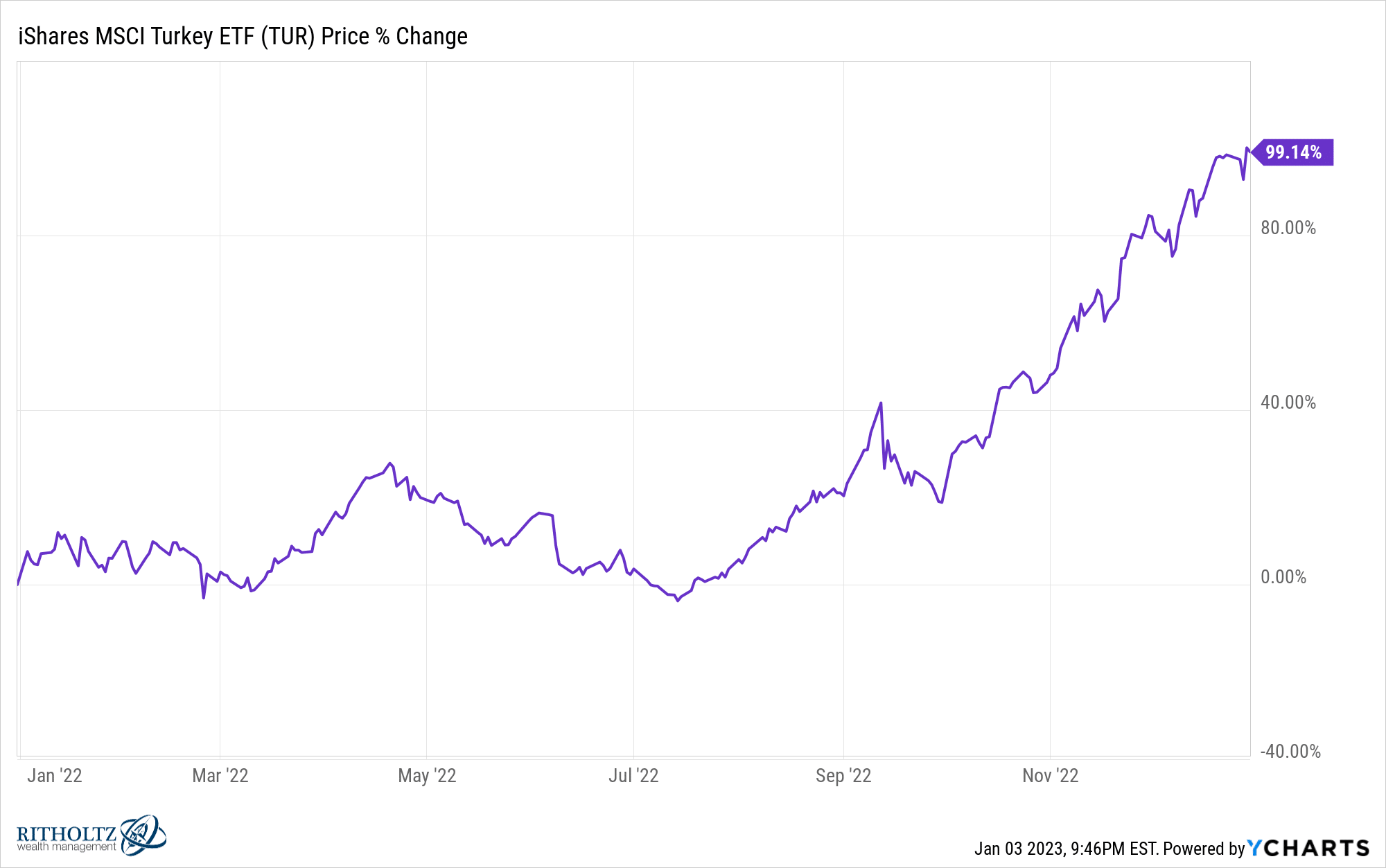

Should you’re a monetary advisor or a fund supervisor and also you weren’t down 20% final yr, you received, mainly. The S&P fell right into a 20% bear market whereas the Nasdaq crashed virtually 40%. Bonds had been down double digits as an asset class. Worldwide shares, whereas outperforming the US and never down as a lot, had been nonetheless down so much. Aside from Turkey, which inexplicably doubled final yr – right here’s the TUR ETF, up 99% in 2022.

I’d Google it to search out out why, however I don’t really feel prefer it. Possibly there’s no cause in any respect.

The Dow Jones Industrial Common was down lower than 10% due to bigger weightings towards vitality shares, however nobody owns the Dow Jones in the best way individuals personal the S&P 500. Proof? The SPY ETF has $356 billion in it and the index has tons of of big ETFs and mutual funds monitoring it. The DIA – Dow Jones model of SPY – has lower than a tenth of the AUM ($29 billion) regardless of having existed for simply as lengthy.

Anyway, the silver lining of this bear marketplace for us is that we acquired to indicate off the capabilities of all of the customized indexing and day by day, algorithmic tax loss harvesting we’ve been doing. Plus the advantage of working a tactical technique in tax-deferred accounts alongside our longer-term positions. Plus we raised a ton of cash from new purchasers who had gone into this mess with no nice advisor or a working monetary plan or any clue about tips on how to mitigate danger in a portfolio. We don’t root for bear markets, in fact, however we make certain they repay on the best way out. And it’s good to have constructive, productive actions to soak up a blood-red tape. That is the seventh bear market of my profession already, we all know tips on how to get by way of this stuff and what to do whereas we’re in them.

So, all issues thought of, this hasn’t been enjoyable however it should all work out in the long run. It at all times does, supplied no person does something silly or irreversible on our watch.

I used to be excited about the hierarchy of people that have been actually affected by the occasions (and worth motion) of 2022 and I assume I’d put staff of tech startups on the high of my checklist.

The rank and file startup employee has most likely acquired a variety of their compensation (and each day motivation) within the type of shares and inventory choices over the previous few years. In some circumstances they’ve even paid the taxes up entrance in order to not have to fret in regards to the positive aspects later. For this cohort, now staring down piles of nugatory or near-worthless shares in 1000’s of corporations, it’s been a horrible expertise. The layoffs received’t cease till the funding markets for enterprise fairness turn into extra forgiving, they usually received’t for the foreseeable future. Capital has gone from low-cost (and even free) to very costly. There is no such thing as a urge for food for this form of danger proper now. When the best firm on earth is on the verge of shedding half its market cap (as Apple appears to be headed for, in the meanwhile), how on earth might there be demand for the shares of a pre-revenue white board thought masquerading as a enterprise?

Keep in mind the times of “Oh you could have a slide deck and an ex-Google worker, right here’s $80 million in seed capital”? Effectively, as of late it’s the other. No seeds. Get away from my window.

The younger individuals who’ve flocked to those kinds of corporations are going to really feel this uncertainty essentially the most. The layoffs have solely simply begun. Subsequent are the wind-downs. That is when an organization is so hopelessly unprofitable and unlikely to be funded that the one accountable possibility is to simply cease. Take what’s omitted of the financial institution, return it to the traders and depart the keys. It takes years for this course of to cleanse the ecosystem of extra and arrange the subsequent era. The individuals with endurance to hold on till then come from household cash or have already been the beneficiaries of an exit or two from a previous cycle. You recognize who they’re. They’ve seven figures within the financial institution and a willingness to spend their time polluting Twitter with half-remembered Clay Christensen aphorisms and threads in regards to the exhausting factor about exhausting issues. They’ll do podcasts and hold forth about Ukraine till the Federal Reserve relents and the cash spigot activates once more. Mortimer, we’re again!

However the staff are sort of f***ed for the second. They most likely didn’t money something out or take any danger off the desk just like the founders have. They needed to put all of it on black and preserve it there whereas awaiting information on the subsequent funding spherical. That information isn’t coming. And there’s nowhere to go proper now, even in an economic system with one of many tightest labor markets ever. The biggest corporations in tech, media and telecom are all freezing hiring or shedding workers, so swimming towards a much bigger ship most likely received’t assist a lot within the quick time period.

After startup staff, I’d most likely most really feel unhealthy for the mortgage brokers and the realtors. They had been driving one of the thrilling bubbles of exercise and motion the housing market has ever seen. A twenty yr up-cycle all packed right into a span of simply twenty months. My favourite native realtor began filming himself making an attempt on Gucci belts within the mirror. And posting it.

The years 2020 and 2021 might need been two of the best years of all time for the housing sector. Dwelling costs rose 40%, finally topping out in June of 2022. It’s been straight down ever since. Costs should fall additional to sync up with prevailing rents. Present house gross sales have already begun fallen by way of the ground. Sellers have nowhere to go and no want to re-borrow at 6.5%. Patrons can’t rationalize the large improve in borrowing prices. Contractors can nonetheless promote newly constructed properties as a result of inventories are so tight, however the earnings from promoting a brand new home relative to the price of constructing it are nothing particular. The market has been put right into a deep freeze. Refinancings are achieved. Demand for mortgages is falling off a cliff. Transactions are vanishing. It’ll worsen this spring. The comps relative to final spring will likely be laughably unhealthy.

Right here’s Brian Wesbury and Robert Stein at FirstTrust writing in regards to the housing market:

The true impact of the change in rates of interest is clear within the present house market. Gross sales hit a 6.65 million annual price in January 2021, the quickest tempo since 2006. However, by November 2022, gross sales had been all the way down to a 4.09 million annual price, a drop of 38.5% to date. In the meantime a decline in pending house gross sales in November (contracts on present properties) indicators one other drop in present house gross sales in December.

Present house patrons have two main issues: first, a lot increased mortgage charges, which suggests considerably increased month-to-month funds. Assuming a 20% down fee, the rise in mortgage charges and residential costs since December 2021 quantities to a 52% improve in month-to-month funds on a brand new 30-year mortgage for the median present house.

You will get the remainder of their housing commentary right here.

So if a startup worker, be good and provide to flow into their resume round. And if a residential realtor who wasn’t ready for the 2021 atmosphere to alter so abruptly, give them a hug – they may use it proper about now. And if a mortgage dealer, properly, perhaps simply cross to the opposite aspect of the road if you see them coming. No eye contact. Simply let ’em cross and say, in low and reverent tones, “There however for the grace of God, go I.”

It’s a tricky atmosphere for most individuals proper now. Attempt to do not forget that it might at all times be worse.

***

Joyful New 12 months. Should you’re not sure of your present monetary plan or portfolio otherwise you’re in search of a second opinion or knowledgeable session, we’ve acquired a dozen Licensed Monetary Planners standing by to talk at your comfort. Don’t be shy, we do that all day for 1000’s of households throughout the nation. Ship us a observe right here:

Ritholtz Wealth Administration

:max_bytes(150000):strip_icc()/GettyImages-1137410599-cb10c321237243b88f5dc0eb206dacab.jpg)

:max_bytes(150000):strip_icc()/GettyImages-1448623832-52fc53ba20034936aaabf25ee6cff828.jpg)

{kind=link}