Michael Vi/iStock Editorial through Getty Photographs

Overview

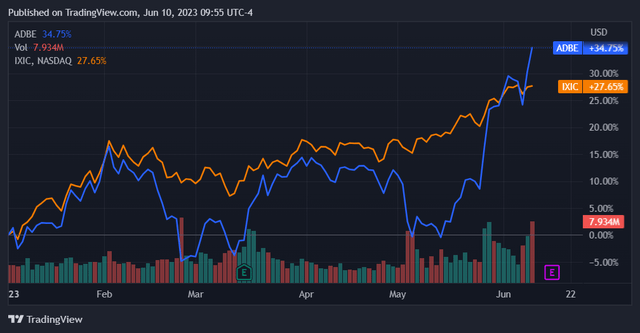

Adobe (NASDAQ:ADBE) is slated to launch its Q2 2023 earnings outcomes 5 days from now, on Thursday June fifteenth. Within the run-up to those outcomes there has already been motion in Adobe inventory, with the earlier week seeing the inventory achieve 5.34% whereas the NASDAQ Composite (COMP.IND) closed flat.

In search of Alpha

Curiously, this latest appreciation has prolonged a multi-week rally to convey Adobe’s value return previous that of the NASDAQ Composite for the primary time this yr.

In search of Alpha

Given latest information objects across the inventory, together with analyst upgrades and commentary on its capability to learn from AI, it isn’t instantly clear that this latest shopping for signifies market optimism round its upcoming outcomes. The timing of the latest rally additional compounds the issue of figuring out the character of its present value motion. The present rally that has introduced Adobe’s YTD return past the index started on the finish of Might, over two weeks earlier than earnings and at the least every week previous to its latest AI product launch or analyst improve bulletins. This timeframe is shut sufficient to the earnings report date for the latest shopping for to be linked to investor earnings expectations.

In both case, now we have a inventory with vital momentum (32% month-to-date) that’s now days away from releasing an earnings report. This sort of state of affairs, through which the volatility of a inventory is rising going into earnings, works to arrange the inventory for a stronger value response to the earnings outcomes that it finally ends up releasing. This definitely appears just like the case for Adobe this time round.

With this context in thoughts, I imagine that Adobe might want to meet or exceed consensus earnings expectations with the intention to keep the present rally in its shares. A miss towards expectations would halt its momentum and subsequently consequence within the evaporation of its latest positive factors. Because of the vital pre-earnings value motion that we’re seeing, it’s clear that momentum may be very a lot in play right here and must be thought-about as the first drive figuring out share value within the near-term.

As such I believe it’s value evaluating the place expectations stand for Adobe’s Q2 2023 earnings and if we are able to glean any indicators as to the outcomes that it’ll put up. This could present an instantly actionable view on the inventory’s trajectory.

Earnings Expectations

For this present quarter, Adobe is predicted to put up a GAAP EPS of $2.72 and revenues of $4.77B. These estimates are fairly near Adobe’s efficiency in its prior quarter (Q1 2023), throughout which it had generated a GAAP EPS of $2.71 and revenues of $4.66B. We are able to examine these ahead estimates towards Adobe’s latest/historic outcomes with the intention to decide the expansion charges and margins which are implicit inside the forecast.

Anticipated revenues of $4.77B suggest 8.76% y/y development from Q2 2022. That is priced to mirror a seamless lower within the agency’s development fee that’s nonetheless fairly near its latest y/y charges of income development. Since there hasn’t been a fabric change in circumstances for the corporate, I believe this estimate is truthful.

Finally, Adobe has not accomplished and built-in its Figma acquisition or had the time to convey AI merchandise into the market. Since these are the 2 main development catalysts for Adobe, however should not but in play, we are able to readily assume that development ought to stay on an analogous trajectory within the instant.

In search of Alpha

In search of Alpha

Continuing to EPS estimates, we see that the anticipated GAAP EPS determine of $2.72 implies 9.24% y/y development from Q2 2022. This could signify earnings per share development past that which Adobe has generated since This autumn 2021. Current quarters don’t facilitate conviction on this EPS estimate as a result of they’ve y/y EPS development far under what is predicted on this upcoming quarter.

In search of Alpha

In search of Alpha

Since there’s not an instantly obvious trendline we should take a look at Adobe’s margin profile to see how possible this stage of projected EPS development actually is. Expanded margins inside the previous yr would enable for larger EPS at related ranges of income, presenting a route for Adobe to hit consensus EPS development targets.

Sadly the margin story right here seems to be entering into reverse. Adobe’s margins have gotten worse over the previous 4 quarters. This implies Adobe has beat latest EPS estimates by means aside from bettering its margins, in actual fact counteracting this detrimental drive on its profitability.

In search of Alpha

Adobe achieved this by share buybacks. The final two quarters have seen an acceleration of its share repurchase program that has labored to maintain per-share profitability excessive.

In search of Alpha

In search of Alpha

The present share repurchase program had $5.2B remaining for share repurchases as of final quarter’s earnings report, with this system licensed to run till the tip of 2024. Moreover, the newest quarter noticed $1.4B in share repurchases executed by Adobe.

Assuming that Adobe has continued to repurchase shares on the identical fee because it did final quarter, we are able to calculate the influence on per-share earnings from the discount in float that this may have achieved.

At its present market cap of $208.25B and its present float proportion of 99.7%, we get $207.63B in whole float for Adobe.

If Adobe repurchased $1.4B of this $207.63B float, it could have diminished its whole float by 0.67%.

We are able to then take this quantity and use it to create an adjusted denominator. We are able to then divide final quarter’s EPS into this adjusted widespread shares excellent denominator to see what EPS can be on the new float, all else held equal.

This calculation is as follows:

$2.71/(1 – 0.0067) = $2.71/0.9933 = $2.73

This exhibits that Adobe can hit consensus EPS estimates (and maybe even exceed them by one cent) purely by its share repurchasing program. Given the latest acceleration in its share repurchases I believe Adobe would have definitely continued to repurchase shares finally quarter’s fee, maybe even rising its ranges of shopping for considerably. General this provides me confidence that Adobe has what it must proceed by this upcoming earnings report in stride. Merely put, the maths is sound.

Danger

The dangers till and thru this subsequent earnings report are twofold. The primary is that Adobe’s income development fee might sluggish sooner than anticipated, making the maths unworkable for sustaining its EPS by share repurchases. This could yield an earnings miss for the upcoming report and generate instant detrimental repercussions for its shares.

The second threat is that if we see additional deterioration in Adobe’s internet margins, that are already far off from historic highs. Whereas they’re nonetheless fairly excessive in an absolute sense, extra stress right here might very properly unwind the current equation of share value repurchases and subsequent EPS will increase that Adobe is counting on. This could crimp its capability to readily hit consensus and in the end have the identical downward share value impact talked about above.

Lengthy to medium-term, the chance round Adobe inventory takes on a unique type. We should keep in mind that its present share repurchase program will run out on the finish of 2024 on the newest, which might drive the corporate to allocate extra capital for additional repurchases or to extend its earnings by margin enhancements.

Usually the present state of affairs right here is extra precarious than I would really like. It’s clear that earnings can be down considerably with out the buybacks, and ongoing low ranges of margin compression are one other long-term concern. I wish to see a extra natural development profile earlier than committing for the long-term.

Conclusion

I believe that Adobe can and can outperform towards consensus estimates within the quarter forward, which ought to result in continued tactical appreciation in its share value. The mathematics is sort of sound and the bar for outperformance just isn’t excessive. As talked about, even mirroring final quarter’s efficiency would see the agency pull forward of consensus GAAP EPS by one cent at an an identical stage of buybacks.

Additional forward, nonetheless, I’m far much less sure. I might be very eager to see a extra natural development profile and a extra sturdy driver of earnings development than share buybacks for Adobe. Contemplating this, I believe Adobe is a tactical purchase however not a long-term one at current. General I do really feel comfy calling it a purchase heading into earnings.

:max_bytes(150000):strip_icc()/What-difference-between-standard-Error-means-and-standard-deviation_color-1c203133aca641aca0d03936d9558693.jpg)

/what-difference-between-magnum-cum-laude-and-summa-cum-laude_V2-3ae02babdc714ea9adaeec0f0a6bf1a5.png)

{kind=link}