Cineberg

Introduction

I’ve been following KBC Group (OTCPK:KBCSY) (OTCPK:KBCSF) for a number of years now as I preferred the financial institution’s robust capital ratios and beneficiant dividend coverage. This enables the Belgian financial institution to benefit from M&A alternatives to additional strengthen its place on the core markets (Belgium and the CEE), and again in 2017, the financial institution signed an settlement with the Nationwide Financial institution of Greece (NBG) to amass the fourth largest financial institution in Bulgaria. The overall worth of the transaction was simply 610M EUR (at 1.1 instances the tangible e book worth) which provides you a good suggestion of KBC’s deal measurement and its plan to slowly develop in its core markets with out jeopardizing the steadiness sheet on pursuing mega-deals.

Yahoo Finance

KBC Group has its main itemizing in Belgium the place the corporate is buying and selling with KBC as its ticker image. The Brussels itemizing has an common day by day quantity of 625,000 shares, making it essentially the most liquid itemizing and I might strongly advocate to make use of KBC’s Brussels itemizing to commerce. As KBC experiences in Euro and has its main itemizing in the identical foreign money, I’ll use the EUR as base foreign money all through this text except indicated in any other case.

Sturdy outcomes, regardless of the market turmoil

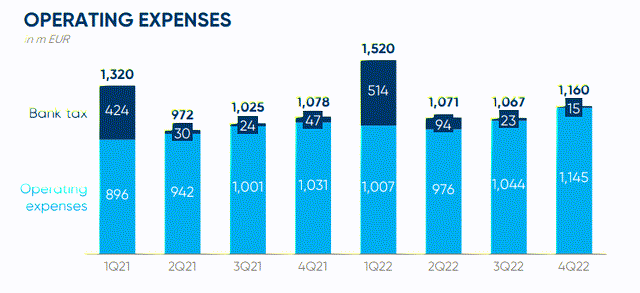

The financial institution’s first quarter was surprisingly robust. Historically, Q1 is the weakest because the financial institution is on the hook for the annual financial institution taxes within the jurisdictions it’s energetic in. Final yr, the entire quantity of financial institution tax was 514M EUR in Q1, and Q1 2023 wasn’t any completely different: the entire quantity of financial institution and insurance coverage taxes elevated to 571M EUR.

KBC Investor Relations

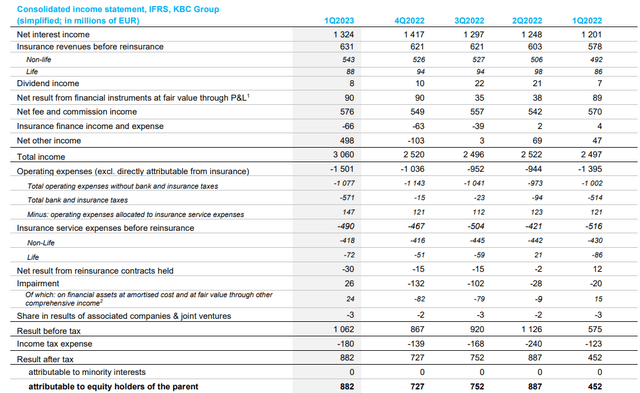

When you would (and will) count on the primary quarter’s backside line end result to be comparatively weak, KBC surprisingly posted a web revenue that was nearly twice as excessive as within the first quarter of final yr regardless of a decrease web curiosity revenue, as you possibly can see beneath.

KBC Investor Relations

The principle cause for the surprisingly robust result’s the 498M EUR in “web different revenue” and that is solely associated to the completion of the sale of the KBC Financial institution Eire. KBC confirmed the conventional run fee of the “web different revenue” is roughly 50M EUR per quarter, and it’s undoubtedly essential to know the overwhelming majority of that web different revenue is non-recurring in nature.

So whereas the web revenue was a really spectacular 882M EUR or 2.08 EUR per share, about 40% of the pre-tax revenue was generated from the sale of the Irish property so the normalized earnings had been barely decrease at simply over 1 EUR per share.

That’s nonetheless high-quality. Take into accout Q1 historically is the weakest quarter of the yr and if we glance again at FY 2022 whereby the financial institution reported a complete EPS of 6.75 EUR, just one.07 EUR was generated within the first quarter of the yr.

This implies there isn’t a want for the financial institution to alter its beneficiant dividend coverage. KBC continues to earmark a minimum of 50% of its consolidated web revenue for dividends KBC paid 4.00 EUR per share in dividends based mostly on its FY 2022 outcomes and because of the non-recurring acquire in Q1 of this yr, odds are KBC will hold the dividend a minimum of steady this yr.

The capital ratios stay robust, and this paves the best way for extra outsized dividends

One of many predominant the reason why I used to be drawn to KBC (apart from having publicity to Jap Europe) is the financial institution’s robust capital ratio. KBC has a number one CET1 capital ratio in Europe and needs to be nicely geared up to take care of the present volatility and nervosity on the monetary markets.

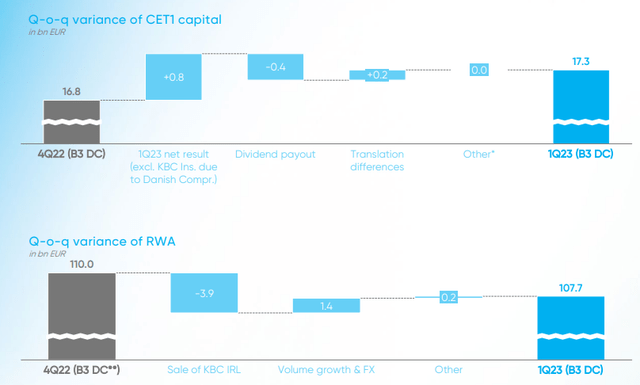

KBC was truly in a position to additional increase its capital ratios due to a robust earnings report. As you possibly can see beneath, the Q1 earnings added about 800M EUR of CET1 capital and greater than compensated for the 400M EUR provision for the dividend. As of the tip of Q1, the entire CET1 capital got here in at 17.3B EUR in comparison with “simply” 16.8B EUR as of the tip of the monetary yr 2022.

KBC Investor Relations

Moreover, the entire quantity of risk-weighted property decreased within the first quarter primarily because of the sale of the Irish property which had a constructive influence of three.9B EUR. This was partially mitigated by the 1.4B EUR associated to FX modifications and quantity development however on the finish of the quarter, the RWA decreased to 107.7B EUR. And that mixture of a better CET1 capital vs. a decrease quantity of risk-weighted property boosted the CET1 ratio to 16.1%.

This implies KBC already has absolutely digested the influence of a better required CET1 ratio. The annual assessment of the European Central Financial institution in December of final yr revealed an elevated CET1 requirement of 11.43% in comparison with 10.81% one yr in the past. However with a CET1 capital ratio of 16.1%, the financial institution is exceeding the minimal requirement with nearly 500 bp. Expressed in Euros, there’s about 5B EUR in “extra” capital on the steadiness sheet.

Funding thesis

I’ve an oblique lengthy place in KBC Group by a mono-holding (which is buying and selling at a double digit low cost to NAV) and though I must monitor the quarterly outcomes extra carefully whereas the monetary system is coping with the fallout of upper rates of interest, I see no cause to alter my bullish place. The financial institution and insurance coverage firm has discovered its lesson in the course of the world monetary disaster in 2008 when it needed to be bailed out and has now transformed itself to be one of the vital strong banks in Europe.

Editor’s Notice: This text discusses a number of securities that don’t commerce on a serious U.S. alternate. Please pay attention to the dangers related to these shares.

{kind=link}