JackF/iStock by way of Getty Pictures

Funding Thesis

Whereas there are some near-term headwinds because of the affect of rising rates of interest on the housing market, JELD-WEN Holding (NYSE:JELD) is executing effectively and was capable of develop income final quarter by means of value will increase in addition to market share features from struggling rivals in Europe. I imagine the corporate ought to emerge stronger on the opposite facet of this housing cycle because of its enhancing execution. Additional, JELD-WEN is anticipated to profit from long-term secular development developments, such because the rising variety of U.S. houses coming into the reworking age, the underbuilt U.S. houses market, and rising residence fairness. These components ought to additional contribute to the corporate’s income development within the new residential and R&R (Restore and Transform) enterprise over the approaching years.

When it comes to margins, the corporate is doing a very good job in phrases of cost-saving measures, concentrating on $100 million in financial savings from particular initiatives and ongoing operational efficiencies. This coupled with value will increase ought to greater than offset value inflation and lead to margin enlargement.

Presently, the corporate’s inventory is buying and selling at a ahead price-to-earnings (P/E) ratio of 12.99x, and I imagine it might see a optimistic re-rating as administration continues to implement productiveness and development initiatives. The corporate’s good development prospects and potential of re-rating of valuation a number of make it a very good purchase.

Income Evaluation and Outlook

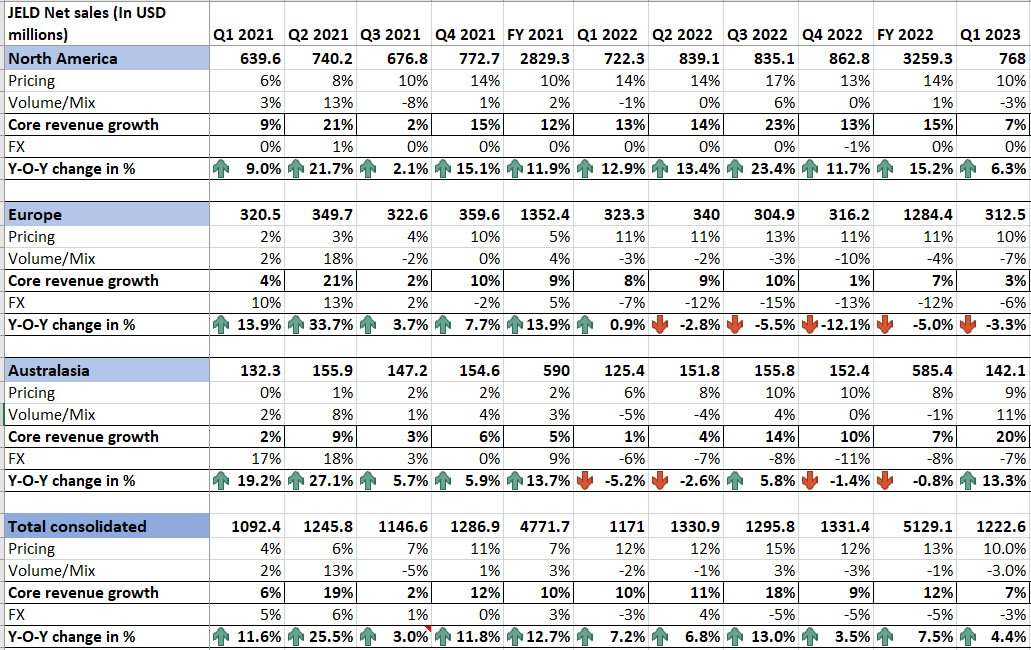

After seeing good development throughout the lockdown, the corporate has began feeling strain from rising charges and a few weakening in client spending attributable to excessive inflation. In Q1 2023, the Europe section of the corporate confronted headwinds from quantity decline and foreign money translation, primarily attributable to weak financial situations throughout many of the area. Consequently, the Europe section skilled a year-over-year decline of three.3% in income, amounting to $312.5 million.

Then again, the North American section noticed year-over-year income development of 6.3% to succeed in $768 million. This development was pushed by robust pricing throughout the quarter, which greater than offset the unfavorable affect of quantity decline within the section. Moreover, the Australasia section achieved a development of 13.3% in income, pushed by larger quantity and pricing. These robust ends in North America and Australasia helped offset the unfavorable affect from the Europe section, leading to an general income development of 4.4% to $1.22 billion within the first quarter of 2023.

JELD-WEN Historic Gross sales (Firm information, GS Analytics Analysis)

Trying forward, the corporate is more likely to face continued strain attributable to larger rates of interest and the present inflationary atmosphere. Nevertheless, the excellent news is that the developments within the housing market have been much less dangerous than feared. If we have a look at the most recent US housing begins information from Could, it surged to 1.63 million begins in Could which is a 13-month excessive and a significant enchancment versus April 2023’s 1.34 million begins. In Europe, whereas the housing business is seeing a slowdown, the corporate is capitalizing on the chance offered by macroeconomic challenges by capturing market share from struggling suppliers within the area.

Additional, it is price noting that the corporate has introduced the sale of the Australasia section to Platinum Fairness as a part of its enterprise simplification technique, and the primary quarter of 2023 would be the final quarter reporting section particulars inside the firm’s persevering with operations. The divestiture of this section ought to assist administration focus extra on its core U.S. and European markets which is a long-term optimistic.

Moreover, the corporate can profit from long-term secular tailwinds, reminiscent of traditionally underbuilt U.S. houses and an rising variety of houses coming into the prime reworking age, together with rising residence fairness. These components are favorable indicators for client spending on residential new development and R&R, respectively, additional supporting the corporate’s income in the long run.

General, whereas there are near-term headwinds, the corporate ought to emerge stronger on the opposite facet of the cycle as soon as the housing market stabilizes.

Margin Evaluation and Outlook

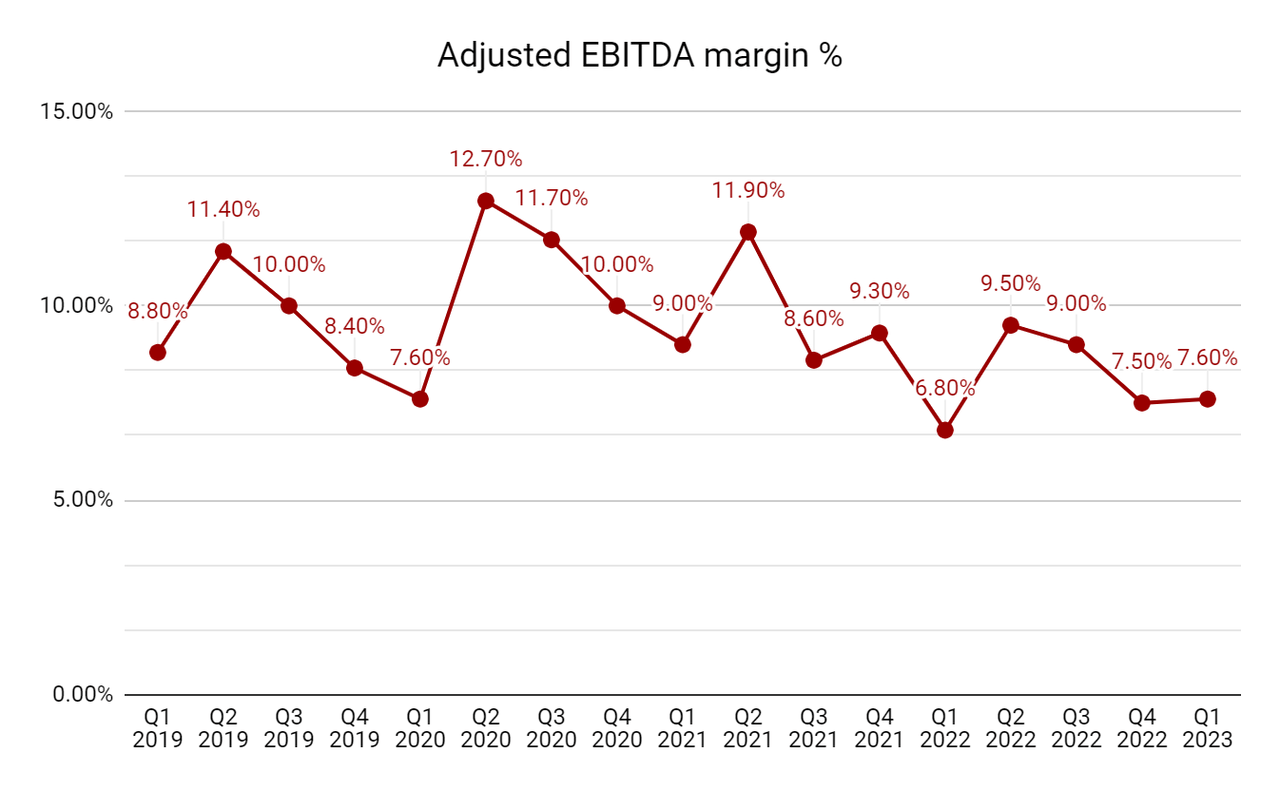

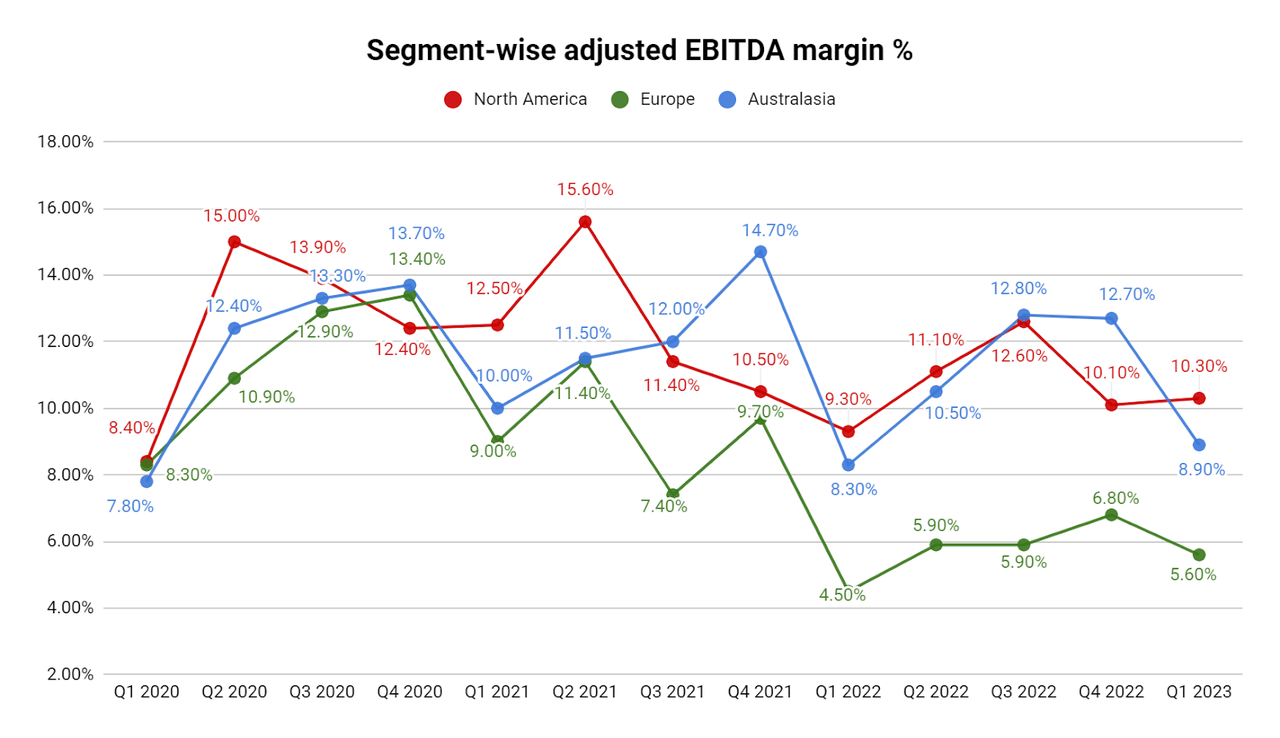

The corporate’s margins have been impacted by high-cost inflation in latest quarters. Nevertheless, administration has completed a very good job when it comes to rising pricing and enhancing productiveness which has helped the corporate greater than offset inflationary headwinds final quarter. The corporate’s adjusted EBITDA margin expanded by 80 foundation factors year-over-year to 7.6% within the first quarter of 2023, with all three segments experiencing optimistic margin development throughout the quarter. The North American section’s margin grew by 100 foundation factors year-over-year to 10.3%, primarily pushed by optimistic value/value realization.

Within the Europe section, productiveness features and optimistic pricing helped to offset the unfavorable affect of foreign money translation and quantity decline. Consequently, the section achieved a year-over-year margin enlargement of 110 foundation factors, reaching 5.6% for the primary quarter of 2023.

The Australasia section, alternatively, skilled a 60 foundation level year-over-year margin development, reaching 8.9% for the primary quarter of 2023.

JELD-WEN margins (Firm information, GS Analytics Analysis) JELD-WEN Section margins (Firm information, GS Analytics Analysis)

Trying forward, the corporate is actively engaged on simplifying its enterprise, enhancing its value construction, and implementing a change plan to cut back working prices and improve industrial excellence within the close to time period. Administration expects these efforts to drive value financial savings price $100 million in 2023. One instance of this initiative is the corporate’s centralized logistics program in North America to optimize its transportation community and enhance cargo visibility for its clients which ought to improve working effectivity and save $15mn in annual prices.

Moreover, the corporate can be engaged on rationalizing its community footprint. For the North American inside door enterprise, the corporate has strategically relocated manufacturing to websites nearer to clients, aiming to optimize manufacturing efficiencies and additional help long-term margins. Moreover, the closure of the Atlanta Doorways facility, which was introduced in January, is anticipated to ship roughly $11 million in annual value financial savings upon completion.

The corporate plans to make use of part of these financial savings to prioritize investments in initiatives with robust payback potential (eg. manufacturing unit automation) to additional enhance margins within the coming years. Along with these productiveness initiatives, the corporate also needs to profit from future value will increase and the carry-forward affect of value will increase from final yr.

Whereas the corporate’s margins face some headwinds within the close to time period attributable to quantity deleverage and price inflation, its value will increase and productiveness initiative ought to greater than offset it and lead to margin enlargement. I imagine the corporate remains to be within the early phases of implementing productiveness initiatives and for the following couple of years, I count on productiveness initiatives to proceed serving to margins.

Valuation and Conclusion

The corporate’s inventory is at the moment buying and selling at a P/E of 12.99x, based mostly on FY23 consensus EPS estimates of $1.36. Whereas it’s a slight premium versus its 5-year common ahead P/E of 12.77, it’s a significant low cost versus the sector median P/E of 17.14x. I imagine the inventory can see a optimistic re-rating of its valuation a number of because it continues to implement its productiveness initiatives and invests part of the cost-savings in automation and development initiatives. The corporate was capable of submit better-than-expected outcomes final quarter as these initiatives gained preliminary traction.

Additional, the corporate can be planning to make use of ~$450 mn of proceeds from the Australasia section divestiture to cut back its leverage (web debt to EBITDA) under 3x by the tip of this yr. This enchancment within the steadiness sheet also needs to assist the corporate spend money on long-term development and enhance its valuation a number of.

I imagine the housing market also needs to backside out within the present yr as rates of interest peak and we might even see a restoration over the following couple of years. So, for medium to long-term traders, the inventory can supply a very good upside. Therefore, I price it a purchase.

:max_bytes(150000):strip_icc()/What-difference-between-standard-Error-means-and-standard-deviation_color-1c203133aca641aca0d03936d9558693.jpg)

/what-difference-between-magnum-cum-laude-and-summa-cum-laude_V2-3ae02babdc714ea9adaeec0f0a6bf1a5.png)

{kind=link}