Khanchit Khirisutchalual

Sadly, the Fed hasn’t but figured this out, however I strongly suspect they may earlier than too lengthy. In the meantime, standing pat, because the FOMC did immediately, is the least worst different to easing. Rates of interest are comparatively excessive from an historic perspective, however there are as but few—if any—indicators that financial coverage is just too tight or that it’s threatening the well being of the financial system. The truth that the year-over-year change within the CPI (now 4.0%) continues to be above the Fed’s 2% goal is meaningless, when a glance below the hood exhibits that this measure of inflation will virtually definitely fall to 2% (or decrease) throughout the subsequent a number of months.

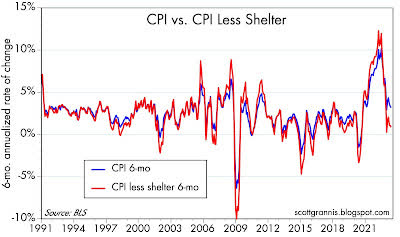

Chart #1

Chart #1 compares the 6-mo. annualized change within the CPI to the identical change within the CPI much less shelter prices. In response to the latter, inflation has already fallen to 0.8%. As I’ve been arguing for the previous a number of months, the measure of shelter prices (e.g., rents) used within the CPI lags the fact of the housing market by about 18 months. In the true world, housing costs haven’t elevated at everywhere in the previous 12 months, however the CPI is assuming they’ve been rising. So eradicating shelter prices from the CPI is fully professional. With out shelter prices artificially inflating the CPI, inflation would already by considerably lower than the Fed’s goal. And if that does not persuade you, then have a look at the truth that over the previous six months, the CPI has risen at solely a 3.2% annualized fee, and it is virtually assured to fall additional by the tip of the 12 months as shelter prices flip detrimental.

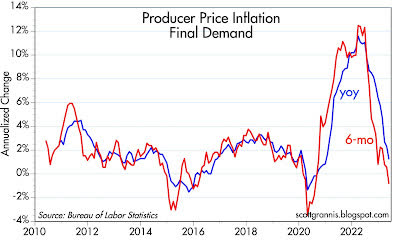

Chart #2

Chart #2 exhibits the 6- and 12-mo. annualized change within the Producer Worth Index for Last Demand. This index is comprised of issues that inhabit the early phases of the inflation pipeline, and right here we see that inflation is already comfortably beneath 2%.

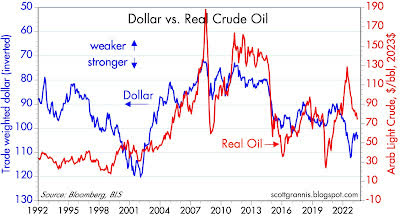

Chart #3

Chart #3 compares the worth of the greenback (inverted) to the inflation-adjusted value of crude oil. Two issues to notice: commodity costs have a robust tendency to maneuver inversely to the worth of the greenback—a stronger greenback tends to push commodity costs down, and a weaker greenback tends to push commodity costs up. As we speak, the greenback is comparatively robust vis a vis different currencies, and commodity costs are usually weak. Crude costs are down virtually 40% since final summer time’s peak, and the CRB Uncooked Industrials index (a broad measure of non-energy commodity costs) has fallen to ranges which prevailed over a decade in the past. In actual phrases, oil immediately prices about half of what it did a decade in the past. Low cost vitality could be a highly effective tonic, selling financial well being.

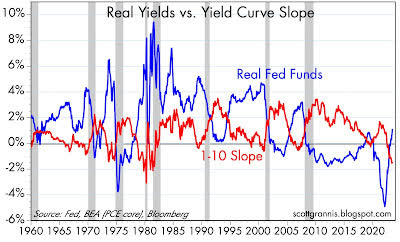

Chart #4

Chart #4 compares the true Fed funds fee (the true measure of how excessive rates of interest are) to the slope of the Treasury yield curve. Be aware that each recession on this chart was preceded by an enormous improve in actual rates of interest (blue line) and a big inversion of the yield curve (pink line). As we speak the yield curve is certainly inverted, however actual rates of interest usually are not but punishingly excessive, so by this standards a recession will not be but baked into the cake. And as I’ve famous in prior posts, credit score and swap spreads are nonetheless fairly low, which additionally means that recession threat is low.

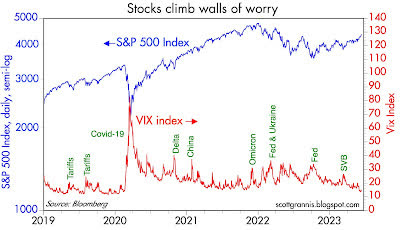

Chart #5

Chart #5 compares the extent of the S&P 500 (blue line) to the extent of the VIX (worry) index. Right here we see that the market has been shifting up from its low of final September on the similar time that the VIX index has been declining from 31 to now solely 14. Fears are subsiding, and the inventory market is respiratory a sigh of aid. The market is aware of it is just a matter of time earlier than the Fed wakes up and begins easing.

Authentic Submit

Editor’s Be aware: The abstract bullets for this text had been chosen by Looking for Alpha editors.

{kind=link}