CalypsoArt

Introduction

As a dividend progress investor, I search funding alternatives in income-producing belongings, primarily shares. I often add to current positions after I discover them engaging. I additionally make the most of market volatility by beginning new positions to diversify my holdings and improve my dividend revenue for much less capital.

Waste Administration (NYSE:WM) is an attention-grabbing firm to research. The corporate is an industrial firm with factories and sophisticated logistics, but its enterprise isn’t as cyclical as most industrial firms. The corporate solves a major problem as folks create rising quantities of waste.

I’ll analyze Waste Administration utilizing my methodology for analyzing dividend progress shares. I’m utilizing the identical methodology to make it simpler to match researched firms. I’ll look at the corporate’s fundamentals, valuation, progress alternatives, and dangers. I’ll then attempt to decide if it is a good funding.

Searching for Alpha’s firm overview exhibits that:

Waste Administration offers environmental options to residential, industrial, industrial, and municipal clients in america and Canada. It gives assortment providers, together with selecting up and transporting waste and recyclable supplies from the place it was generated to a switch station, materials restoration facility (MRF), or disposal web site, and owns and operates switch stations, in addition to owns, develops, and operates landfill services that produce landfill gasoline used as renewable pure gasoline for producing electrical energy.

Fundamentals

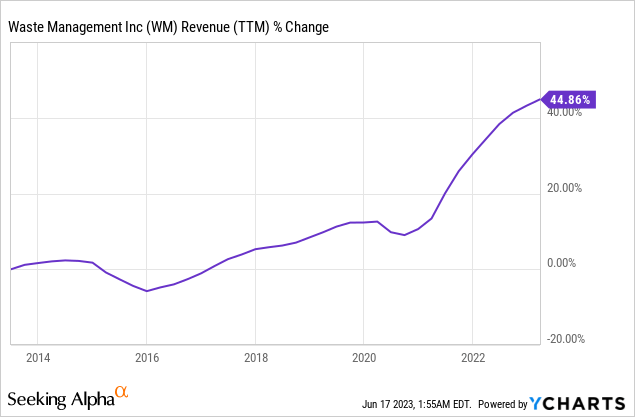

The revenues of Waste Administration have elevated by 45% over the past decade. The explanations for the rise in gross sales have been value will increase, service enlargement to extra shoppers, and the corporate providing further providers like renewable power. Sooner or later, as seen on Searching for Alpha, the analyst consensus expects Waste Administration to continue to grow gross sales at an annual charge of ~6% within the medium time period.

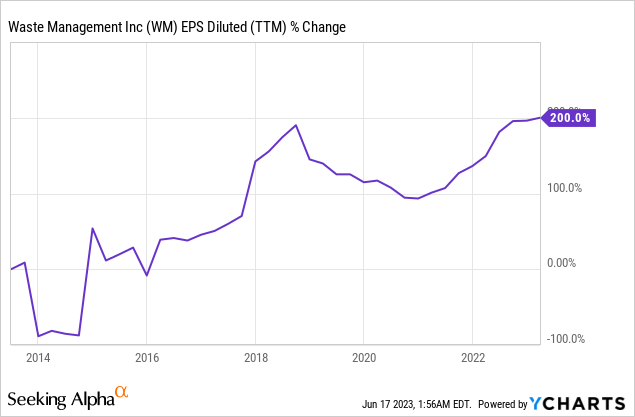

The EPS (earnings per share) over the identical interval has elevated by 200%, which suggests it tripled in simply ten years. EPS progress has been a lot quicker as the corporate grew gross sales, elevated costs, and minimize prices to enhance margins and purchase again shares. The corporate retains enhancing stable waste margins via disciplined pricing and price controls to maintain rising the margins. Sooner or later, as seen on Searching for Alpha, the analyst consensus expects Waste Administration to continue to grow EPS at an annual charge of ~11% within the medium time period.

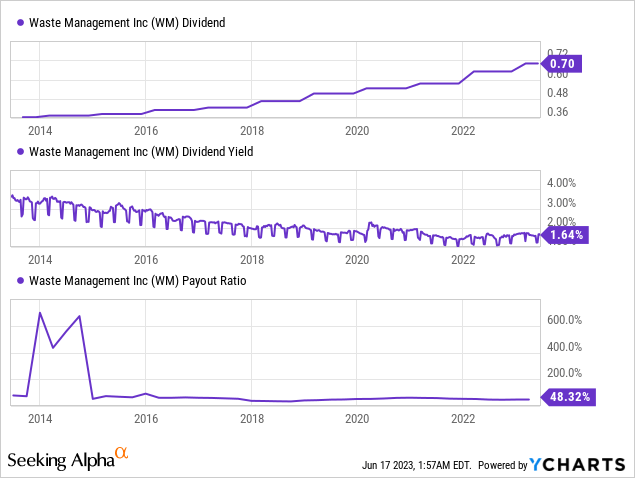

The dividend is likely one of the firm’s crown jewels. It has been rising the dividend steadily for 19 years and has not diminished the dividend for extra 4 years prior. The dividend fee might not look extraordinarily engaging with the yield at 1.64%, however it’s probably protected. The present payout ratio leaves sufficient room even when the EPS decline. Wanting ahead, buyers ought to anticipate the corporate to continue to grow its dividend at round 11% yearly, which aligns with the corporate’s forecasted EPS progress charge.

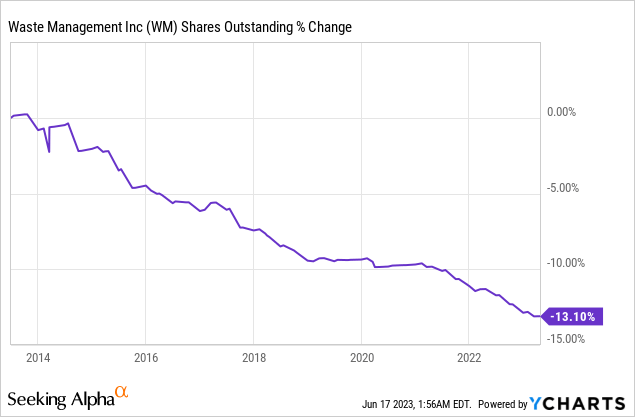

Along with the dividend, the corporate returns capital to shareholders through buybacks. These share repurchase plans help EPS progress by decreasing the variety of excellent shares. During the last decade, the variety of shares decreased by 13%. Waste Administration is shopping for again shares, but it does not do it aggressively. It is smart, as aggressive buybacks ought to be used when the shares are extremely undervalued.

Valuation

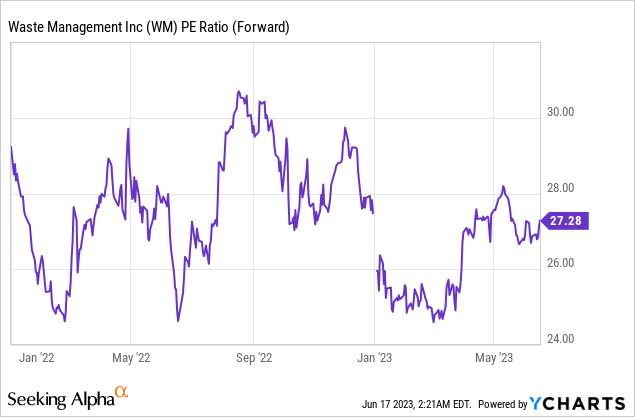

The corporate’s P/E (value to earnings) stands at 27 when contemplating the 2023 EPS forecast. Paying greater than 27 occasions earnings for an organization with an 11-12% progress charge appears excessive. Whereas the present valuation aligns with the common valuation over the past twelve months, it’s nonetheless exhausting to justify such a premium. This can be very exhausting to justify the premium when rates of interest are larger and risk-free curiosity is round 5%.

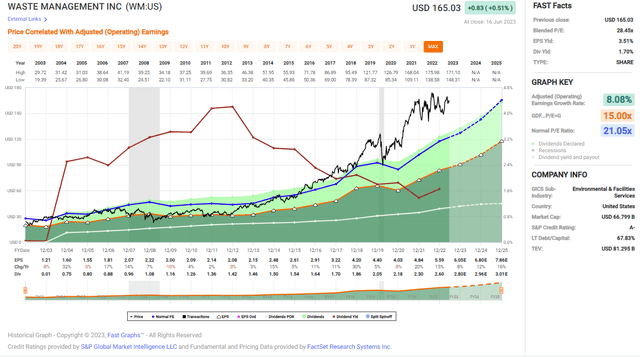

The graph under from Quick Graphs emphasizes how the corporate has traded for a premium since 2018. The common P/E ratio of the corporate over the past twenty years was 21. It’s nonetheless excessive, however not almost as excessive as the present P/E of 27. The corporate is forecasted to develop quicker than it did up to now twenty years, however I consider it’s nonetheless inadequate to justify the premium. The corporate is buying and selling for a valuation larger than tech firms like Alphabet and Meta.

Quick Graphs

Alternatives

The primary alternative for Waste Administration is that the corporate is absolutely built-in. It helps the corporate in two vital methods. First, the corporate can take pleasure in a greater value construction as every chain inside the worth chain helps the opposite chains. It has fewer bills and one headquarters to coordinate the actions. Furthermore, it makes the corporate stickier than a few of its friends, as it’s more durable to switch an built-in firm. Changing it means discovering one other absolutely built-in possibility or managing a number of firms to do the identical job.

Different two alternatives for Waste Administration revolve round sustainability and environmental development as extra states and municipalities present a rising curiosity in it. Concerning renewable power, Waste Administration is investing in renewable pure gasoline energy vegetation. It would make the most of pure gasoline created in its landfills and switch it into electrical energy that it could promote again to the grid. It implies that the corporate creates a brand new chain within the worth chain.

Recycling is the second alternative relating to the development. The corporate realizes that persons are making an attempt to cut back waste and change into extra environment friendly. Subsequently, Waste Administration is investing in enhancing its recycling exercise. The corporate invests cash in constructing new supplies restoration services, and it additionally invests in its automation. There are 43 deliberate new or automated services, and they’re anticipated so as to add 2.8M incremental tons of recycled managed.

Dangers

Competitors and regulation are two principal challenges that Waste Administration is coping with. On the subject of competitors, the world of recycling, renewable power, rubbish disposal, and many others, could be very aggressive. Whereas not all firms are built-in, they will nonetheless provide some degree of competitors versus Waste Administration. It is usually extremely regulated as most shoppers are cities, counties, and states. The corporate offers with hazardous supplies and is below scrutiny by regulators and politicians. A change within the regulatory atmosphere might improve prices and harm the EPS.

Inflation is one other threat for Waste Administration, particularly if it persists across the 4%-5% mark. Waste Administration’s enterprise requires vital investments in its workforce and equipment. Greater wages and better costs of uncooked supplies impression the corporate’s bills. Suppose we proceed to see substantial annual inflation. In that case, will probably be more durable for Waste Administration to keep up its 17% working margin, and we may even see it decline extra from the 18% it loved in 2019.

The shortage of margin of security is a long-term threat for the buyers within the firm. The corporate trades for a excessive valuation, that means any miss in its execution might ship the inventory down. When an organization is priced for perfection, buyers take a major execution threat. Good outcomes will not be sufficient to justify the valuation. If the corporate returns to its common valuation, will probably be down 23% from the present value.

Conclusions

To conclude, Waste Administration is a stable firm on observe to turning into a dividend aristocrat. The corporate has good fundamentals with the regular progress of its high and backside traces, which drive dividend progress and share rely discount. The corporate has what I consider are a number of nice progress alternatives and an built-in construction that each protects it from the competitors and helps it capitalize on new alternatives comparable to renewables and recycling.

Nevertheless, whereas the corporate has manageable dangers, comparable to competitors, inflation, and regulation, there may be some uncertainty relating to the margin of security. The present valuation leaves the corporate with no margin of security, and it should execute flawlessly. This will increase the extent of uncertainty to some extent the place I’m not snug, as even returning to common valuation will lead to vital capital depreciation. For this reason I consider that shares of Waste Administration are a HOLD.

.jpg)

:max_bytes(150000):strip_icc()/What-difference-between-standard-Error-means-and-standard-deviation_color-1c203133aca641aca0d03936d9558693.jpg)

/what-difference-between-magnum-cum-laude-and-summa-cum-laude_V2-3ae02babdc714ea9adaeec0f0a6bf1a5.png)

{kind=link}