Mario Tama/Getty Photographs Information

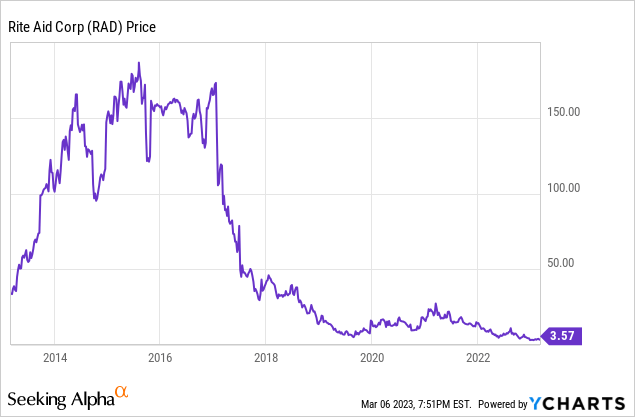

Ceremony Assist Corp. (NYSE:RAD) shareholders have endured horrible outcomes the previous couple of years and the longer term doesn’t look very promising both. Since my February 26, 2021 promote advice article RAD inventory has plunged 82%. To long-term RAD shareholders the present value of $3.57 is definitely about $0.18 per share after adjusting for the 2019 1-20 reverse inventory cut up. That’s all prior to now. Traders wish to examine what would possibly occur over the subsequent yr or two. Principally, I’m anticipating important dilution for present shareholders, or they could be fully wiped-out in a Ch.11 chapter course of. That is an replace to prior RAD articles.

Promote Inventory to Elevate Money = Dilution

With a purpose to keep out of chapter courtroom, in my view, Ceremony Assist must enormously cut back their debt. An alternate provide of inventory for debt is usually used to deleverage. One other method is to promote new shares and use the money to pay down debt. This methodology has turn out to be standard in the previous couple of years. AMC Leisure Holdings (AMC), for instance, has offered an enormous variety of new shares to pay down their debt. They went from having 109.3 million complete variety of A and B shares in August 2021 to 517.6 million shares at the moment, which doesn’t even think about the popular shares (APE).

Many RAD traders are questioning if the corporate may attempt to elevate a considerable amount of new money by way of huge new inventory providing one thing like Mattress Bathtub & Past’s (BBBY) providing in early February. BBBY deal was for over $1 billion, however it can improve the variety of BBBY shares excellent to nearly 900 million shares from 117.3 million. That means BBBY will obtain a median quantity of roughly $1.28 money per new share excellent. That may be a LOT of dilution. The center of the providing was the “sweetheart” deal provided to these establishments that purchased at the least $75 million underneath the providing, which successfully allowed them to buy BBBY shares considerably under the market value. The commerce by establishments was to promote quick BBBY inventory, take part within the sweetheart deal, after which use these low-cost shares to cowl their quick positions.

In concept Ceremony Assist issuing extra shares to boost money to pay down debt appears doable, but it surely might not be really easy. Ceremony Assist had 56,523,354 shares excellent as of December 22, 2022. The entire licensed shares are solely 75 million. Primarily based on my calculations utilizing the 2022 proxy assertion, a complete of 5.816 million shares both have been granted as a part of awards given or are reserved for future awards underneath incentive plans already authorized by shareholders. Which means solely about 12.6 million RAD shares could possibly be offered in a inventory providing with out receiving shareholder approval to extend the variety of licensed shares. With the inventory promoting at $3.57, that might suggest they may be capable of elevate about $45 million, which is a “token” quantity in comparison with their $3.2 billion in long-term debt.

Initially AMC didn’t face the necessity to get shareholder approval to extend the variety of licensed shares as a result of once they began promoting new shares, they have been already licensed to challenge 524.2 million shares, however when administration tried to get authorization to extend the quantity, they pulled the proposal for lack of shareholder assist. BBBY already had authorization for 900 million shares.

If Ceremony Assist tries to hunt shareholder approval to extend the variety of their shares excellent, they won’t have the component of shock that was related to the BBBY inventory sale. I do not, nevertheless, see any organized “meme” dealer opposition to RAD shareholders voting to extend the quantity.

Assuming for a second that they do get authorization to extend the variety of shares and are profitable promoting them, there could possibly be huge dilution for present RAD shareholders. Noteholders and holders of Ceremony Assist debt may gain advantage by utilizing the money raised to pay down debt, however there may be a repeat of a S&P dedication that Ceremony Assist technically “defaulted”, which I coated in a July RAD article.

The clock is working towards Ceremony Assist. Previously the corporate has filed their proxy for the annual assembly round Could 21 with a voting document date roughly June 2. The shareholder conferences are often held the final of July. That’s a very long time earlier than a possible for a vote on the rise within the licensed shares. There’s, nevertheless, the opportunity of a particular assembly could possibly be referred to as a lot earlier underneath the corporate’s by-laws (textual content of the by-laws) to vote particularly on this matter.

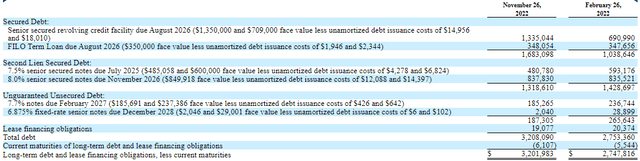

Debt Discount

Ceremony Assist would get extra “bang for his or her buck” by shopping for again debt promoting at steepest low cost to par and/or closest to maturity. Assuming that they’re able to elevate a major amount of money by way of a inventory provide, what are the restrictions on what debt could be paid down? The amended revolver “permits for the voluntary repurchase of any debt or different convertible debt, as long as the Presently Efficient Services should not in default and the Firm maintains availability underneath its revolver of greater than $375.95 million”, in keeping with their newest 10-Q.

Lengthy-Time period Debt

sec.gov

Their revolver has a present credit score restrict of $2.850 billion, which was elevated by $50 million final December 1, and as of November 26, 2022, they borrowed $1.335 billion underneath the revolver. This suggests that they had $1.515 billion nonetheless obtainable on the finish of November. Initially it might appear that there’s loads of room for them to have the ability to repurchase debt underneath the $375.95 million restriction. There are, nevertheless, two issues. First, Ceremony Assist has been burning money and borrowing extra. They burned up $318.852 million money from operations for the 9 months ending November 26, 2022. Second, if outcomes worsen within the close to future the revolver restrict may get decreased.

Having an enormous inventory providing most definitely would enormously profit debt holders, together with holders of seven.7% 2/15/2027 unsecured notes (CUSIP 767754AJ3). These unsecured notes are extraordinarily dangerous as a result of there’s a excessive likelihood that if Ceremony Assist doesn’t elevate new money by way of a inventory/rights providing and it continues to burn money that it could possibly be in Ch.11. Underneath a Ch.11 reorganization plan, in my view, it’s unlikely unsecured notes would get any restoration as a result of there’s simply an excessive amount of debt that has a precedence for recoveries, until they obtain a “reward” from a better precedence class. I might additionally count on RAD shareholders can be worn out underneath a Ch.11 reorganization plan.

Some Elements That May Affect 4Q Outcomes

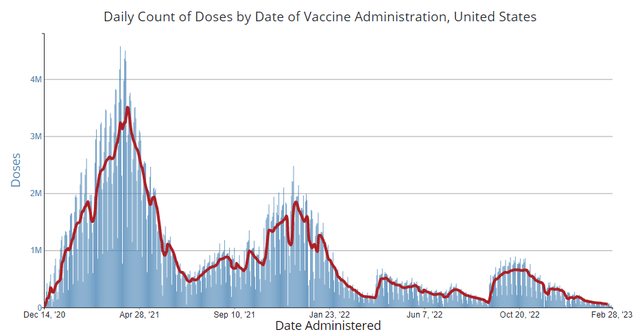

The optimistic affect of Covid-19 vaccines on Ceremony Assist continues to drop to a really low quantity. The chart under is for all Covid-19 vaccines within the U.S. and never only for Ceremony Assist, but it surely does give the overall thought of the vaccines administered at Ceremony Assist shops. In addition to the income from the vaccines, there’s elevated foot visitors into Ceremony Assist shops and that always leads to different purchases. With out the income associated to Covid-19 vaccines, 4Q may evaluate negatively to 4Q 2022 fiscal yr’s outcomes.

covid.cdc.gov/covid-data-tracker

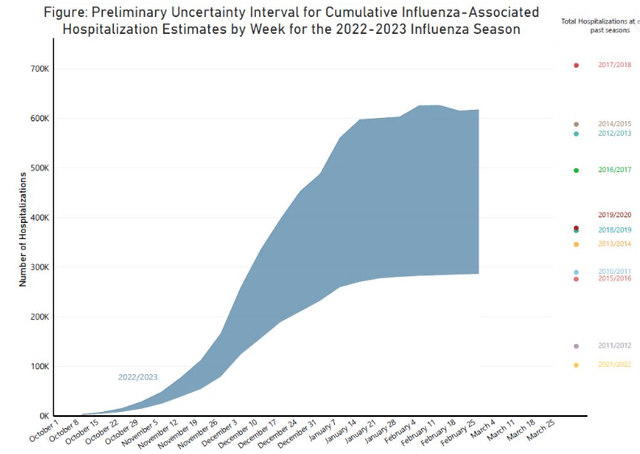

The 2022/2023 flu season appears to be a lot worse than the prior yr. The quantity on the desk under for 2021/2022 flu season is the underside proper determine. The chart itself is for estimates, which has a really broad estimate vary, of hospitalizations, however the estimates do point out that there most definitely will probably be a major variety of shoppers searching for drugs at Ceremony Assist shops in the course of the 4Q. This needs to be a significant optimistic for Ceremony Assist because it ought to improve foot visitors.

www.cdc.gov/flu

Conclusion

Since I’m anticipating a recession beginning in 2Q or early 3Q and Ceremony Assist is extraordinarily leveraged, the corporate might must take drastic steps to maintain out of chapter courtroom. I coated points in prior articles about promoting Elixir and I believe elevating money by way of an enormous inventory providing could be their greatest hope at this level.

Whereas a inventory providing would assist debt holders, I’m not recommending the acquisition of their unsecured notes due to the chance of not getting any restoration if Ceremony Assist does finally file for Ch.11. I’m sustaining my impartial/maintain advice on RAD inventory as a result of there’s nonetheless the potential of a turnaround or some white knight using in to purchase them. Traders should perceive that RAD is a really dangerous commerce.

:max_bytes(150000):strip_icc()/What-difference-between-standard-Error-means-and-standard-deviation_color-1c203133aca641aca0d03936d9558693.jpg)

/what-difference-between-magnum-cum-laude-and-summa-cum-laude_V2-3ae02babdc714ea9adaeec0f0a6bf1a5.png)

:max_bytes(150000):strip_icc()/nikola_badger2-28963695a2fae6f2920734d1af0bdf3f1917c5d6e1826ad26d2bfe2cd6686ec9-c201b13fd17a462fa091b2cd28882980.jpg)

{kind=link}