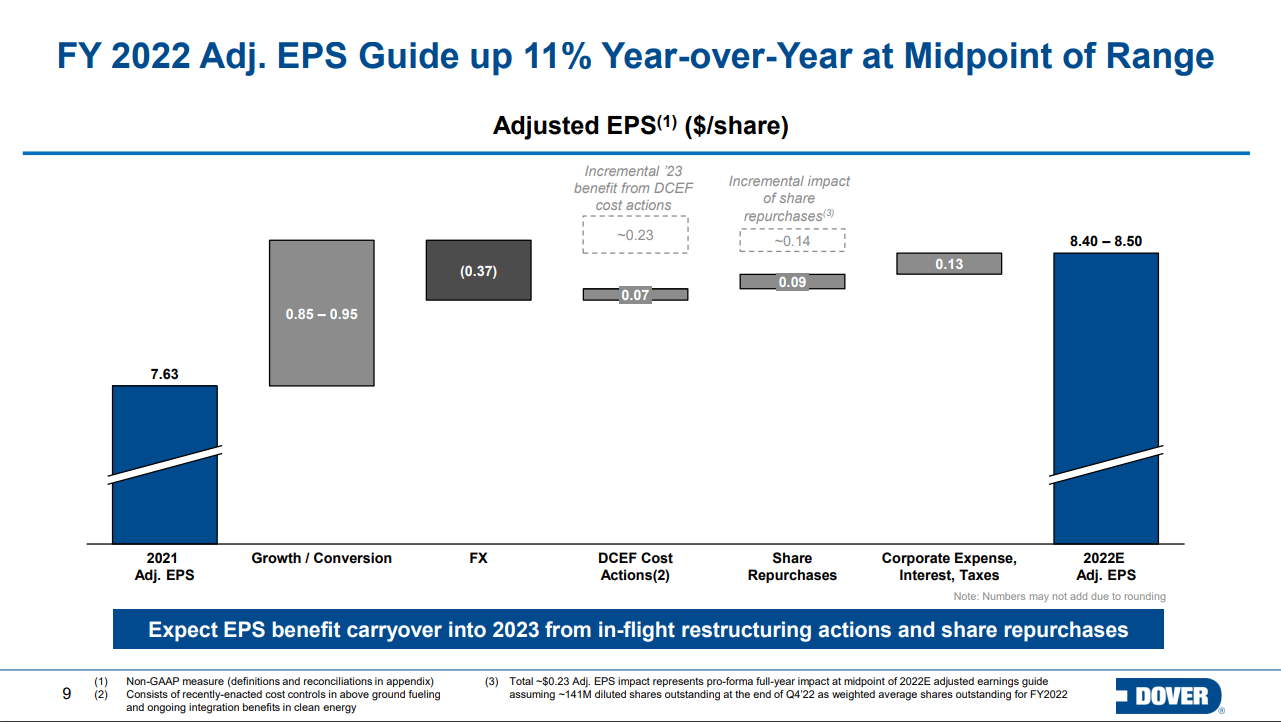

#8: Dover Company (DOV)

Years of dividend development: 67

Dividend yield: 1.5%

2005 – 2011 DPS CAGR: 10.7%

2011 – 2016 DPS CAGR: 7.8%

2016 – 2021 DPS CAGR: 3.0%

Newest DPS improve: 1.0%

Dover Company is a diversified world industrial producer with annual revenues of almost $9 billion. Dover’s 5 reporting segments embrace Engineered Techniques, Clear Vitality & Fueling, Pumps & Course of Options, Imaging & Identification, and Local weather & Sustainability Applied sciences.

The corporate is a Dividend King with greater than six many years of dividend will increase. Actually, with 2022’s dividend improve marking 67 consecutive years of dividend development, Dover boasts the second-longest dividend development streak amongst U.S. corporations.

Dover’s earnings-per-share have compounded at 6% yearly during the last decade. Development, in truth, accelerated in the latest years, with earnings-per-share development rising at an annual fee of greater than 14% over the previous 5 years. Dover did endure some setbacks through the worst of the COVID-19 pandemic, however the firm rapidly rebounded.

Supply: Investor Presentation

Is Dover Corp Prone to Lower its Dividend?

Regardless of Dover’s dividend development fee decelerating considerably over the previous few years, we don’t imagine the corporate is headed towards a dividend reduce. Whereas Dover is a cyclical inventory, with its revenues topic to wild fluctuations throughout unfavorable market durations, the corporate has managed to maintain its earnings at stable ranges and even develop then notably over time. Final 12 months, the corporate’s web earnings hit a brand new all-time whereas following earnings development surpassing dividend development over the 12 months, the inventory’s payout ratio stands at a really wholesome 24%

Click on right here to obtain our most up-to-date Certain Evaluation report on Dover Company (preview of web page 1 of three proven under):

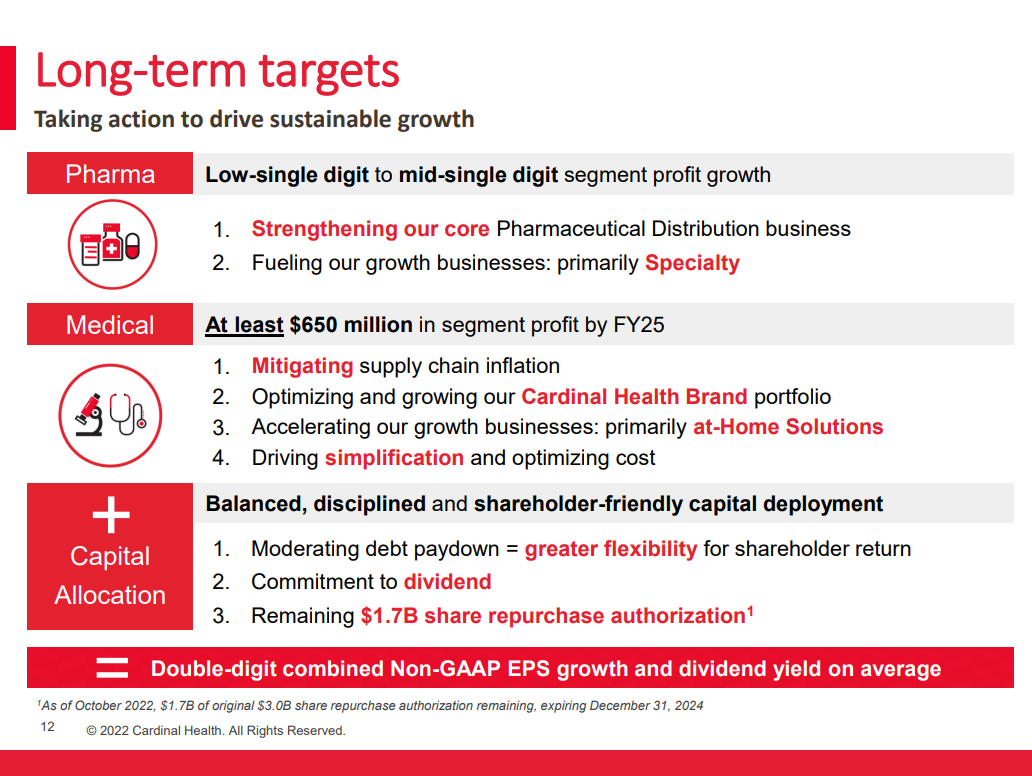

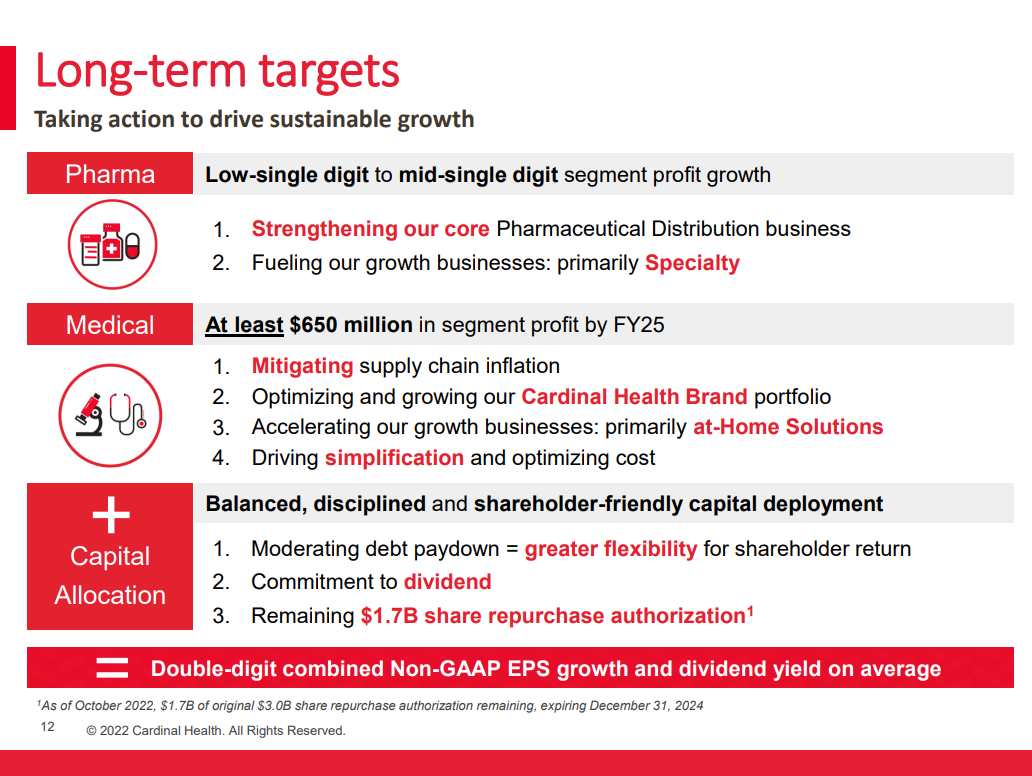

#7 Cardinal Well being, Inc. (CAH)

Years of dividend development: 35

Dividend yield: 2.5%

2005 – 2011 DPS CAGR: 24.3%

2011 – 2016 DPS CAGR: 15.0%

2016 – 2021 DPS CAGR: 3.9%

Newest DPS improve: 1.0%

Dublin, Ohio-based Cardinal Well being is without doubt one of the “Massive 3” drug distribution corporations together with McKesson (MKC) and AmerisourceBergen (ABC). Cardinal Well being serves over 24,000 United States pharmacies and greater than 85% of the nation’s hospitals. The corporate has operations in additional than 30 international locations with roughly 46,000 workers.

With 35 years of dividend will increase, the $20.4 billion market cap firm is a member of the Dividend Aristocrats Index.

Between 2011 and 2021, Cardinal Well being grew its earnings-per-share by a median compound fee of seven.6% per 12 months, whereas the dividend grew at greater than 9% yearly. Transferring ahead, we don’t anticipate this type of development, particularly contemplating the slowdown in earnings enchancment in the previous few years.

Supply: Investor Presentation

Is Cardinal Well being Prone to Lower its Dividend?

Certainly, Cardinal Well being’s dividend development tempo has decelerated dramatically over the previous decade, whereas its most up-to-date 1% dividend improve was definitely underwhelming. Nonetheless, we don’t imagine the corporate plans to chop its dividend anytime quickly.

It is because the corporate’s earnings are more likely to stay sturdy as medicine are inclined to generate constant gross sales as their important pharmaceutical merchandise. Additional, the corporate’s payout ratio stands at a cushty 38%, whereas Cardinal’s total monetary well being has been enhancing.

Particularly, Cardinal’s long-term debt has declined from $9.0 billion in 2017 to $4.7 billion as of its most up-to-date Q3 2022 report. Lastly, the corporate is more likely to droop its inventory repurchases earlier than touching the dividend, and inventory repurchases have remained robust all year long.

Click on right here to obtain our most up-to-date Certain Evaluation report on Cardinal Well being, Inc.(preview of web page 1 of three proven under):

#6 Emerson Electrical Co. (EMR)

Years of dividend development: 66

Dividend yield: 2.2%

2005 – 2011 DPS CAGR: 9.2%

2011 – 2016 DPS CAGR: 6.6%

2016 – 2021 DPS CAGR: 1.2%

Newest DPS improve: 1.0%

Emerson Electrical was based in Missouri in 1890. Since that point, it has developed by means of natural development, in addition to strategic acquisitions and divestitures, from a regional producer of electrical motors and followers right into a $56 billion diversified world chief in know-how and engineering.

Its world buyer base and various product and repair choices afford it about $20 billion in annual income. The corporate’s very spectacular 66-year dividend improve streak lands it on the celebrated Dividend Kings listing.

Supply: Investor Presentation

Emerson is present process a big shift in its technique, whereby it’s promoting off legacy items and focusing extra on automation and recurring income. We imagine that low single-digit development in income and a tailwind from the buybacks would be the key drivers of earnings-per-share development within the coming years. The corporate has decreased its share depend by about 37% since 1987.

Nonetheless, we observe there may be more likely to be vital earnings weak spot whereas the transformation performs out, together with a gradual begin to fiscal 2023.

Is Emerson Electrical Prone to Lower its Dividend?

Regardless of Emerson Electrical having considerably slowed down the speed at which it grows its dividend, we don’t imagine this to be an indication of a near-term reduce. The dividend is well-covered.

Actually, with earnings-per-share rising at a CAGR of seven.3% over the previous decade, Emerson’s payout ratio has relaxed considerably currently. It stood at 77% in 2016 however has now fallen to 51%. The deceleration in dividend hikes is more than likely a part of Emerson’s transformation plan.

Click on right here to obtain our most up-to-date Certain Evaluation report on Emerson Electrical Co. (preview of web page 1 of three proven under):

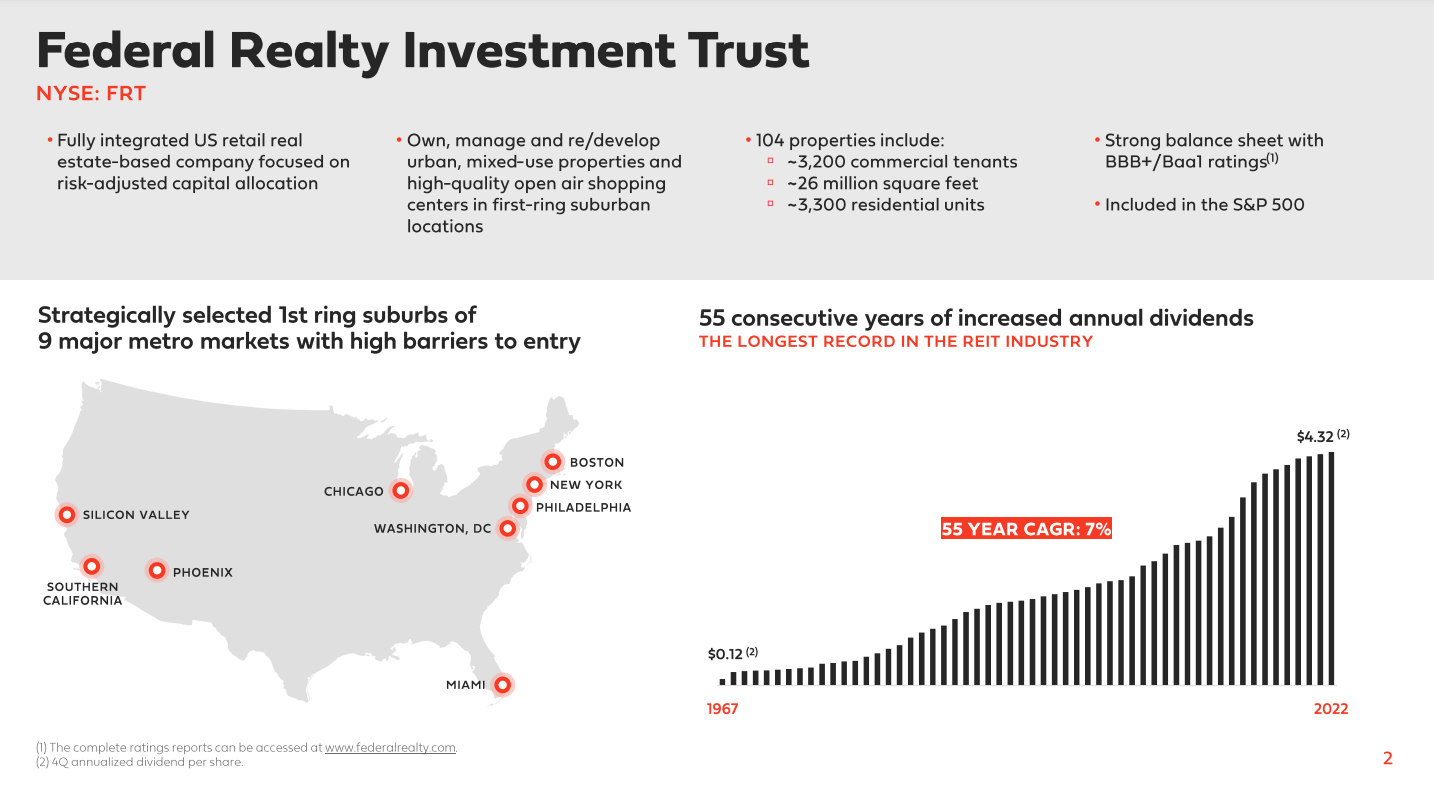

#5 Federal Realty Funding Belief (FRT)

Years of dividend development: 55

Dividend yield: 4.2%

2005 – 2011 DPS CAGR: 3.8%

2011 – 2016 DPS CAGR: 7.1%

2016 – 2021 DPS CAGR: 2.1%

Newest DPS improve: 0.9%

Federal Realty is without doubt one of the bigger actual property funding trusts (REITs) in america. The belief was based in 1962 and concentrates on high-income, densely populated coastal markets within the US, permitting it to cost extra per sq. foot than its competitors. Federal Realty trades with a market capitalization of $8.3 billion at this time.

Previous to 2020, Federal Realty’s funds-from-operations had not dipped year-over-year at any level up to now decade, a tremendously spectacular feat provided that the belief operates within the extremely cyclical actual property sector. The corporate’s efficiency has normalized since, and Federal Realty is predicted to realize near-record earnings in Fiscal 2022.

Transferring ahead, we anticipate that Federal Realty’s development will likely be comprised of a continuation of upper lease charges on new leases and its spectacular growth pipeline fueling asset base enlargement. Margins are anticipated to proceed to rise barely because it redevelops items of its portfolio, and same-center income continues to maneuver larger.

Federal Realty options the longest dividend development streak amongst REITs, boasting 55 years of successive annual dividend will increase.

Supply: Investor Presentation

Is Federal Realty Prone to Lower its Dividend?

Federal Realty’s newest dividend improve of 0.9% was definitely disappointing, however we don’t imagine it indicators a possible dividend reduce. The corporate is more than likely simply being conservative within the face of a tricky actual property setting amid rising rates of interest. In addition to, Federal Realty is predicted to report near-record FFO/share in Fiscal 2022.

Moreover, it’s not the primary time a marginal dividend improve has occurred throughout a tricky market panorama. In 2009, Federal Realty elevated its dividend-per-share by only a cent (1.5%) to a quarterly fee of $0.66 earlier than dividend will increase re-accelerated as quickly as market situations normalized.

Federal Realty’s payout ratio stays fairly wholesome as effectively, presently standing under 70%.

Click on right here to obtain our most up-to-date Certain Evaluation report on Federal Realty Funding Belief (preview of web page 1 of three proven under):

#4 Realty Earnings Company (O)

Years of dividend development: 27

Dividend yield: 4.7%

2005 – 2011 DPS CAGR: 3.7%

2011 – 2016 DPS CAGR: 6.7%

2016 – 2021 DPS CAGR: 3.4%

Newest DPS improve: 0.8%

Realty Earnings is a REIT that has turn into well-known for its profitable dividend development historical past and month-to-month dividend funds. At the moment, the belief owns greater than 4,000 properties that aren’t a part of a wider retail growth (corresponding to a mall) however as a substitute are stand-alone properties. Which means its areas are viable for a lot of completely different tenants, together with authorities providers, healthcare providers, and leisure.

Realty Earnings has trademarked itself as “The Month-to-month Dividend Firm”, boasting 628 month-to-month dividends declared and 100 consecutive quarterly will increase.

Supply: Investor Presentation

Realty Earnings generates its development by means of rising rents at current areas, by way of contracted lease will increase or by leasing properties to new tenants at larger charges, but additionally by buying new properties. Administration invested about $2.1 billion in new properties in 2020 and one other $6.4 billion in 2021. Realty Earnings expects to extend its investments in worldwide markets through the subsequent couple of years.

Is Realty Earnings Prone to Lower its Dividend?

Much like Federal Realty, Realty Earnings’s newest dividend improve was below-average as administration is being conservative within the face of a tricky actual property setting amid rising rates of interest. We don’t imagine that Realty Earnings’s dividend security is threatened for a number of causes.

Firstly, at 76%, its payout ratio is definitely the bottom it has been in over a decade. Secondly, administration continues to develop the dividend a number of instances a 12 months (often quarterly), which additional cements their confidence within the dividend. Lastly, Realty Earnings’s properties are in excessive demand and can seemingly stay so. The occupancy fee throughout the portfolio is round 99%, and tenants typically report excessive lease protection ratios.

Click on right here to obtain our most up-to-date Certain Evaluation report on Realty Earnings Company (preview of web page 1 of three proven under):

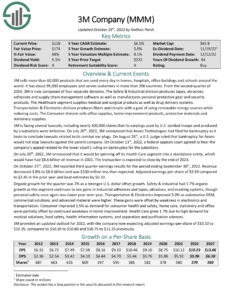

#3 3M Firm (MMM)

Years of dividend development: 64

Dividend yield: 5.0%

2005 – 2011 DPS CAGR: 3.5%

2011 – 2016 DPS CAGR: 15.0%

2016 – 2021 DPS CAGR: 5.9%

Newest DPS improve: 0.7%

3M sells greater than 60,000 merchandise which might be used day-after-day in properties, hospitals, workplace buildings, and colleges all over the world. It has about 95,000 workers and serves prospects in additional than 200 international locations. 3M consists of 4 separate divisions.

The Security & Industrial division produces tapes, abrasives, adhesives, and provide chain administration software program, in addition to manufactures private protecting gear and safety merchandise. The Healthcare phase provides medical and surgical merchandise in addition to drug supply programs.

The Transportation & Electronics division produces fibers and circuits with the aim of utilizing renewable power sources whereas decreasing prices. The Client division sells workplace provides, house enchancment merchandise, protecting supplies, and stationery provides.

3M has grown earnings at a fee of 5.4% per 12 months during the last decade. Easing uncooked materials/logistics/labor inflation and a stabilizing world provide chain setting are more likely to be constructive earnings development catalysts in 2023, in line with administration.

Supply: Investor Presentation

Is 3M Prone to Lower its Dividend?

3M is going through a number of lawsuits, together with almost 300,000 claims that its earplugs utilized by U.S. fight troops and produced by a subsidiary had been faulty. On December twenty second, a U.S. choose blocked 3M from making an attempt to dodge legal responsibility for accidents from its allegedly faulty earplugs by diverting blame to a subsidiary. The continuing state of affairs seemingly explains administration’s resolution to decelerate dividend will increase.

That mentioned, we imagine that 3M’s dividend ought to stay secure. Whereas dividend development has outpaced earnings development in recent times, the payout ratio stays under 60%. Additional, the corporate’s diversified portfolio of mission-critical merchandise ought to proceed to generate sturdy money flows no matter short-term headwinds within the economic system.

Click on right here to obtain our most up-to-date Certain Evaluation report on 3M Firm (preview of web page 1 of three proven under):

#2 Worldwide Enterprise Machines Company (IBM)

Years of dividend development: 27

Dividend yield: 4.7%

2005 – 2011 DPS CAGR: 21.4%

2011 – 2016 DPS CAGR: 13.7%

2016 – 2021 DPS CAGR: 3.6%

Newest DPS improve: 0.6%

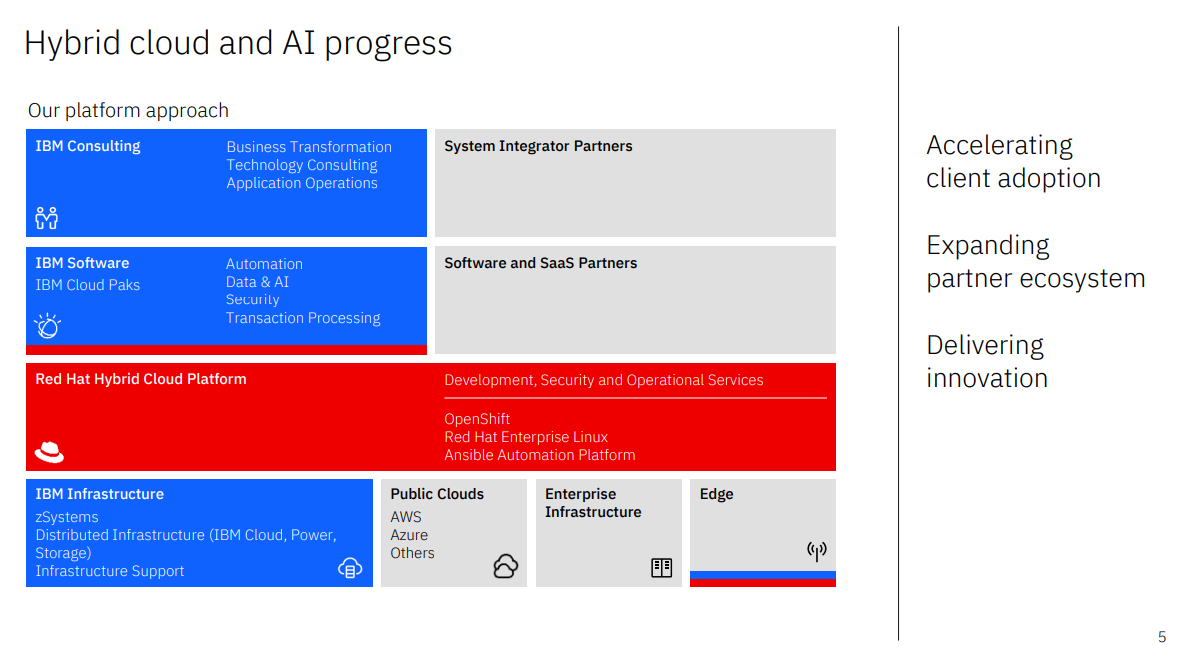

IBM is a worldwide data know-how firm that gives built-in enterprise options for software program, {hardware}, and providers. IBM’s focus is working mission-critical programs for giant, multi-national prospects and governments.

Final 12 months, IBM spun off Kyndryl, its managed infrastructure enterprise, however it’s nonetheless one of many largest IT providers corporations on the planet. The corporate now has 4 enterprise segments: Software program, Consulting, Infrastructure, and Financing. IBM had annual income of ~$57.4 billion in 2021 (not together with Kyndryl).

IBM’s core operations are worthwhile. However IBM had issue producing development up to now a number of years because of the transition to cloud and SaaS within the IT trade and IBM’s late emphasis on this market. Nevertheless, IBM is now specializing in cloud and SaaS and intends to be a serious participant within the hybrid cloud, as illustrated by the Crimson Hat and plenty of smaller acquisitions.

Supply: Investor Presentation

Is IBM Prone to Lower its Dividend?

IBM’s dividend development has slowed down considerably currently. This is smart, contemplating that the corporate is producing the identical free money circulate per share because it did 15 years in the past following years of declining revenues. We wouldn’t kill the potential for a dividend reduce within the medium time period if IBM’s revenues and earnings had been to proceed to say no, because the payout ratio has already climbed to 67%. That mentioned, constructive catalysts are in place that ought to maintain payouts, together with rising cloud revenues and continued deleveraging.

Click on right here to obtain our most up-to-date Certain Evaluation report on Worldwide Enterprise Machines Company(preview of web page 1 of three proven under):

#1 Walgreens Boots Alliance (WBA)

Years of dividend development: 47

Dividend yield: 5.1%

2005 – 2011 DPS CAGR: 22.4%

2011 – 2016 DPS CAGR: 14.7%

2016 – 2021 DPS CAGR: 5.3%

Newest DPS improve: 0.5%

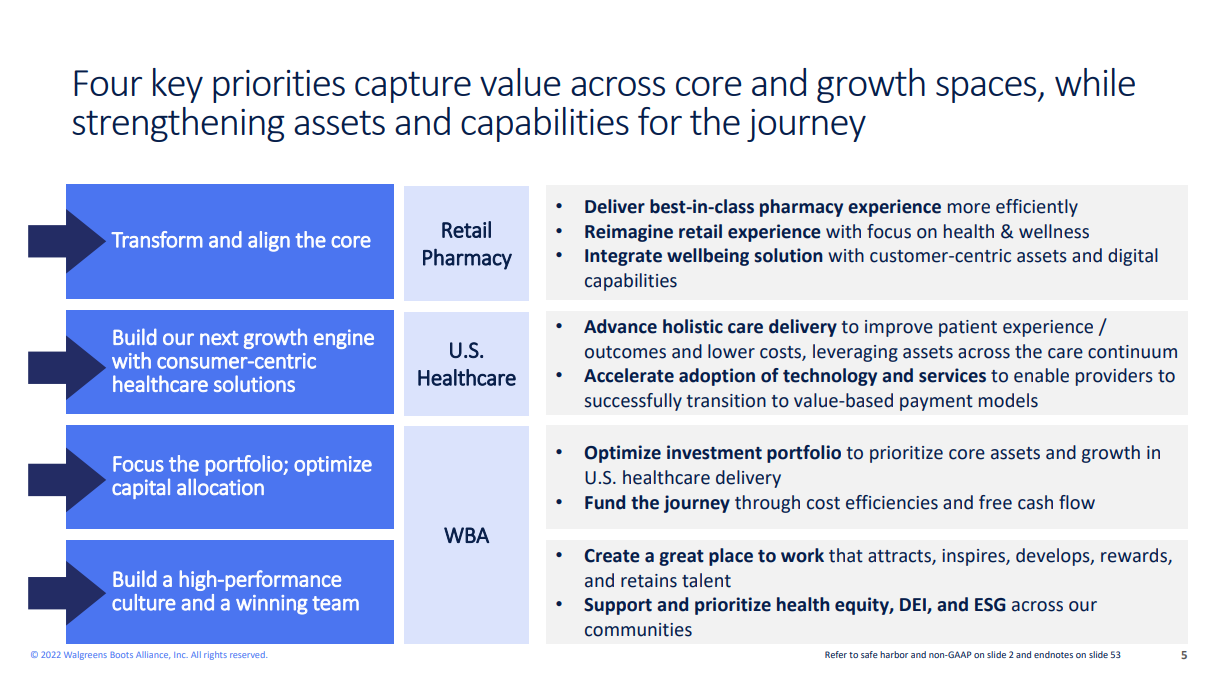

Walgreens Boots Alliance is the most important retail pharmacy in america and Europe. The $32.1 billion market cap firm has a presence in additional than 9 international locations by means of its flagship Walgreens enterprise and different enterprise ventures.

Walgreens’ earnings-per-share grew at a CAGR of seven.6% over the previous decade, powered by rising revenues and a declining share depend. This was pushed by a mixture of things, together with stable top-line development ($72 billion to $133 billion), a gradual web revenue margin, and a discount within the variety of excellent shares.

Supply: Investor Presentation

Is Walgreens Boots Alliance Prone to Lower its Dividend?

Walgreens has been rising its dividend by smaller and smaller quantities over time. That mentioned, we don’t imagine its 47-year dividend development is about to come back to an finish anytime quickly. With earnings-per-share rising considerably quicker than the dividend over the previous decade, the inventory’s payout ratio presently stands at 42%, decrease than 44% in 2012. As a consequence of promoting needed drugs and different prescribed drugs, we imagine the corporate will proceed producing stable money flows. They need to proceed to guard the dividend and even for additional dividend will increase forward, no matter their development fee.

Click on right here to obtain our most up-to-date Certain Evaluation report on Walgreens Boots Alliance (preview of web page 1 of three proven under):

Ultimate Ideas

Inspecting an organization’s dividend development fee pattern generally is a useful indicator for buyers trying to evaluate its monetary well being and dividend development prospects. A chronic slowdown within the tempo at which dividends are rising may sign that the corporate is experiencing monetary hurdles.

In that case, the corporate may probably be susceptible to a dividend reduce sooner or later, no matter how spectacular its dividend development streak is. We have now seen this occur greater than as soon as, with Pitney Bowes Inc. (PBI), AT&T Inc. (T), and Mercury Basic Company (MCY) ending their multi-decade dividend development monitor data as their financials couldn’t maintain their payouts additional. In all three circumstances, a dividend reduce was adopted by a steady deceleration in dividend development.

The eight Dividend Aristocrats mentioned on this article all noticed dividend development of lower than or equal to 1% in 2022, and plenty of have additionally proven a pattern of slowing dividend development over the long run. Whereas we can’t fully kill the potential for a dividend reduce for any of those corporations, we imagine that almost all, if not all of those Dividend Aristocrats, are presently not susceptible to reducing their dividends.

Whether or not it’s a scientific threat, like rising rates of interest within the case of Federal Realty Belief and Realty Earnings, or a systemic threat, like the continued lawsuit within the case of 3M, the comparatively tiny dividend will increase seen this 12 months amongst these Dividend Aristocrats can seemingly be attributed to the warning exercised by their administration groups.

In case you are enthusiastic about discovering extra high-quality dividend development shares appropriate for long-term funding, the next Certain Dividend databases will likely be helpful:

The foremost home inventory market indices are one other stable useful resource for locating funding concepts. Certain Dividend compiles the next inventory market databases and updates them month-to-month:

Thanks for studying this text. Please ship any suggestions, corrections, or inquiries to [email protected].

:max_bytes(150000):strip_icc()/What-difference-between-standard-Error-means-and-standard-deviation_color-1c203133aca641aca0d03936d9558693.jpg)

/what-difference-between-magnum-cum-laude-and-summa-cum-laude_V2-3ae02babdc714ea9adaeec0f0a6bf1a5.png)

{kind=link}