Sundry Pictures

Funding Thesis

Nokia Oyj (NYSE:NOK) managed to shift its enterprise away from cellphones connecting folks, to connecting the world via the community infrastructure, and quick 5G speeds making it one of many leaders in connectivity globally. With the latest full-year outcomes introduced, the corporate managed to show round from being an unprofitable enterprise just some years in the past to delivering fairly spectacular outcomes. The share worth has not mirrored the turnaround in any respect, and the group appears to be sleeping on it.

With implausible enhancements in margins and the three-phase plan properly on its strategy to acceleration, the administration’s tone was very upbeat about steady enchancment in margins over the subsequent phases of the plan. I’ll briefly contact on some alternatives that the corporate has sooner or later enlargement of their enterprise, I’ll current a DCF evaluation which is able to see an enchancment in working margins over the subsequent decade with solely slight progress in revenues, as I imagine margin enlargement will play the most important function. Based on the mannequin, which continues to be on the conservative aspect, the corporate is a purchase at these ranges, nevertheless, seeing that the corporate has gone nowhere by way of inventory worth appreciation, the true potential of the corporate is probably not reached for fairly some time.

FY2022 Outcomes

The corporate delivered very strong full-year outcomes, beating analysts’ estimates. All segments of the enterprise noticed y-o-y gross sales will increase; nevertheless, the theme was largely targeted on the corporate’s enchancment of margins, which the administration expects to proceed going ahead as the corporate turns into extra environment friendly and leads the market sooner or later in all their reported segments.

How Can the Firm Propel Itself Ahead?

NOK has been lagging behind the broader market and its rivals by fairly a bit. The destructive sentiment for the corporate would possibly stem from the assumption that the corporate is completed. It’s going the way in which many large gamers of the previous have gone, finally submitting for chapter like Blockbuster or Kodak. I don’t suppose that is the case in any respect for the corporate any longer, as the corporate managed to shift its enterprise fully and have become one of many large gamers within the networking trade. I imagine the explanation for the shortage of affection for the corporate is that plenty of traders might not know what NOK is even doing anymore.

Three out of the 4 reportable segments have skilled margin expansions, apart from Nokia Applied sciences, which noticed a slight contraction, nevertheless, working margins are within the mid-70s there and don’t contribute that a lot to gross sales but, because it accounts for round 5%-7% of whole revenues generated. The administration within the newest earnings name mentioned that the corporate filed an extra 1,700 patents on new concepts, so I imagine the longevity of this phase goes to be round for some time and can hold steadily rising over time.

There may be plenty of progress within the 5G area for the corporate. In the identical earnings name, the administration mentioned it already noticed “implausible double-digit progress in India” in that regard and it’s predicted that it’s simply ramping up till 2024, and at that time, the expansion will begin to present a secure revenue for the community gamers like NOK. The corporate goes to learn from increased adaptation charges of 5G networks all over the world. It’s not going to cease there as there are already plans for 6G infrastructure specs to be launched in 2025, Nokia is seeking to be on the forefront of that innovation already, coupled with the corporate’s different applied sciences that assist networking change into extra environment friendly like AI and machine-learning, NOK appears to be positioned fairly properly sooner or later and I do not see it disappearing any time quickly. The corporate in my view is initially of a fantastic turnaround story. The query is, are folks going to note that it managed to shift its enterprise so efficiently?

One other manner that the corporate can unlock shareholder worth is by shopping for again shares. For my part, an organization that generates a lot in FCF ought to be capable to make many extra buybacks than the present €600m approved by the board. The identical goes for the dividend, which has been elevated to .12 cents. It’s nonetheless fairly small for a corporation like NOK.

The most important driver of worth unlocking of NOK is the three-phase technique that was introduced by then the brand new CEO Pekka Lundmark again in October 2020, simply a few months after he took the reins of the corporate. It appears just like the technique has labored very properly to this point. Already the corporate has left the primary section, which was “reset”, and now the corporate is onto the subsequent section – “speed up”. The “speed up” stage has been going very properly, as the corporate noticed substantial will increase in profitability and effectivity, which in flip positioned it significantly better for altering markets and aligning with buyer wants. The administration was all in regards to the margin expansions on their newest earnings name and the theme seems to be the identical going ahead as the corporate is seeking to obtain at the least 14% working margins. I did not hear of any potential timeline for when the corporate expects to realize it however from taking a look at how the three-stage technique has been creating, I would not be shocked if it reaches 14% by year-end or early subsequent yr. The final stage of the plan is “scale”, which suggests the corporate wish to change into the market chief within the segments it’s working. If the corporate continues its acceleration stage efficiently going ahead, NOK can change into very environment friendly in its operations and can acquire a aggressive benefit over its closest rivals for my part, primarily constructing itself a robust moat sooner or later and turning into a frontrunner.

Financials

The corporate has a really large money place which covers the long-term debt excellent. I like seeing firms that may cowl their obligations with simply the money available, which suggests the corporate is not going to have any liquidity issues and curiosity bills on debt are properly coated. The money place permits the corporate to increase its operations additional, purchase again shares or improve the dividend. Money could be very versatile in that regard.

Talking of liquidity, the corporate’s present ratio has been strong all through latest years and has improved barely within the final couple of years. The corporate doesn’t have any issues paying off its short-term obligations.

Present Ratio (Personal Calculations)

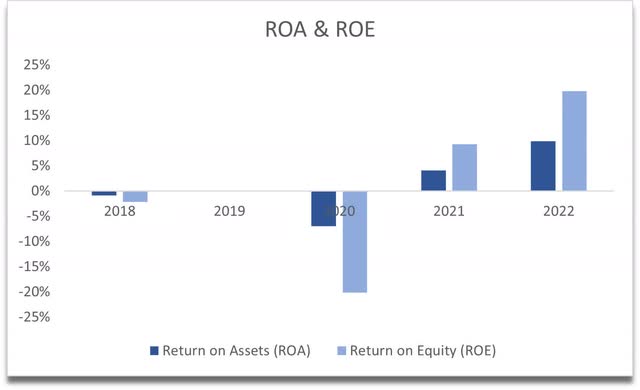

The place it exhibits that the corporate has made a 180 is how way more environment friendly and worthwhile it turned because the announcement of the three-phase technique and because the new CEO got here into energy. ROA and ROE went from deep within the negatives to very respectable positives, which means that the initiatives have been profitable. These initiatives are nonetheless ongoing, and I’d anticipate to see even higher numbers going ahead.

ROA and ROE (Personal Calculations)

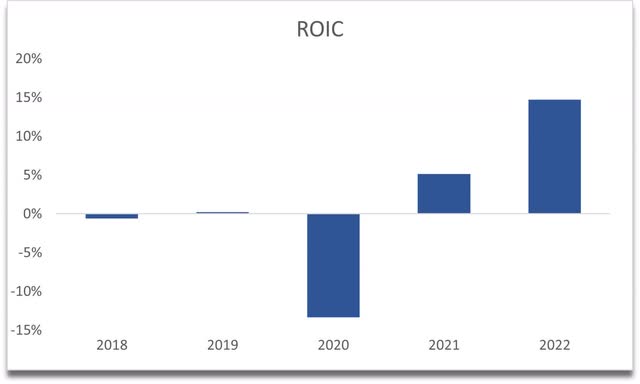

The corporate has additionally managed to realize optimistic returns on capital. The administration’s skill to spend money on optimistic NPV tasks has been profitable and it’s bearing fruit. ROIC is getting increased, which suggests the corporate is having fun with a aggressive benefit and a good moat. It is probably not the kind of aggressive benefit that its rivals have been having fun with, nevertheless, if the corporate continues this trajectory, I imagine it could change into the chief.

ROIC (Personal Calculations)

I will hold an in depth watch on how these metrics above will develop over time. The corporate has a really wholesome stability sheet in my view, with barely elevated leverage which is not a lot of an issue contemplating the free money circulate that the corporate manages to generate greater than covers curiosity bills. I do not see how the corporate wouldn’t be capable to climate any kind of downturn within the brief run.

Valuation

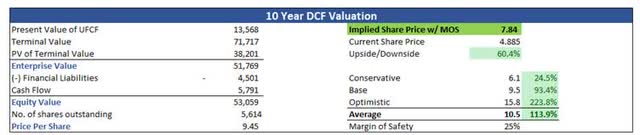

I made a decision to piggyback off the administration’s ambition to succeed in at the least 14% of working margins. I modeled the corporate’s financials and determined to steadily improve effectivity to round 12% by the yr 2032, which is way more conservative than the administration’s expectations. I wished to see what the corporate’s intrinsic worth can be if NOK falls wanting its expectations. As typical, my fashions are available in 3 eventualities, so I get a spread of potential outcomes for the corporate’s valuation. For the conservative case, working margins attain 10.6% which nonetheless exhibits an enchancment of 70bps from present margins. The optimistic case sees working margin enhancements to round 13%, which continues to be under the administration’s short-term goal.

For income assumptions, I saved to a easy linear decline in progress from 5% in ’23 to 2% by ’32. Below these assumptions on the bottom case, the income will increase to round $37B by ’32. On the optimistic and conservative instances I both lowered the assumptions by 2% or elevated them by 2%.

The above conservative assumptions coupled with a robust stability sheet require a 25% margin of security to be added to the calculations in my view. If the corporate manages half of what it’s anticipating to realize sooner or later, which is increasing working margins to 14%, the corporate with a 25% margin of security is value $7.84 a share, implying a 60% upside from present valuations.

10-year DCF Valuation (Personal Calculations)

In Conclusion

The corporate appears to be on sale proper now. With sturdy money circulate era, the brand new three-phase plan is working properly. The corporate managed to pivot its enterprise fully from the place it was all these years in the past. The danger can be that folks’s sentiments might not change the way in which the corporate shifted its enterprise for the optimistic. Many individuals, after they hear of Nokia, get an image of a 3310 of their heads and the way the corporate hasn’t executed something since. That’s removed from the reality of what the corporate has change into since then and the place it’s headed sooner or later. I have not thought in regards to the firm in years. I used to be a type of individuals who thought it was an organization that didn’t adapt for the long run and received swept by the meme mania for a second there, which prompted me to look into the corporate in additional element out of curiosity to see what it was as much as.

Is the corporate going to succeed in its potential? If folks notice it’s not a telephone firm any longer then sure it might, nevertheless, the corporate has been buying and selling on this vary for some time now and it might proceed. I’m going to attend a pair extra months and see what occurs within the financial system. On this form of surroundings, all shares are very unstable and should current a greater entry level for the long-term investor.

:max_bytes(150000):strip_icc()/What-difference-between-standard-Error-means-and-standard-deviation_color-1c203133aca641aca0d03936d9558693.jpg)

/what-difference-between-magnum-cum-laude-and-summa-cum-laude_V2-3ae02babdc714ea9adaeec0f0a6bf1a5.png)

{kind=link}