Printed on April tenth, 2023 by Nikolaos Sismanis

Buyers in search of a reliable and constant supply of revenue might discover it advantageous to spend money on firms that distribute month-to-month dividends. This will tremendously improve predictability and cut back the uncertainty related to investing in equities. Thus, month-to-month dividend shares might be notably in the course of the present, extremely unstable market setting.

That mentioned, there are simply 86 firms that presently supply a month-to-month dividend fee, which may severely restrict the investor’s choices. You’ll be able to see all 86 month-to-month dividend paying names right here.

You’ll be able to obtain our full Excel spreadsheet of all month-to-month dividend shares (together with metrics that matter, like dividend yield and payout ratio) by clicking on the hyperlink under:

One title that now we have not but reviewed is First Nationwide Monetary Company (FNLIF), a Canadian-based firm that operates within the monetary providers trade. At present, the inventory comes connected to a yield of 6.4%, which is greater than 4 instances larger than the yield of the S&P 500 Index. Coupled with the truth that the corporate pays out dividends on a month-to-month foundation, it could be a becoming choose for income-oriented buyers.

This text will consider the corporate, its enterprise mannequin, and its distribution to see if First Nationwide Monetary Company may very well be an excellent candidate for buy.

Enterprise Overview

Over the past three a long time, First Nationwide has grown to turn into a acknowledged and revered chief in actual property financing. Being Canada’s greatest non-bank issuer of single-family residential mortgages, the corporate offers a complete array of mortgage options tailor-made to swimsuit the distinctive necessities, life-style, and monetary goals of every consumer.

Moreover, First Nationwide presents industrial mortgages, attributing its triumph to its group of specialists who’re among the many most revered and famend within the trade.

As an originator and underwriter of mortgages, 2022 was a transitional 12 months for First Nationwide. The trade underwent a fast transformation as a result of vital rise in rates of interest, resulting in a pointy deceleration in housing exercise. This stands in stark distinction to 2021 when the housing market skilled heightened exercise because of traditionally low-interest charges ensuing from the federal government’s financial coverage aimed toward mitigating the financial fallout of the Covid-19 pandemic. Consequently, First Nationwide’s single-family and industrial originations had been 17% and 1% decrease, respectively, year-over-year.

Whereas larger rates of interest negatively impacted the variety of new originations final 12 months, they did have a reasonably optimistic revenue on the corporate’s outcomes.

In reality, the favorable end result of the upper charges greater than compensated for the headwinds it created. This was as a result of firm with the ability to earn larger curiosity income on mortgages held for securitization and investments, leading to a exceptional 13% development in revenues to C$1.57 billion. Following larger revenues, First Nationwide’s revenue earlier than taxes landed at C$269.1 million in 2022 in comparison with C$263.8 million in 2021.

Supply: Annual Report

Progress Prospects

To develop its revenues and earnings, First Nationwide can primarily depend on two elements – increasing its mortgage portfolio and rising the curiosity revenue generated from it.

The issue is that assessing First Nationwide’s development prospects is considerably difficult nowadays as a result of extremely unsure nature of the evolving rates of interest. At first look, the corporate’s revenues and revenue final 12 months rose final 12 months as the corporate was in a position to earn extra on its current mortgage portfolio.

That mentioned, rising rates of interest are usually not helpful for mortgage issuers for just a few causes:

First, when rates of interest rise, it turns into dearer for potential consumers to take out mortgages, which may end up in decrease demand for mortgages. We noticed this taking place within the firm’s 2022 outcomes.

Second, First Nationwide might expertise a lower in profitability, as larger rates of interest can result in larger borrowing prices for the corporate as effectively. This wasn’t the case final 12 months, however it may very well be as soon as the corporate has to refinance its personal debt.

Third, as rates of interest rise, some debtors might discover it troublesome to make their mortgage funds, which may end up in a rise within the variety of defaults. This, in flip, may cause mortgage issuers to undergo losses as they might must repossess and promote properties at a loss.

Due to this fact, regardless of final 12 months’s enhancing outcomes, it’s essential to notice that if rates of interest stay excessive, the corporate’s profitability might not be as robust within the upcoming years.

Total, the corporate’s earnings monitor file is sort of unstable, which might be attributed to varied elements which have the potential to influence its profitability relying on the prevailing macroeconomic situations considerably.

Nonetheless, First Nationwide’s earnings are likely to pattern upward over the long run. The corporate’s earnings-per-share over the previous 5, seven, and ten years have grown on common by -1%, 9.6%, and 6.3%, respectively.

Dividend Evaluation

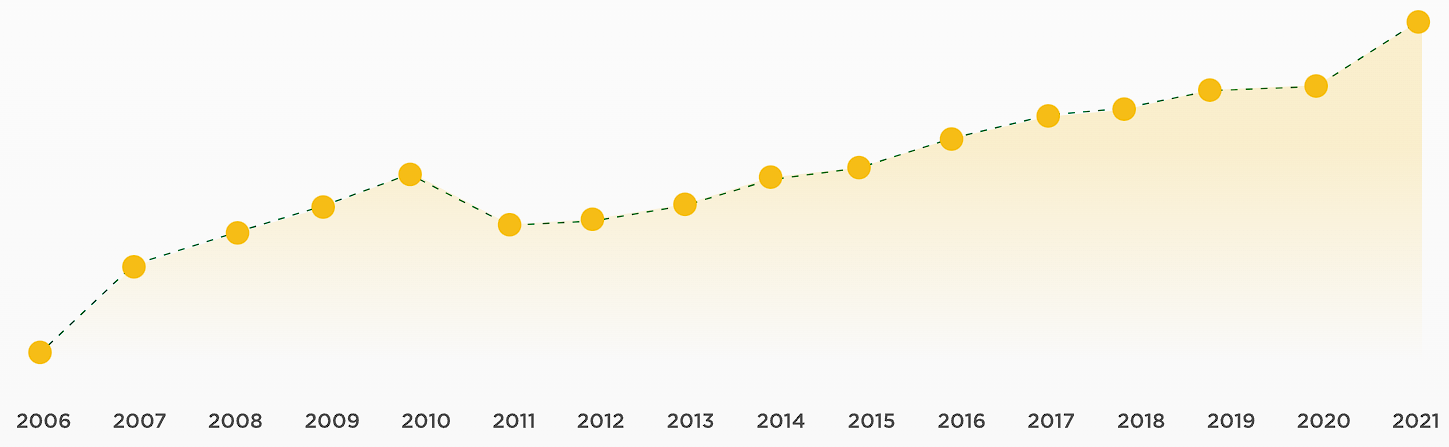

First Nationwide is presently yielding 6.4%, with the corporate boasting a exceptional monitor file of paying dividends. In reality, First Nationwide is a member of the S&P/TSX Canadian Dividend Aristocrats Index.

Though the dividend skilled a lower of roughly 20% in 2010 as a result of opposed influence of the Nice Monetary Crises on the actual property mortgage market, the dividend has grown steadily yearly from 2011 onward.

Particularly, over the previous decade, the corporate’s dividend has grown at a compound annual development fee of 6.4%, mirroring its earnings-per-share development over the identical interval.

Supply: Investor Relations

Shifting ahead, we consider that First Nationwide might decelerate the tempo at which it grows its dividend. It’s because the present payout ratio already seems comparatively excessive at 72%, and profitability might decline within the coming years because of larger rates of interest.

Due to this fact, the corporate is unlikely to take the danger of pushing the payout ratio to a degree that would jeopardize its monetary stability. The latest dividend enhance of simply 2.1% helps this rationale.

Remaining Ideas

First Nationwide is more likely to expertise profitability headwinds within the coming years, particularly if rates of interest stay elevated. Whereas larger curiosity revenue on its current mortgage portfolio might considerably offset the dearth of latest originations, the corporate’s personal monetary bills are more likely to strain its backside line.

That mentioned, for buyers in search of a gradual stream of month-to-month revenue and an above-average yield, First Nationwide could also be a sexy possibility. Regardless of working in a difficult setting, the corporate has maintained an inexpensive payout ratio and even barely elevated its dividend final 12 months, indicating its dedication to rewarding its shareholders.

As such, income-oriented buyers are more likely to discover worth within the inventory albeit any short-term setbacks in its financials because of larger rates of interest.

If you’re excited about discovering extra high-quality dividend development shares appropriate for long-term funding, the next Certain Dividend databases can be helpful:

The key home inventory market indices are one other stable useful resource for locating funding concepts. Certain Dividend compiles the next inventory market databases and updates them month-to-month:

Thanks for studying this text. Please ship any suggestions, corrections, or inquiries to [email protected].

{kind=link}