Richard Drury

With progress bulls within the driver’s seat and the Invesco QQQ ETF (QQQ) up a startling 43.6% YTD, it’s powerful to be optimistic about worth names which have misplaced their attract virtually utterly.

Extra particularly, whereas the market is seemingly pricing in additional certainty round international provide chains, inflation receding, rates of interest changing into much less of a difficulty as a consequence, extra flexibility for producers and fewer stress for shoppers, it has develop into a lot tougher to defend methods revolving round essentially sound however for some motive underpriced shares as they’re both delivering measly good points or are edging decrease within the worst case. Nonetheless, at the moment I’ll make an try to take action, with an up to date tackle the Alpha Architect U.S. Quantitative Worth ETF (BATS:QVAL).

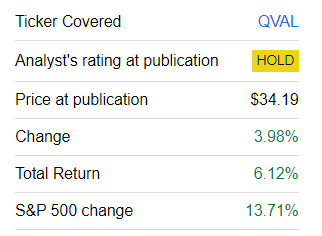

My earlier observe on QVAL was printed in December 2022, after I was much less optimistic about this worth/high quality combine and thus opted for a Maintain ranking. Since then, QVAL has solidly underperformed the S&P 500 index as a result of, as I stated above, bulls favored progress tales amid inspiring inflation information and the AI hype.

Looking for Alpha

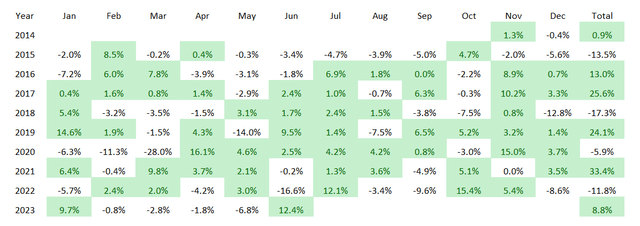

To deliver a bit extra shade, one thing atypical has occurred to QVAL this yr. The ETF noticed 4 crimson months in a row (February-Could), which has by no means occurred since its launch in 2014, with the exception being 2015, when it was declining persistently from Could to September. The earlier time it had three loss-making months in a row was in January – March 2020 amid the coronavirus market drama.

QVAL month-to-month and annual efficiency (Created utilizing information from Portfolio Visualizer)

Nonetheless, at this level, I’m extra assured about QVAL’s short-term prospects on account of two principal elements 1) elementary robustness of its portfolio, with spectacular progress/high quality/worth steadiness, and a couple of) potential cracks within the tech rally. Concerning the latter, with Netflix (NFLX) and Tesla (TSLA) quarterly earnings disappointing the market not too long ago, it’s cheap to mull over gaining some safety towards a possible broad correction in tech and quasi-tech darlings, and doing so with QVAL is sensible.

Looking for Alpha

However, there may be an outsized oil value threat on this combine (47% vitality sector publicity) that may in the end nullify its defensive impact; there are different threat issues as nicely. So I might suggest continuing with warning and punctiliously weighing the professionals and cons earlier than longing QVAL.

The Alpha Architect U.S. Quantitative Worth ETF modified its funding mandate a number of occasions previously, switching from an lively mannequin to a passive one after which to an lively once more. Since January 2022, it has not been monitoring any index. In line with the prospectus, at this level, its lively technique screens the universe of liquid U.S. shares utilizing the proprietary “worth entice” checks, being attentive to accruals amongst different parameters, measuring valuation utilizing the Complete Enterprise Worth/Earnings Earlier than Curiosity and Taxes ratio, additionally assessing “present profitability, stability, and up to date operational enhancements,” with a purpose to compose an equally-weighted portfolio of fifty to 100 positions. Among the many sectors, QVAL has little interest in financials, and for good motive because the TEV/EBIT ratio is of no use in the case of banks and the like. Nonetheless, different sectors is likely to be absent within the portfolio at occasions, e.g., the ETF presently has no publicity to utilities and actual property as nicely.

This technique appears to be like properly calibrated and probably able to creating sturdy worth inventory cohorts. However what’s in actuality contained in the portfolio?

Think about the next dichotomy first. There are fairness portfolios with the mid-single-digit earnings yields backed by the mid-to-high double-digit ahead EPS progress charges. They’re within the limelight when markets are ebullient, financial coverage is supportive or there may be a minimum of an expectation it could develop into supportive quickly sufficient, and traders are prepared to purchase into progress tales regardless of their costs. On the similar time, there are portfolios that provide a lot juicier yields, however ensuing from bleaker weighted-average progress charges, sometimes a lot decrease than 10%. They carry out strongly when the urge for food for progress is subdued. Actually, worth investing is just not monochrome, and reviewing a portfolio utilizing these two metrics is just not the one doable and clearly not the easiest way, but it’s easy and common sufficient to use throughout sectors. In fact, after we can add enterprise worth, EBITDA, money movement, and different parameters, we should always achieve this for a extra complete view and extra knowledgeable funding choices.

However what if a 21% earnings yield comes with an over 35% EPS ahead progress fee? That is QVAL’s phenomenon. And I imagine it’s value being attentive to it. Beneath is a comparability of the principal metrics as of July 20 and as of December 5.

Metric 20-Jul 5-Dec Market Cap $29.2 billion $18.87 billion EY 21% 20.2% EPS Fwd 35.2% 31.1% P/S 1.15 1 Income Fwd 9.2% 23.1% EBITDA/EV 21.4% 24% EV/S 1.33 1.14 ROTC 22% 23.9% Money Move Yield 25% 18.6% Click on to enlarge

Computed utilizing information from Looking for Alpha and the fund

Sector July December Supplies 5.7% 24.6% Info Expertise 2% 5.3% Industrials 16.6% 9.8% Well being Care 2.1% N/A Vitality 47% 37.4% Client Staples 3.7% 1.6% Client Discretionary 18.8% 20.5% Communication 3.9% N/A Click on to enlarge

Computed utilizing information from QVAL and iShares Russell 3000 ETF (IWV)

Even supposing about 67.5% of QVAL’s internet property are actually allotted to shares that have been absent within the December model, and in addition regardless of the sector publicity adjustments (healthcare and communication added and publicity to industrials and vitality elevated), the fund nonetheless has a phenomenally engaging valuation, sturdy high quality, and powerful progress metrics as nicely. Its weighted-average market cap has superior considerably, however the EY has even improved, now standing at about 21% (a P/E of 4.6x). I completely perceive that vitality (exploration & manufacturing, refining, and many others.) and supplies performs are the highest contributors, and earnings-based ratios are usually not your best option for them, thus this determine shouldn’t be reviewed in isolation.

Image Weight Sector Quant Valuation Grade Quant Profitability Grade EY PBF Vitality (PBF) 2% Vitality A A- 62% Alpha Metallurgical Sources (AMR) 1.8% Supplies A+ A+ 57% Peabody Vitality (BTU) 1.9% Vitality A- B+ 54% CNX Sources (CNX) 2% Vitality A- B 49% Scorpio Tankers (STNG) 1.8% Vitality C+ A+ 42% Click on to enlarge

Computed utilizing information from Looking for Alpha and the fund

Fortunately, there are not any financials within the basket, and EBITDA/EV can be utilized. And at round 21.4%, this earnings yield (adjusted for debt) tells an analogous story, particularly contemplating EBITDA is forecast to develop by round 16.1% portfolio-wise. The median progress fee appears to be like utterly ample at 9.5%, as per my calculations.

Subsequent, whereas EV/Gross sales is simply at 1.3x, the WA gross sales progress fee is above 9%. Some traders would possibly contemplate it too low, but I might say that this can be a fairly engaging degree assuming the income a number of. On a facet observe, the sharp decline within the fee is because of the elimination of Coterra Vitality (CTRA) and Devon Vitality (DVN) that have been the important thing contributors to it in December.

Subsequent, QVAL has ~22% ROTC, principally because of Alpha Metallurgical Sources (AMR), Cal-Maine Meals (CALM), and PBF Vitality (PBF). This can be a dependable indication of its top quality.

Remaining ideas

Progress bulls have seen a number of spectacular months because the model returned with a vengeance because of the inflation challenge slowly disappearing and AI boosting threat urge for food. But such a run would possibly finish abruptly, and it’s higher to be ready. QVAL’s appears to be like like an ETF to think about for that goal.

Its 50 stocks-strong portfolio has a single-digit P/E and single-digit EV/EBITDA, whereas each EPS and EBITDA progress charges are sturdy. There’s near nothing to criticize on the standard facet as solely Liberty Vitality (LBRT) has a C+ Quant Profitability ranking, whereas different holdings are B- rated or higher. The share of shares with a B- Valuation grade is near 56%.

Lastly, QVAL has a 39 bps expense ratio, which is pretty ample for an lively technique, whereas liquidity is total fantastic.

:max_bytes(150000):strip_icc()/What-difference-between-standard-Error-means-and-standard-deviation_color-1c203133aca641aca0d03936d9558693.jpg)

/what-difference-between-magnum-cum-laude-and-summa-cum-laude_V2-3ae02babdc714ea9adaeec0f0a6bf1a5.png)

{kind=link}