Vladimirs_Gorelovs

Thesis

My article analyzes Danone S.A.’s (OTCQX:DANOY) Q2 2023 Earnings Report, noting the corporate’s spectacular gross sales development and ongoing enhancements of their transformation plan. Nonetheless, I additionally make clear potential danger elements and headwinds resembling unfavourable quantity combine impacts from adversarial international trade charges in addition to challenges with Russia that finally concludes with a “maintain” score for the inventory.

Firm Overview

Danone S.A., an illustrious multinational company, boasts a various portfolio of products, which extends from dairy merchandise like yogurts, cheeses, and milk-based objects, to drinks, plant-based choices, ice lotions, and frozen confections. The corporate can also be acclaimed for its sturdy vary of dietary merchandise particularly crafted for moms, infants, and younger youngsters. Moreover, it dispenses specialised healthcare vitamin objects and an assortment of water manufacturers which are enriched with the pure essence of fruits, fruit juices, and nutritional vitamins. The distribution of their merchandise spans numerous channels, resembling stores, comfort shops, medical institutions, and digital commerce platforms. Having been established in 1899, the corporate’s central headquarters is located in Paris, France.

Danone S.A. Q2 2023 Earnings Highlights

Danone S.A. revealed a commendable Q2 efficiency, recording a like-for-like web gross sales development of 6.4% – a testomony to the power of all its geographical sectors. This parallels the gross sales of Q1, signifying the agency’s constant stride in its broad-based enlargement.

The corporate’s Chinese language market proved sturdy, and the European transformation technique displayed significant progress. The Important Dairy Merchandise [EDP] class was instrumental to the Q2 development, because it manifested a web gross sales improve of 6.2%, because of thriving Excessive Protein, On a regular basis Vitamin, and Espresso Creation platforms. The Specialised Vitamin class retained a aggressive development charge of 4.9%, registering market share advances in areas resembling China and Southeast Asia. The Waters class, pushed by the stellar performances of Evian in Europe and Mizone in China, recorded a wholesome improve of 9.6%.

The 6.4% like-for-like web gross sales improve in Q2 included a worth impact of 8.7% and a quantity combine contraction of two.3%. Pricing took a downward flip relative to earlier quarters, whereas quantity efficiency displayed an uptick within the semester’s preliminary volumes. Nonetheless, foreign money trade charges had a unfavourable impression of 4.3% attributable to depreciation of some currencies towards the euro. In totality, the quarter’s reported development stood at 2.4%, with web gross sales amounting to EUR 7.2 billion, a slight rise from EUR 7.1 billion in Q2 of the previous 12 months.

Every geographical area made vital contributions. Europe registered 6.5% development, with nations like France, Poland, and Spain performing as the expansion engines. North America yielded 5% gross sales development in Q2, predominantly propelled by the Espresso Creations unit. The zone encompassing China, North Asia, and Oceania logged a 9.6% gross sales improve, majorly powered by quantity combine. Latin America posted Q2 gross sales development of 10.8% with all nations within the area contributing to this efficiency. Lastly, the remainder of the world area recorded a 3.9% gross sales development within the second quarter.

Danone S.A.’s recurring working margin for H1 was famous at 12.2%, marking a betterment from final 12 months. The agency has voiced confidence in its capacity to satisfy its full-year steerage for modest margin enhancements. The recurring EPS for H1 2023 stood at EUR 1.76, a 7.6% rise relative to the previous 12 months. The free money circulate for H1 2023 touched EUR 1.1 billion, displaying an roughly EUR 400 million improve from the prior 12 months, a consequence of prudent capital allocation and dealing capital administration.

All in all, Danone S.A.’s management tasks optimism concerning the the rest of 2023 and plans to implement its “worth creation mannequin” primarily based on its first semester efficiency. And regardless of latest evolutions in Russia (elaborated under beneath “Dangers & Headwinds”), the corporate stays steadfast in its forward-looking enterprise technique.

Efficiency

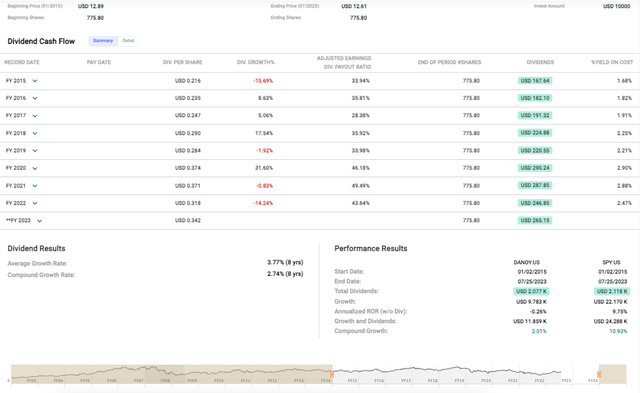

Danone’s efficiency over the previous eight and a half years has been, frankly, lackluster. The evident statistic right here is the corporate’s annualized charge of return (ROR) with out dividends at a dismal -0.26% – and this, throughout a time when the general market, as benchmarked by the S&P Index, has been a good-looking 9.75% return.

Quick Graphs

Regardless of this, I wish to spotlight what some traders would possibly see as a silver lining – the dividends. The full dividends amassed over this medium-term interval stands at USD 2.077K on a hypothetical $10k funding, making Danone a alternative (not essentially an interesting one) for dividend-focused traders.

Valuation

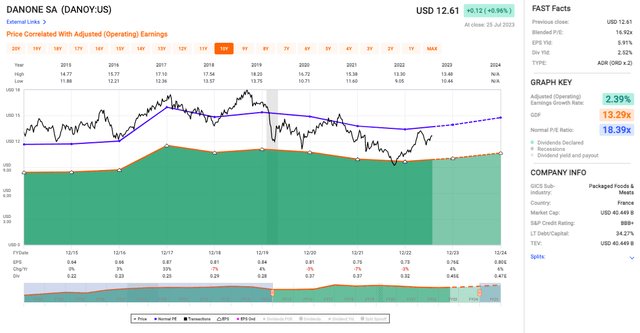

Danone’s development charge stands at a relatively modest 2.39%, which is not precisely the quantity I might be leaping up and down over. We’ve got a blended P/E of 16.92x and a traditional P/E ratio of 18.39x (see chart under) which signifies that Danone is presently buying and selling at a barely decrease a number of than its historic norm. This might point out that the inventory is undervalued, offering traders with a sexy entry level; or it may sign decrease future development expectations. And for these with an urge for food for income-generating investments, a dividend yield of two.52% and EPS yield of 5.91% would possibly pique your curiosity

Quick Graphs

Dangers & Headwinds

A conspicuous unfavourable quantity mixture of -2.3% was reported in Q2, marking a departure from the optimum trajectory. As quantity combine is an amalgamation of each demand and competitors elements, this downturn may probably signify a diminished shopper attraction or an intensification of competitors within the market. You may take this small downturn calmly or view it as presumably signaling an early warning of eroding market share and probably a dwindling topline.

One other noteworthy knowledge level is the subdued worth impact reported for Q2 – 8.7%, a discount from 10% in Q1. The deceleration, albeit minor, of this metric might trace in direction of a waning pricing energy. This probably undermines the corporate’s capacity to take care of or improve its costs, which is an important side in offsetting value will increase and safeguarding revenue margins.

Moreover, let’s not neglect Europe’s recurring working margin. This metric receded by 232 foundation factors in comparison with the earlier 12 months, dropping to 10.6%. As of now, this minor improvement means that even with reported development, the profitability panorama on this important market is retreating. With Europe being a considerable phase of the corporate’s operations, steady slippage in profitability right here may spell hassle for the agency within the near-term.

Lastly, the precarious state of affairs in Russia provides one other layer of complexity to the agency’s predicament. The choice to deconsolidate its Important Dairy and Plant-Primarily based [EDP] enterprise will result in a money impairment of round EUR 0.2 billion and a foreign money translation distinction of roughly EUR 0.5 billion. CEO Antoine de Saint-Affrique addressed the difficulty in his opening convention name remarks by noting

Given the sensitivity of the state of affairs, I hope you’ll perceive there’s not a lot we are able to say at this stage aside from the truth that we stay centered on individuals’s security and on continuity of operations.

Sadly, for now, that does not give traders a lot to go on.

Last Takeaway

Primarily based on the supplied particulars, I’d charge Danone S.A. as a “maintain.” The corporate is displaying sturdy gross sales development in all its geographical segments, and the progress of their transformation plan is promising. Nonetheless, the lackluster annualized return charge and a number of other danger elements such because the unfavourable quantity combine, adversarial international trade impacts, and ongoing points in Russia are regarding. These may considerably impression the corporate’s profitability and future development, necessitating a cautious strategy.

Editor’s Word: This text discusses a number of securities that don’t commerce on a serious U.S. trade. Please pay attention to the dangers related to these shares.

/what-difference-between-magnum-cum-laude-and-summa-cum-laude_V2-3ae02babdc714ea9adaeec0f0a6bf1a5.png)

{kind=link}