webphotographeer/E+ through Getty Pictures

Analysis Temporary

As we method one other week of earnings season, there’s one regional financial institution based mostly in my house state within the NYC space that’s price doing a pre-earnings analysis article on at present, as its subsequent earnings launch is true across the nook this Thursday Jul twenty seventh.

Valley Nationwide Bancorp (NASDAQ:VLY) is the mother or father firm of Valley Nationwide Financial institution, a identified model in northern New Jersey with firm roots going again to 1927.

Notable gadgets from its firm web site, company profile: $54B in belongings, branches in 6 states, trades on the Nasdaq (NDAQ), headquarters in New Jersey, market cap of $4.7B. Worthy to say is that institutional possession is 75%, among the many largest being BlackRock (BLK) and Vanguard, proudly owning 109MM shares between the 2 of them.

At the moment, we’re analyzing whether or not this regional financial institution is a value-buying alternative the place an investor can personal a bit of the financial institution’s present revenue stream and add it to their portfolio of financial institution shares for some “regional” diversification.

Scores Methodology

Our aim is to seek out undervalued shares of corporations with stable monetary fundamentals that pay aggressive dividend yields. Our key business focus is tech, financials, insurance coverage, and innovation.

To simplify my ranking of an fairness, I’ve damaged it down into whether or not I’d advocate or not advocate based mostly on these particular person components:

Valuation vs Sector Common. Dividend Yield vs Sector Common. Constructive YoY Web Earnings Development. Capital & Liquidity Energy Inventory Worth vs 200 Day SMA.

If I like to recommend on all 5 classes, it’s a “robust purchase”, 4 classes, is a “purchase”, 3 is a maintain, and fewer than that could be a promote ranking. Then I evaluate my ranking to the consensus rankings from Looking for Alpha & Wall Road.

Valuation vs Sector Common: Advocate

In our first class to debate, we wish to get proper into the valuation numbers. The 2 metrics used are the GAAP-based ahead price-to-earnings (P/E) ratio and the ahead price-to-book (P/B) ratio, then evaluating them each to the sector common. We’re on the lookout for valuations which might be near or decrease than the sector common by at the least 5 to 10%.

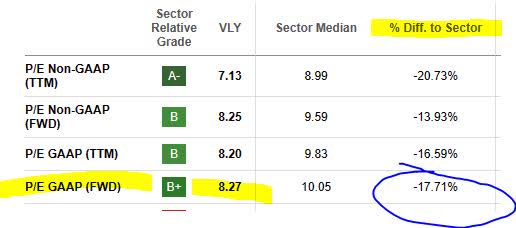

Based mostly on official valuation information taken from Looking for Alpha, we’re impressed by the ahead P/E of 8.27, which received a “B+” grade from Looking for Alpha and is near 18% under its sector common.

Valley Financial institution – P/E ratio on July 23 (Looking for Alpha)

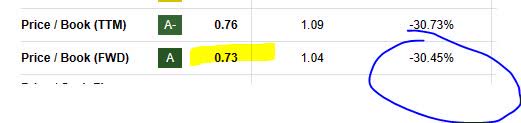

By way of the ahead P/B ratio, it’s at the moment 0.73, getting a grade of “A” from Looking for Alpha and is over 30% under the sector common.

Valley Financial institution – P/B ratio on July 23 (Looking for Alpha)

Normally, we choose a P/B under 1.0, and subsequently contemplate this inventory undervalued on each metrics, and would advocate on this class.

Dividend Yield vs Sector Common: Advocate

Our subsequent class to have a look at is the dividend yield and the way it compares to the sector common.

The close to 5% yield will get our consideration, at the moment at 4.68%, paying $0.11 a share on a quarterly foundation, based mostly on official dividend information.

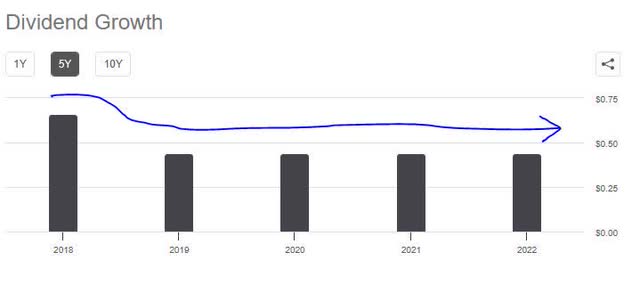

Considerably much less spectacular is 5-year dividend progress, which went from an annual dividend of $0.66 in 2018 to $0.44 the following yr, and remaining so by means of 2022, because the chart under exhibits.

Valley Financial institution – 5 yr dividend progress (Looking for Alpha)

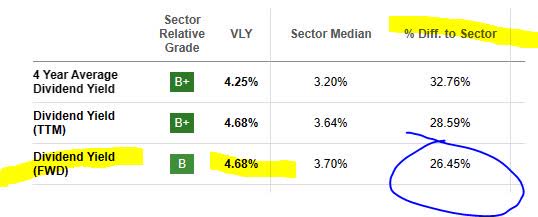

Nonetheless, the place it lacks in 5-year dividend progress it makes up for dividend yield vs the sector common. Contemplate the desk under, which exhibits that the present yield is definitely over 26% above the sector common:

Valley Financial institution – dividend yield vs sector common (Looking for Alpha)

This determine exceeds our goal of the dividend yield being at the least 5 to 10% above the sector common.

Based mostly on this proof, we advocate this inventory within the class of dividend yield compared to sector common.

Constructive YoY Web Earnings Development: Advocate

Subsequent, as we get into the matters of web revenue, capital & liquidity, as a reference we are going to use the corporate’s Q1 earnings presentation, out there from their investor relations web site.

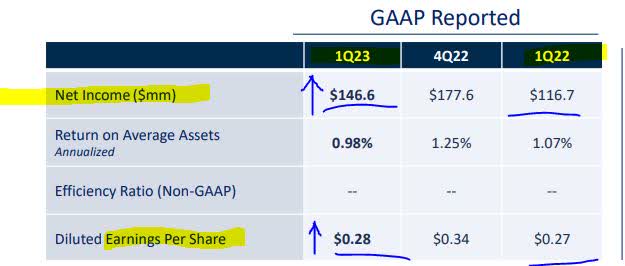

One optimistic to say from their Q1 outcomes, as proven under, is a $29.9MM YoY enhance in web revenue, in addition to a slight YoY enhance in diluted earnings per share:

Valley Financial institution – web revenue YoY (Valley Financial institution – Q1 presentation)

From a top-line view, it seems some key drivers are YoY progress in each web curiosity revenue in addition to non-interest revenue, which each confirmed YoY progress vs the identical quarter a yr in the past:

Valley Financial institution – web curiosity revenue (Valley financial institution – q1 presentation) valley financial institution – non curiosity revenue (Valley financial institution – q1 presentation)

That is additionally an instance of revenue diversification as properly, for my part. The explanation I do not merely take a look at income progress however web revenue is as a result of I wish to see an organization that manages bills effectively as properly, so these analysts who solely care in regards to the top-line will not be contemplating this.

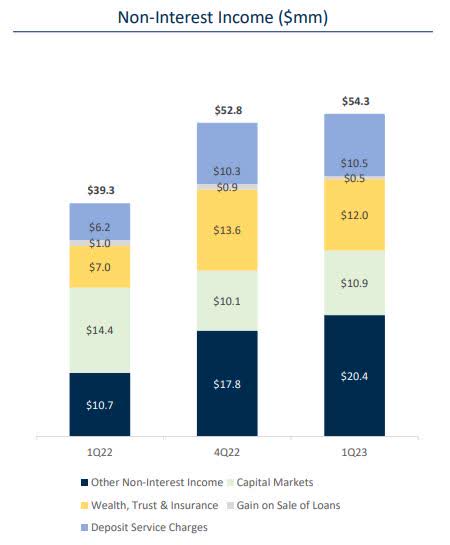

Though the core enterprise of a financial institution normally is dependent upon curiosity revenue, most banks I’ve reviewed even have a portfolio of different revenue streams. The next is an efficient instance of non-interest revenue has carried out for this financial institution YoY:

Valley financial institution – non-interest revenue progress by class (Valley financial institution – Q1 outcomes presentation)

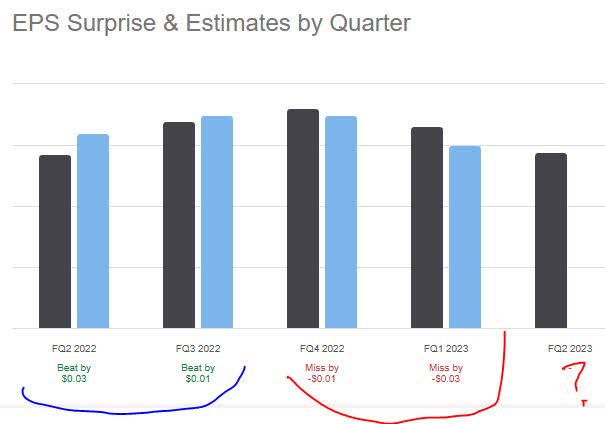

I believe that the optimistic revenue momentum will proceed wanting ahead in the direction of Q2 outcomes, with a 50% likelihood the financial institution beats barely on earnings estimates, based mostly on it having beat 2 of the final 4 estimates, as proven under:

Valley financial institution – earnings surprises (Looking for Alpha)

Based mostly on the proof discovered, I like to recommend this inventory on the premise of optimistic web revenue progress YoY.

Capital & Liquidity Energy of Firm: Advocate

On this class, we now have chosen to debate each capital & liquidity in the identical part regardless that they aren’t totally the identical factor, however each vital to the solvency & enterprise continuity of a financial institution.

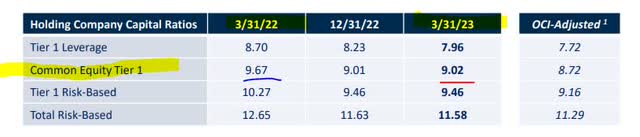

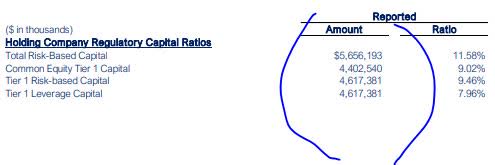

First, it’s notable to say that their CET1 ratio is properly above the well-known Basel III requirements, regardless that it’s barely decrease YoY:

Valley Financial institution – CET1 ratio (Valley Financial institution – Q1 presentation)

You will need to observe what benchmarks I’m evaluating this information to, and for that I reference the necessities {that a} monetary establishment have a complete risk-based capital ratio of 8% below Dodd-Frank guidelines, and tier 1 risk-based capital ratio of 4.5%.

On this case, this financial institution is properly in extra of the regulatory baseline required, and regardless of being a smaller regional financial institution, because the desk under exhibits, its whole risk-based capital exceeds $5.65B.

Valley financial institution – regulatory capital (Valley financial institution – q1 presentation)

Key liquidity notables to say:

The agency talked about of their Q1 commentary that they’ve “substantial extra liquidity out there from on- and off-balance sheet sources.”

As well as, they drove liquidity by means of further deposits, in addition to use of the FHLB:

Bolstered on-hand liquidity with totally FDIC-insured oblique buyer deposits sourced throughout substantial seller community. Utilized short-term FHLB advances to rapidly construct extra liquidity out of an abundance of warning. Extra liquidity continues to normalize as FHLB advances mature.

Wanting ahead to Q2 outcomes quickly, I count on related or higher outcomes as on this prior quarter, specifically want to see the CET1 enhance even higher. For the second, I like to recommend this inventory within the class of capital & liquidity power, proven by the proof.

Inventory Worth vs 200 Day SMA: Advocate

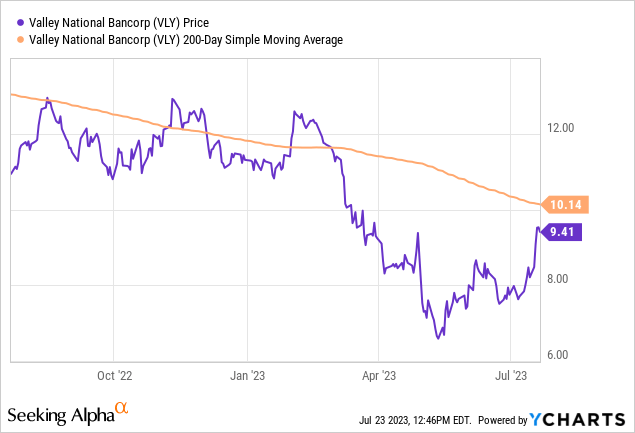

Going into the brand new buying and selling week, as of Sunday July twenty third the final share worth for this inventory closed at $9.41, as proven within the chart under:

Compared to the 200 day easy shifting common of $10.14, which we’re monitoring, the newest share worth is about 7.2% under the SMA.

Our personal portfolio technique & buying and selling thought we now have mentioned in current articles is buying and selling a “vary” that’s 5% above or under the 200 day SMA. That will put our buying and selling vary for this inventory at the moment between $9.63 and $10.65. Since this inventory is at the moment under that vary, we contemplate it a shopping for alternative for positive, and advocate it by way of share worth vs 200 day SMA.

To assist illustrate our investing thought, we now have created the next simulation spreadsheet, in order to “present” and never simply inform.

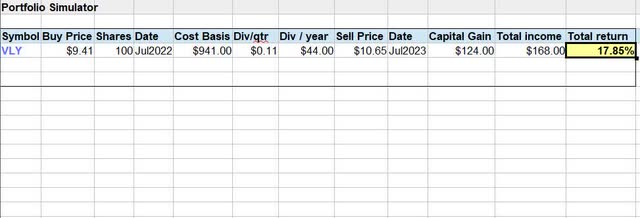

Portfolio Simulator (Albert Anthony & Co.)

As you may see in our investing thought above, we’re shopping for 100 shares at $9.41, the newest share worth as of the writing of this text and holding it for one yr to get the complete yr dividend revenue, then promoting at 5% above the present 200 day SMA. Our whole return on capital is projected to be 17.85%.

The chance to this investing thought, and monitoring the long-term shifting common, is that it could possibly additionally take a damaging flip after we purchase the shares and thereby inflicting unrealized losses (paper losses) to our portfolio.

We’re conscious that promoting coated name choices and incomes premiums from them is one approach to offset a few of that danger, as we now have performed so prior to now, nevertheless we is not going to get into the complexities of choices buying and selling on this article, for brevity’s sake.

Nonetheless, we predict monitoring the 200 day long-term common is much less dangerous than making an attempt to “time” the short-term averages, and our present investing thought rests on that notion. Your constructive suggestions within the feedback is actually welcome!

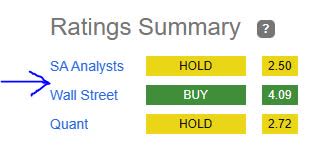

Scores Rating: Robust Purchase

At the moment this inventory received all 5 of my ranking classes and is getting a robust purchase ranking. That is barely extra bullish than the Wall Road consensus of a purchase ranking, as proven under, and rather more bullish than the consensus from SA analysts and the SA quant system which gave it a maintain ranking:

Scores Consensus (Looking for Alpha)

Dangers to my Outlook:

A danger that would influence my overly bullish outlook on this inventory is the financial institution’s publicity to business actual property, significantly workplace properties, in addition to any damaging developments going through their mortgage guide resembling web charge-offs and non-performing loans. This might scare away some buyers from this inventory.

So, I made a decision to see what the corporate itself needed to say about this of their Q1 presentation, to get some thought of what the Q2 figures could appear like.

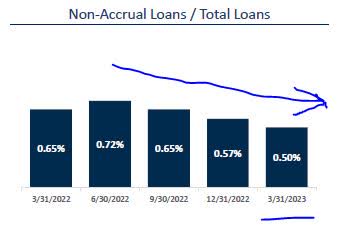

First off, a notable optimistic is that the share of non-accrual loans to whole loans has declined going into the tip of Q1, as proven within the chart under, bringing the quantity down to only 0.50% of whole loans:

Valley financial institution – non-accrual loans (Valley Financial institution – q1 presentation)

I venture that this downward pattern will proceed going into the Q2 outcomes, predicting non-accrual loans to be someplace within the vary of 0.40% – 0.50% of whole loans.

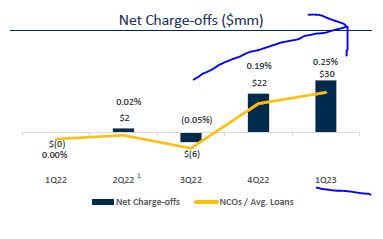

Barely extra regarding, as proven under, is the uptick of web charge-offs, nevertheless on the finish of Q1 they’re nonetheless simply 0.25% of avg. loans:

Valley Financial institution – web chargeoffs (Valley financial institution – Q1 presentation)

I count on for Q2 outcomes this quantity to stay related, within the vary of 0.20% – 0.30%.

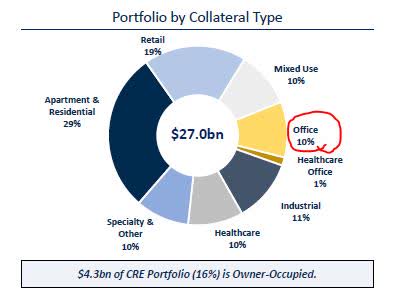

Now the enjoyable half, the query you’re all ready for.. what’s their publicity to workplace properties on the finish of Q1?

Because it seems, simply 10% of their CRE portfolio!

Valley financial institution – CRE portfolio (Valley financial institution – Q1 presentation)

The vast majority of their portfolio is tied to residences/residential, so with workplace making up lower than 1 / 4 of the pie I’d contemplate it a minor danger publicity. On the identical time, nobody property class makes up over half the portfolio.

I venture these numbers to be related within the Q2 figures and wouldn’t be stunned if the financial institution decides to restrict additional workplace publicity going ahead, with a aim of bringing it below 10% of the portfolio. Definitely I want to hear administration commentary in Q2 concerning the efficiency of the workplace portfolio.

All in all, this proof ought to present a counterweight to buyers involved about my bullish sentiment on this inventory.

Evaluation Wrap Up

To wrap up at present’s evaluation, listed here are key factors we mentioned.

I’m giving this inventory a robust purchase ranking at present, because it received in 5 of my ranking classes. This ranking is extra bullish than each the Wall Road & Looking for Alpha consensus.

Positives: Dividend yield vs sector common, inventory worth vs 200 day SMA, P/E and P/B valuation vs sector common, optimistic web revenue progress, liquidity & capital power of firm.

A danger that would dampen my bullish outlook on this financial institution is their publicity to dangerous loans, web charge-offs, and business actual property, particularly workplace property, and this danger has been addressed.

In closing, I proceed to search for hidden dividend gems among the many regional banks, and for my part this has been one among them. I’m including it to my watchlist and would contemplate together with it as a small proportion of a bigger financial institution inventory portfolio, to offer regional & dividend yield diversification.

{kind=link}