xtrekx/iStock by way of Getty Pictures

The CROX Funding Thesis Stays Wonderful, Regardless of The Rally Thus Far

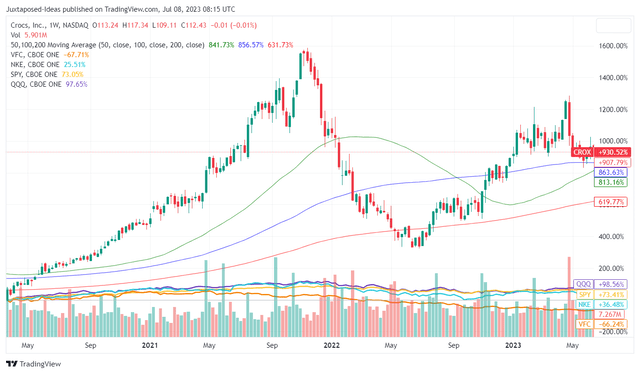

CROX 3Y Inventory Return

Buying and selling View

Crocs, Inc. (NASDAQ:CROX) has delivered excellent returns of +930.52% for the reason that worst of the pandemic, regardless of the drastic correction in 2022.

That is towards its client discretionary friends’ efficiency to this point, corresponding to Nike (NKE) at +36.48%/ V.F. Corp’s (VFC) at -66.24% and the broader market, such because the SPY at +73.41% and the QQQ at +98.56%.

Most significantly, all of those positive factors are attributed to its inventory returns, since CROX doesn’t pay a dividend. This cadence suggests two vital issues, in our opinion.

One, its long-term shareholders have continued to lend immense help to the inventory, sustaining its positive factors to this point. Secondly, the administration crew led by the CEO Andrew Rees, has additionally renewed its branding and refocused its choices since 2017, delivering glorious outcomes repeatedly, naturally explaining the primary level.

For instance, CROX has managed to develop its top-line to $884.17M by the most recent quarter, with the Crocs model delivering +22% YoY progress and HEYDUDE a +15% YoY progress.

With HEYDUDE producing an annualized income contribution of $941.6M (+104.8% YoY) and approximate gross revenue of $467.03M (+296.8% YoY) by the most recent quarter, based mostly on the step-up within the GAAP gross margin from 25.6% to 49.6%, it seems that the $2.5B price ticket will not be that hefty in spite of everything.

This proves that the extremely competent CROX administration has been in a position to fold the brand new acquisition into its present choices, whereas unlocking expanded margins.

Given these developments, buyers are in all probability not stunned by the raised FY2023 steerage, with revenues of $4B (+12.6% YoY) and EPS of $11.45 (+4.8% YoY) on the midpoint, particularly for the reason that administration expects HEYDUDE gross margins to enhance nearer to Crocs’ 55.8% within the close to time period.

As well as, because of the $589.85M of FCF generated during the last twelve months [LTM], we’re assured of CROX’s steerage of gross leverage of below 2x by the top of the yr and long-term goal of beneath 1x, with $600M of its long-term money owed already repaid over the LTM.

For now, its gross sales might have decelerated to +12.1% YoY within the North America market, because of the harder YoY comparability, elevated rate of interest atmosphere, and tightened discretionary spending.

Nonetheless, we imagine CROX’s outperformance internationally at +31.8% YoY within the newest quarter, particularly in China and Australia, might properly stability the momentary headwind, with Asia Pacific now comprising 21.5% (+3.7 factors QoQ/ +4 YoY) of Crocs revenues within the newest quarter.

Most significantly, demand in China seems to be accelerating, with the administration reporting a two-year progress price of +95% ex-currency within the newest earnings name, suggesting its lengthy runway for progress within the nation.

Because of these early promising outcomes, we imagine CROX’s H2’23 efficiency might exceed expectations, although FQ2’23 margins could also be briefly impacted by the seasonally increased SG&A and advertising spend. Buyers might wish to mood their expectations a bit.

So, Is CROX Inventory A Purchase, Promote, or Maintain?

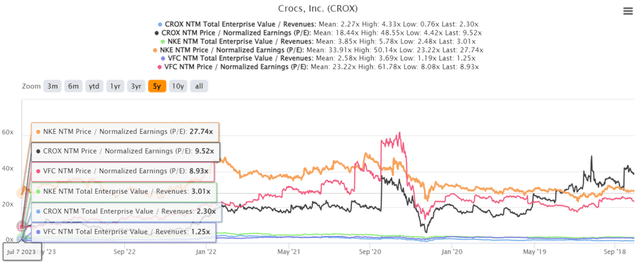

CROX 5Y EV/Income and P/E Valuations

S&P Capital IQ

For now, CROX’s valuations proceed to be moderated, with NTM EV/ Revenues of two.30x and NTM P/E of 9.52x, buying and selling beneath its 5Y imply of two.27x and 18.44x, respectively. The identical has been noticed with VFC’s valuations and, to a a lot smaller diploma, with NKE.

Maybe that is as a result of market analysts’ decelerating prime and backside line projection at a CAGR of +10.4% and +9.3% by means of FY2025, respectively, in comparison with its normalized ranges of +28.3% and +132.2% between FY2017 and FY2022.

Nonetheless, we imagine the pessimism embedded in CROX’s valuations are overly executed, for the reason that administration has been in a position to drastically develop its revenue margins by two-fold between FY2019 and FY2022.

Given its regular gross margins of 53.9% (+0.8 factors QoQ/ +4.7 YoY) within the newest quarter, we’re satisfied in regards to the administration’s pricing technique as properly, regardless of the rising stock stage of $476.11M (inline QoQ/ +16.8% YoY), in comparison with the FY2019 ranges of fifty.1% and $172.03M, respectively.

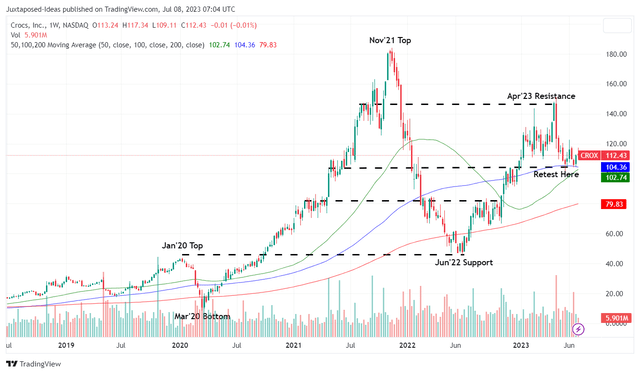

CROX 5Y Inventory Worth

Buying and selling View

With CROX remaining well-supported right here, we’re cautiously ranking the inventory as a Purchase. There’s a first rate margin of security to our value goal of $135.66 as properly, based mostly on its NTM P/E 9.52x and the market analysts’ FY2025 adj EPS projection of $14.25.

Lengthy-term shareholders can also wish to be affected person, since we imagine an upward rerating in its P/E valuations to the earlier normalized ranges of 17x is fully potential, nearer to its client discretionary friends, as soon as the macroeconomic outlook lifts and the Fed pivots.

This quantity suggests a long-term value goal of $242.25, implying an bold upside potential of +115% from present ranges. This correction is simply temporal.

:max_bytes(150000):strip_icc()/Primary-Image-usaa-cd-rates-april-2023-7483875-fbc5fe4c35f949c2bc5fb7d87b6ecd31.jpg)

{kind=link}