JTSorrell

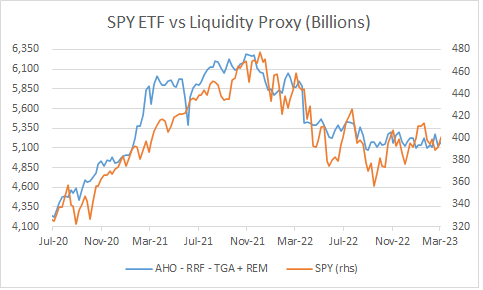

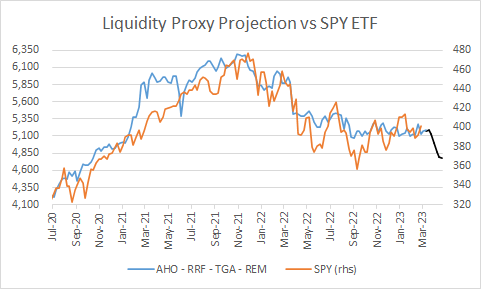

Because the begin of the pandemic, the markets, particularly the SPDR® S&P 500 ETF Belief (NYSEARCA:SPY) appear to be transferring in sync with greenback liquidity characterised by the proxy for liquidity measured in its hottest kind by the Whole measurement of the Federal Reserve steadiness sheet minus the quantities “trapped” within the Treasury Basic account and the Reverse Repo facility of the Federal Reserve.

I gained’t go into the main points of why greenback liquidity is so necessary for the evolution of asset inflation or deflation as this text could be excessively lengthy however right here you will discover a superb thread by Andy Constan explaining the underlying dynamics.

On this article I might use a barely totally different definition that appears to trace the habits of the market extra precisely by utilizing complete Securities held outright by the Federal Reserve as an alternative of the Whole measurement of the federal reserve. I might additionally add the liquidity offered by the FED because it began dropping cash round September final 12 months as a result of the yield on their steadiness sheet holdings is right this moment a lot decrease than the yield it’s paying on their liabilities. And that hole in apply its paid with newly created {dollars}.

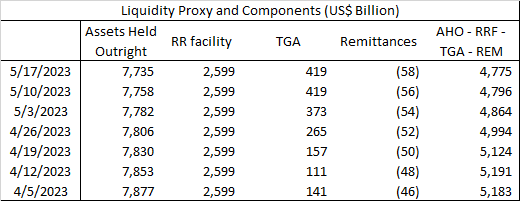

So, the definition that I might use is as follows: Property Held Outright – Treasury Basic Account – Reverse Repo Facility – Remittances As a consequence of US Treasury

A few caveats, the primary one is that instantly subtracting remittances to the components is a simplification as in regular occasions (when the fed is earning money) that variable works as a circulate of cash that periodically leaves the fed and partially funds the US Treasury. However when the FED begins dropping cash it begins working as a steadiness of the entire amassed losses because the FED can’t ask for that cash from the US Treasury. It merely prints that cash and register the amassed losses as an accounting entry. When the numbers the place optimistic they stayed at very low ranges that made them immaterial to the total addition of phrases, that’s the reason I merely used the entire knowledge sequence to simplify the calculations, so technically an error however an immaterial one.

The second is that some would argue that the total measurement of the steadiness sheet of the FED is a greater proxy than Property Held Outright, and that measure has been closely affected by the emergency loans noticed over the past couple of weeks. That’s actually debatable however no less than from my perspective an emergency mortgage is a short lived growth of liquidity with an outlined maturity date for the counterpart who’s unlikely to make use of that liquidity to develop threat taking and doubtless desires to rapidly repay that mortgage as its utilization is seen as an indication of fragility. All of the parts of the definition that I take advantage of are indefinite expansions or contractions of liquidity, that don’t impose any dedication on the counterpart receiving the liquidity, one thing that might be known as unencumbered liquidity.

And the relation to SPY seems like this because the begin of the pandemic.

Chart 1 (Fred St Louis Fed & Alphavantage)

Into the Particulars

The main target of this text is on the implications of tax season on the anticipated build-up of the Treasury Basic Account and the results for this proxy of liquidity assuming the Federal Reserve continues with its quantitative tightening plans and a steady stage of the quantity “trapped” within the Reverse Repo Facility.

To do that I might be utilizing mainly two further datasets offered by the U.S. Treasury. The primary one is the desk known as Deposits and Withdrawals of Working Money from the Day by day Treasury Assertion (DTS) Report and the second is the U.S. Authorities Income Collections Report.

The primary one exhibits the each day deposits and withdrawals to the Treasury Basic Account with vital element rounded to the closest million. And I’ll focus virtually solely on two gadgets affecting the Treasury Basic Account; the deposits denominated Public Debt Money Points (Desk IIIB) and the withdrawals denominated Public Debt Money Redemp. (Desk IIIB) to isolate the affect of internet debt issuance on the Treasury Basic Account Stability.

The second dataset exhibits the each day Authorities Income Collections and classify every of these collections as both Non-Tax, IRS Non-Tax and IRS-Tax and I might focus solely on those categorised as IRS-Tax to isolate the affect of taxes on the Treasury Basic Account Stability. These revenues are by far an important of the three classes representing between 79% and 87% p.c of the entire revenues of the US Treasury relying on the financial actuality of every 12 months, with good years on the excessive facet of that vary and unhealthy years on the low facet. So, for 2023 tax season that displays the financial atmosphere of 2022 I count on Tax Income to be on the excessive facet of that vary.

For many of all the approaching evaluation I might concentrate on years 2011 to 2019 and 2022 to go away out years closely affected by the Nice Monetary Disaster and the years 2020 and 2021 as in these years the tax season calendars had been altered to accommodate the difficulties arising from the pandemic.

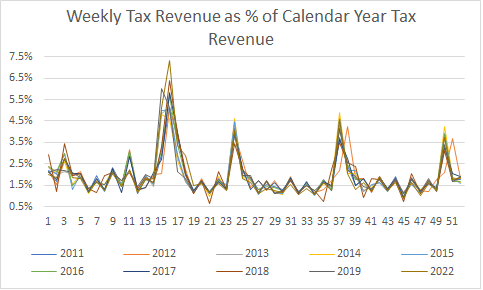

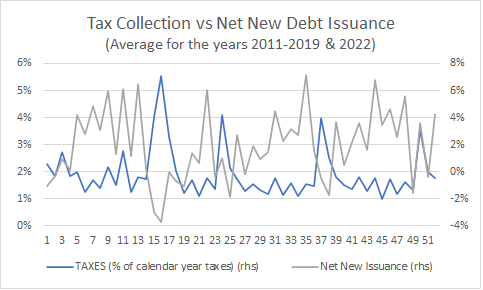

On the next chart we will see that the cadence of tax income assortment exhibits a really clear annual seasonality throughout these years, so going ahead I might use the common of these years as it’s a truthful illustration of the years underneath evaluation.

Chart 2 (Fiscal Information – Treasury.gov)

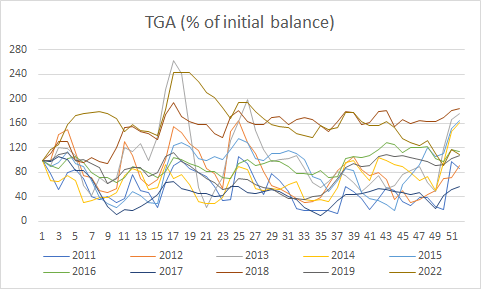

For the TGA the sample is undeniably messier, however you may clearly see the bumps through the intervals wherein tax income assortment is concentrated.

Chart 3 (Fred Stlouisfed)

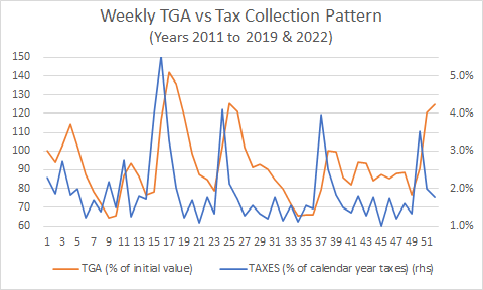

And while you use the common seasonality of each sequence, the affect of tax collections on the quantity of liquidity trapped within the TGA turns into a lot clearer.

Chart 4 (Fred St Louis FED & Fiscal Information – Treasury.gov)

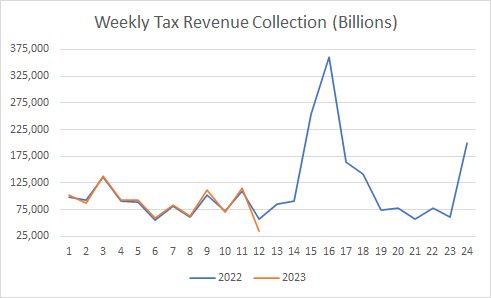

And we’re mainly one week away from the beginning of the height tax assortment interval, the 4-weeks that focus the largest improve within the treasury normal account of the 12 months. Estimating the quantity of tax collections for this 12 months is way more durable, however even after sure changes like those that occurred to tax brackets to replicate inflation, taxing happens over an financial system that in apply works in nominal {dollars} so I might assume that one thing like 2022 is cheap and for the primary 12 weeks of the 12 months that has been the case.

Chart 5 (Fiscal Information – Treasury.gov)

The earlier chart concentrates within the first 24 weeks of the calendar 12 months to offer a better take a look at the interval underneath evaluation. In the course of the first 12 weeks of this 12 months, tax collections have amounted to 1,048 billion and through the identical interval of 2022 tax collections amounted to 1,043 billion. Trying ahead to the crucial 4-week interval underneath dialogue (weeks 15 to 18) tax collections amounted to 920 billion in 2022 and that very same interval noticed a rise within the TGA from 547 to 945 billion, so a internet improve in trapped liquidity of $398 billion.

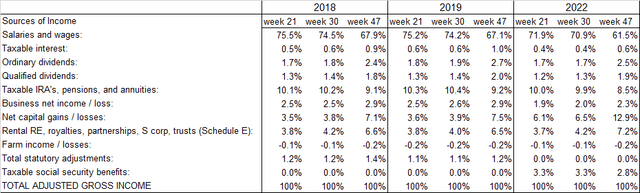

However to double-check if that assumption is cheap, I used the statistics offered by the IRS to grasp the composition of the person taxable earnings for years 2022, 2019 and 2018. It is helpful that the statistics for these tax seasons are separated into 3 time intervals: tax collections as much as week 21, as much as week 30 and as much as week 47 of the calendar 12 months.

Chart 6 (IRS)

Immediately you may see that the parts usually are not precisely the identical and due to that the comparisons usually are not good between years, however these parts are comparatively immaterial (statutory adjustment & Taxable social safety advantages). Other than that. it is clear that Salaries and Wages are by far an important element and the element with the largest soar in 2022 vs 2018-19 its Web Capital Achieve / Losses.

Utilizing conservative assumptions (making an attempt to not overestimate complete gross earnings) for the present 12 months I might assume that Salaries and Wages elevated 5%, Taxable curiosity doubles, Capital Features halves and all different parts keep on the similar stage. With that, I get to a gross adjusted earnings stage for the primary 21 weeks of the 12 months that’s 0.9% larger than 2022.

After that comes all of the credit and deductions however truthfully, I will not get into these as I clearly wouldn’t have the experience to make assumptions for these parts.

There are additionally two different related accounts in these reviews: Taxes due at time of submitting and Whole refunded overpayments. And for 2018-19 these added to internet tax refunds of between $180 and $188 million {dollars} however for 2022 it amounted to solely $101 million internet refunds. I wouldn’t have a transparent understanding of the supply of that divergence however to be further conservative I might assume a return to the one thing nearer to 2018-2019, and I’ll impute the total distinction in money influx to the US TREASURY to the 4 weeks underneath evaluation, so $830 billion for this 12 months as an alternative of the $920 billion collected in 2022. Decreasing the build-up within the TGA from $398 in 2022 to $308 billion this 12 months.

And eventually, it is necessary to acknowledge that these particular person taxes made up between 82% and 75% of complete IRS-TAX income acquired by the US treasury for the primary 21 weeks of 2018 and 2019, and solely 63% for the 12 months 2022, so clearly there’s vital affect of different taxes affecting complete tax income collections, however I couldn’t discover clear statistics for different sources like companies.

With all of that, please take into account that the estimation of $830 billion in tax collections and consequently for the build-up in TGA balances for this 12 months has a major underlying stage of uncertainty.

Affect of internet new debt issuance

However there’s one other issue to contemplate and people are the deposits associated to internet new debt issuance coming into the TGA, that requires moving into the weeds of the DTS report talked about beforehand. This database is tougher to completely perceive as there have been many modifications through the years by way of reporting, however the modifications usually are not mirrored on the older set of datapoints. So, I centered solely on the information from 2013 to the current day.

Throughout that interval, I added up all deposits aside from gross new debt issuance (Public Debt Money Points (Desk IIIB)) as most of these deposits exit to pay for debt that’s maturing all via the 12 months (Public Debt Money Redemp. (Desk IIIB)).

To that quantity I added solely the quantity of debt that was not used to payback maturing debt (Web New debt Issuance). That’s complete Treasury Income plus the financing of the fiscal deficit, so mainly a proxy of fiscal spending.

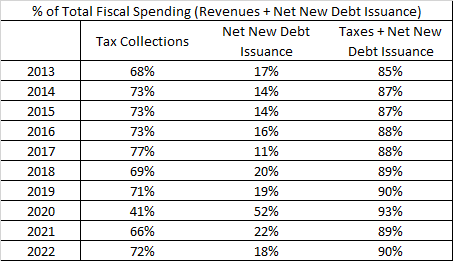

And within the following desk you may nonetheless see that tax collections proceed to be an important driver, however internet new debt issuance additionally has a cloth affect relying on the dynamics of the fiscal deficit.

Desk 1 (Fiscal Information – Treasury.gov)

The Debt Ceiling

In line with the Congressional Funds Workplace (CBO) the fiscal deficit ought to quantity to $1.4 trillion in 2023, that will indicate a weekly cadence of recent debt issuance of roughly $27 billion if it was achieved uniformly alongside the calendar 12 months. That may imply that through the 4-week interval underneath evaluation the US authorities must be getting an extra influx associated to internet new debt at a tempo of $108 billion, however they’re prohibited from doing so after hitting the debt ceiling weeks in the past.

So, if the sample of internet new debt issuance has traditionally been achieved evenly through the 12 months that will imply that this 12 months limitation ought to blunt the affect of tax assortment from $308 to $208 billion. However has the sample of internet new debt assortment occurred steadily throughout the calendar 12 months?

Apparently not.

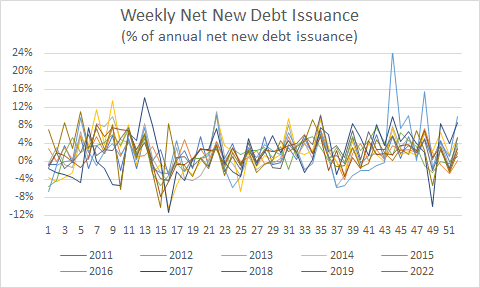

The next chart exhibits the seasonality of internet new debt issuance and once more there appears to be a sample.

Chart 7 (Fiscal Information – Treasury.gov)

Once you take a look at the common of these years in opposition to the common of the sample for tax collections you may clearly see that the US Treasury consciously seeks to blunt the results of the tax assortment peaks on liquidity by reducing internet new debt assortment throughout these intervals.

Chart 8 (Fiscal Information – Treasury.gov)

That exhibits that the historic will increase within the TGA steadiness which can be seen in chart 4 occurring in parallel with tax assortment peaks are the results of these tax collections and NOT of internet new debt issuance. So, the lack to challenge internet new debt through the 4-week interval underneath evaluation is irrelevant as a result of that has all the time been the case throughout that interval.

With that out of the way in which let’s get to the implications for the market underneath a sure set assumption.

The Assumptions

Whole Tax collections of $830 billion for the interval of week 15 (ending April 16) to 18 (ending Might 5) of 2023. A build-up on the TGA of $308 billion from week 15 to week 19 (ending Might 14). A continuation of the FED QT program. A steady quantity trapped within the Reverse Repo Facility. A creation of recent {dollars} at a tempo of roughly $2 billion by the FED to pay for the hole between the yield of its property and its liabilities. The restrict by counterpart to make use of the reverse repo facility stays unchanged.

The Market Implications

From round April 5 to 10, 2023, to some level between Might 5, 2023 and Might 14, 2023 the market ought to expertise a major lower in greenback liquidity of roughly $416 billion. That’s composed of a 308 billion improve within the TGA, $118 billion discount in Property Held Outright within the FED steadiness sheet and roughly $10 billion improve in liquidity coming from the brand new {dollars} required to pay the detrimental hole between the yield on property within the portfolio of the FED and the price of their liabilities. And that could be a lot!

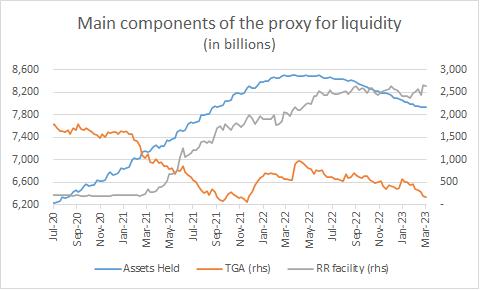

As of the final report (April 5) the liquidity proxy (Property Held Outright – Treasury Basic Account – Reverse Repo Facility – Remittances As a consequence of US Treasury) stood at $5,183 billion. And as you may see in chart 1 it has acted because the gravity for the market. It’s also attention-grabbing to see that the liquidity proxy stopped falling by early October 2022 coinciding with the lows for the market reached round mid-October.

And by wanting on the most vital parts of the proxy for liquidity within the subsequent chart you may see that the rationale for that stability could be discovered primarily within the discount of the TGA steadiness that has fully nullified the results on liquidity of the QT program of the FED and since the quantity of liquidity trapped on the reverse repo facility stopped rising across the similar time.

Chart 9 (Fred St Louis Fed)

I count on the TGA to maintain draining for another week, how a lot it is onerous to say however for arguments sake let’s say that by a $30 billion for the following week. So, lets challenge the next weeks underneath the assumptions beforehand described and see how chart 1 seems with that projection.

Desk 2 (Writer Projections) Chart 10 (Fred St Louis Fed, Alphavantage & Writer Projections)

Dangers

A very powerful threat for the thesis is that the quantity trapped in Reverse Repo Facility may transfer in a dramatic manner that may counteract the entire sample that I’m projecting. I believe that’s unlikely because it has proven stability for nearly a 12 months as you may see on chart 9, nevertheless it’s attainable. A factor to trace is the potential for the fed decreasing the restrict by counterpart, if that had been to occur it may sharply cut back the quantity trapped within the reverse repo facility no less than quickly.

Other than that it’s the potential for tax season collections coming in a lot decrease than my estimation. That could be a threat, however in any case, the sample ought to nonetheless be there however might be considerably blunted.

And eventually, if the fed ends QT or extra importantly begins QE once more all of the conclusions of this text could be void.

Conclusion

With the approaching tax assortment peak every week away, underneath assumptions based mostly on historic patterns, it’s extremely possible that the proxy for liquidity ought to have a really vital discount to ranges not seen since late 2020. And if the affect of liquidity within the markets stays as vital as has been through the previous 3 years there’s additionally a really a transparent threat for a major correction for the markets.

To be clear, I count on that correction to be brief lived as a result of after tax season with the lack to challenge internet new debt the TGA must be drained comparatively rapidly including again that trapped liquidity into the financial system. After that, the largest occasion by way of liquidity (assuming QT stays in place) ought to come from the eventual lifting of the debt ceiling as new debt issuance could be concentrated in a comparatively small interval producing a brand new potential large hiccup for the market by way of liquidity.

I’m open to any constructive criticism as my goal is to proceed deepening my very own understanding of the entire liquidity topic. Thanks for studying!

:max_bytes(150000):strip_icc()/senior-couple-snuggling-56a437be3df78cf77281530c.jpg)

:max_bytes(150000):strip_icc()/What-difference-between-standard-Error-means-and-standard-deviation_color-1c203133aca641aca0d03936d9558693.jpg)

/what-difference-between-magnum-cum-laude-and-summa-cum-laude_V2-3ae02babdc714ea9adaeec0f0a6bf1a5.png)

{kind=link}