tadamichi

Written by Nick Ackerman.

For some background, right here is my view on dividend development shares:

Dividend development shares aren’t all the time probably the most thrilling investments on the market. They usually aren’t grabbing the headlines, and so they aren’t the shares operating up lots of of percentages in a yr. The truth is, they’re usually among the least thrilling shares. And that’s exactly their strongest promoting level. With such an enormous world of dividend development shares accessible on the market, it is very important display by way of to see if there are any worthwhile investments to discover.

They’re shares that present rising wealth over time to earnings traders. Dividend growers are sometimes bigger (not all the time), extra financially secure corporations that may pay out dependable money flows to traders. Some are slower growers than others. Some are going to be cyclical that require a robust financial system. Some are going to be secular, which does not typically depend on a extra strong financial system.

Dividend development can promote share worth appreciation. In fact, that’s if these corporations are rising their earnings to assist such dividend development within the first place. Belief me. There are yield traps on the market – I’ve owned a number of that I am not notably happy with.

I like to think about investing in dividend shares as a perpetual mortgage of types. Primarily, each dividend is a reimbursement of your authentic capital. Ultimately, holding lengthy sufficient, you’ve gotten the place “paid off.” It’s all returned again into your pocket from that time ahead.

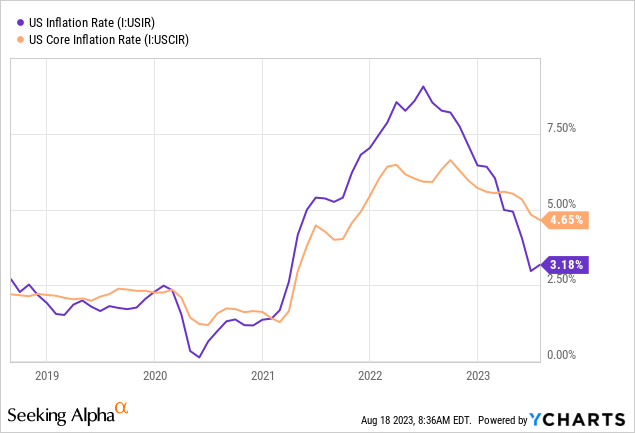

The Fed gave one other 25 foundation level hike with a view to proceed to tame inflation bringing charges to the very best stage in 22 years. Inflation continues its downward pattern. Most predict this to be one of many final hikes, with doubtlessly yet one more later this yr, nevertheless it all is dependent upon the information because it is available in. The most recent CPI report exhibits a slight uptick from final month.

The Fed themselves undertaking for rates of interest to be lower subsequent yr and in 2025 from present ranges. Once more, it is dependent upon how knowledge is available in and what types of occasions occur throughout this time.

All of this being mentioned, it is very important perceive my strategy to dividend shares and why screening dividend shares might be essential for earnings traders. These are August’s 5 dividend development shares that is perhaps worthwhile for a deeper exploration. As with all preliminary screening, that is simply an preliminary dive – extra due diligence could be mandatory earlier than pulling the set off.

The Parameters For Screening

I will be utilizing some useful options that Looking for Alpha offers proper right here on their web site for this display. Specifically, I might be screening using their quant grades in dividend security, dividend development and dividend consistency.

Dividend Security is comparatively self-explanatory. These might be shares that SA quants present cheap security in comparison with the remainder of their numerous sectors. The grade considers many various components, however earnings payout ratios, debt and free money move are amongst these. This class might be shares with A+ to B- rankings.

For the dividend development class, we’ve got components such because the CAGR of assorted durations relative to different shares in the identical sector. Moreover, the quants additionally have a look at earnings, income and EBITDA development. As we are going to see, this does not imply that each inventory with a better grade has the expansion we’re searching for. This simply components in that the dividend has grown or earnings are rising to assist dividend development presumably. For these, the grades will even be A+ by way of B- grades.

Lastly, for dividend consistency, we wish shares that might be paying dependable dividends for us for a really very long time. Specifically, hopefully, they’re elevating yearly, although that is not an express requirement. We will even embody shares with a basic uptrend in dividend funds, which implies there may have been durations the place they paused will increase for a yr or two.

After taking a look at these components alone, we’re left with 527 shares right now from the 525 listed final month. I am going to hyperlink the display right here, although it’s a dynamic listing that continually updates repeatedly. When viewing this text, there may very well be kind of when going to the hyperlink.

From there, I wished to slim down the listing much more. I then sorted the listing by ahead dividend yield, from highest to lowest. Since these might be safer dividend shares within the first place, screening for these among the many greater payers should not damage.

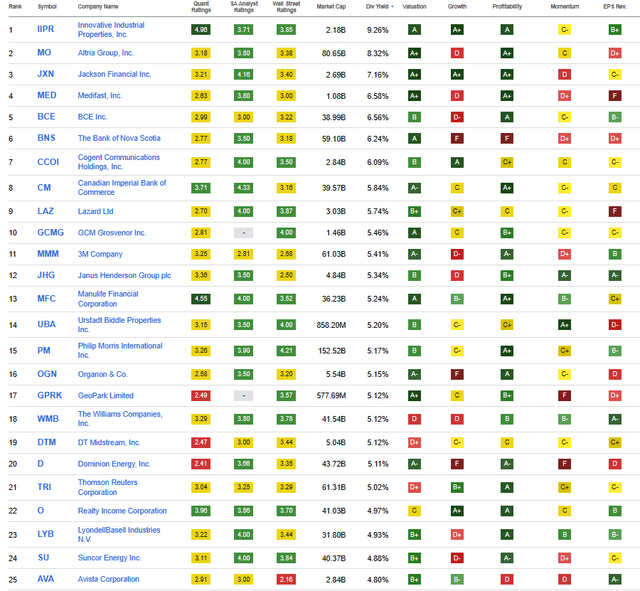

I’ll share the highest 25 that confirmed up as of 08/02/2023.

Prime 25 Screening (Looking for Alpha)

As standard, we are going to skip over the names on the high of the listing that we not too long ago coated within the prior couple of months. That features Progressive Industrial Properties (IIPR), BCE (BCE), The Financial institution of Nova Scotia (BNS) and Cogent Communications Holdings (CCOI).

That leaves us with giving Altria (MO), Jackson Monetary (JXN), Medifast (MED), Canadian Imperial Financial institution of Commerce (CM) and Lazard (LAZ) a search for this month. JXN is a brand new identify, however the remaining we’re revisiting.

Altria 8.32% Yield

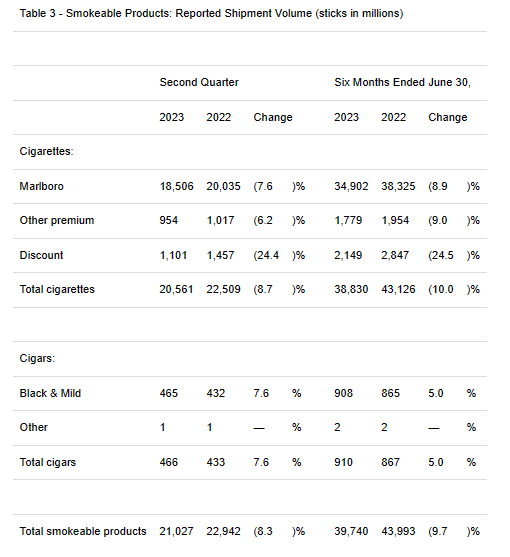

As standard, MO wants little or no introduction. This can be a favourite of earnings traders. This sin inventory not too long ago posted its outcomes, and it was largely in keeping with analysts’ expectations. Whereas they’ve made a number of missteps over time in making an attempt to exchange the shrinking cigarette delivery volumes, they’re on a brand new quest after buying NJOY. Cigar shipments have grown, however their bread and butter Marlboro model continues to see shrinking volumes yr after yr.

MO Cigarette Quantity (Altria)

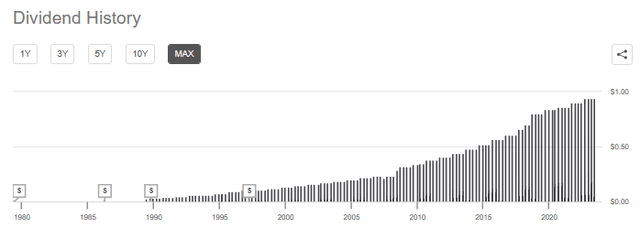

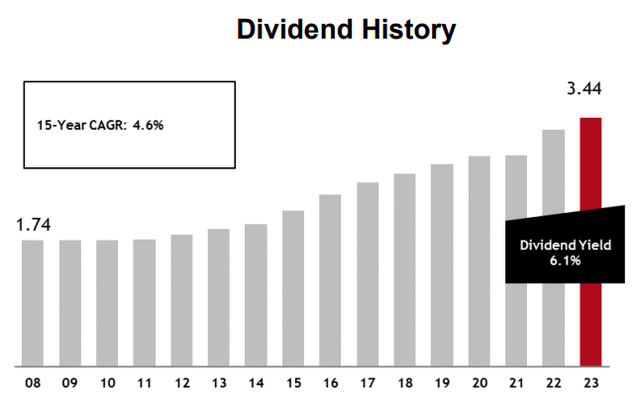

Regardless of that, income grew year-over-year at round 1.3%. Actually, nothing to brag about, however contemplating your core enterprise confirmed a ten% decline in cargo quantity for whole cigarettes, it actually exhibits the pricing energy they’ve. In fact, the true declare to fame for MO right here is the rising dividend which has been rising for 53 years, in accordance with Looking for Alpha.

The tempo of development lately could have slowed down on the again of slower earnings development, however they’re broadly anticipated to maintain on elevating the dividend. If historical past repeats, the elevate must be introduced someday later this month.

MO Dividend Historical past (Looking for Alpha)

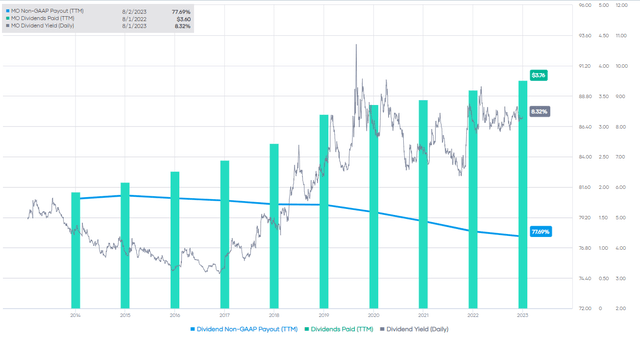

That is backed by a well-covered dividend with a payout ratio of round 77% based mostly on ahead estimates. That is actually excessive, however solely actually the place it has been for the final decade. The truth is, during the last decade, it will seem that the payout ratio has really come down throughout this time barely. Moreover development within the dividend, the precise yield itself is a monster on the inventory’s present share worth.

MO Dividend Historical past and Earnings (Portfolio Perception)

Jackson Monetary 7.16% Yield

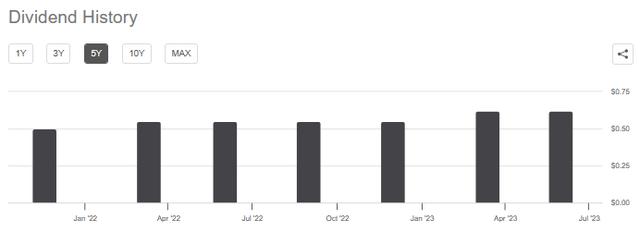

This can be a new identify to the listing and one I debated including. That is just because the historical past is not that lengthy, however they seem dedicated to rising their dividend nonetheless. Initially, the corporate paid a $0.50 quarterly payout that was raised to $0.55; then, the final enhance bumped it as much as $0.62. So pretty wholesome will increase as properly.

JXN Dividend Historical past (Looking for Alpha)

JXN was spun off from Prudential (PRU); this was accomplished in late 2021, thus, is why the corporate would have a brief historical past. Nevertheless, operations return to its founding in 1961.

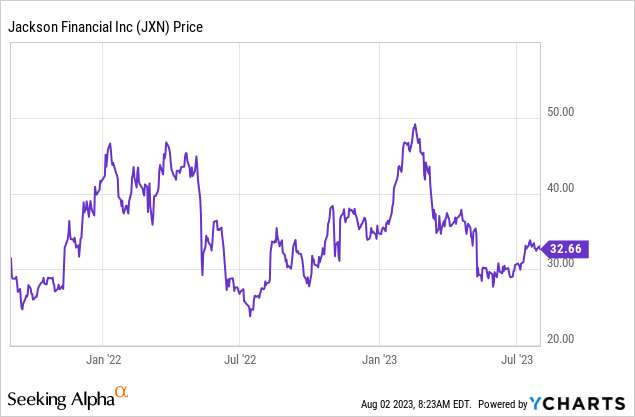

Moreover rising its dividend to push the yield up, the corporate has seen a struggling share worth during the last a number of years, with a very deep drop extra not too long ago.

YCharts

One of many causes for being underneath strain may very well be the expectation for earnings to drop fairly considerably this yr earlier than growing once more over the following a number of years. In fact, that is solely estimates of the will increase, and it’ll rely upon what occurs within the general financial system going ahead.

JXN Earnings Estimates (Looking for Alpha)

Annuity gross sales hit a brand new report in 2022, and that confirmed bode properly for JXN, particularly because the record-high gross sales continued within the first quarter of 2023 as properly. The dividend is well coated with a payout ratio of 17.4% based mostly on ahead EPS estimates, even contemplating the dip in earnings which are anticipated earlier than anticipating development returning. This could result in a vibrant dividend development future for JXN, and it makes it most positively an attention-grabbing identify to think about.

Medifast 6.6% Yield

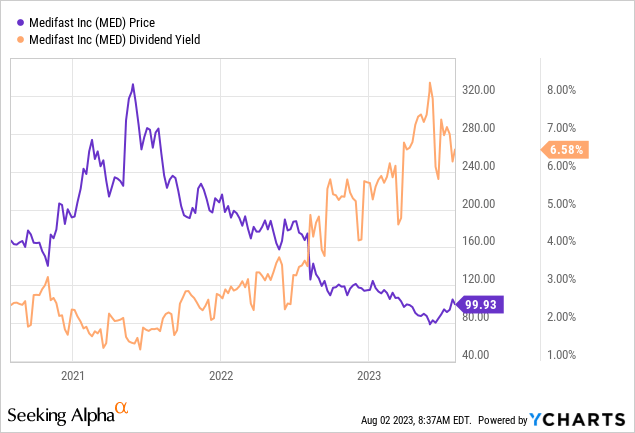

This can be a identify we have come throughout a number of occasions, the final being in Could 2023. The yield right here is primarily the results of the inventory plunging over 43% within the final yr. This was a pandemic darling that is seeing its fortunes reverse as so most of the Covid performs are going through related fates.

YCharts

Earnings have been booming throughout this time as well being grew to become entrance and middle when folks have been at dwelling with nothing higher to do. The corporate focuses on “weight reduction, weight administration, wholesome dwelling merchandise, and different consumable well being and dietary merchandise” across the globe. Nevertheless, customers appear to have reversed these wholesome habits again to pre-pandemic ranges.

MED Earnings (Portfolio Perception)

The corporate did reward shareholders fairly impressively whereas earnings have been booming. And it have to be mentioned that they’re making an attempt to carry onto their dividend streak by elevating 0.6% with their final elevate.

MED Dividend Historical past (Looking for Alpha)

Nevertheless, the strain of earnings coming down so dramatically pushes the payout ratio to 83%. That leaves them with some room, however as an organization that wishes to develop, that additionally limits money that would go to their development. That is solely round a $1 billion market cap firm, however they do have massive ambitions for development.

General, we’re focusing on 200 to 300 foundation factors of sustainable gross margin financial savings by 2025, enabling us to make the most of these financial savings to gas the actions we’re taking to develop within the years forward We consider that funding our development this fashion can assist mitigate detrimental impacts on our margins and can enable us to make future progress in the direction of our 15×25 targets.

I would like to speak somewhat bit extra in regards to the development initiatives that we’re at the moment enterprise. We now have already established share management within the weight reduction market, however with greater than 2,200 million folks in america alone taking a look at weight administration as a part of their broader effort to attain their well being and wellness targets, it is clear that we’ve got solely simply scratched the floor of what’s attainable.

Whereas our enterprise development rhythm has been disrupted, our core enterprise stays sturdy, and we proceed to be extremely assured in our coaches’ capacity to develop their attain and engagement with our present choices. On the similar time, our mannequin provides us the flexibility to discover different revenue-generating alternatives as we proceed to nurture that core enterprise.

“15×25” is a reference to returning to fifteen% annualized income development and 15% working margins by 2025.

Their Q2 outcomes got here in at $2.77, which smashed the anticipated $1.32 to $1.44 vary they guided for in Q1. That is actually some vibrant information, however for Q3, they’re guiding for EPS of $0.71 to $1.32.

That is one firm that I would nonetheless look to keep away from except you’ve gotten a robust opinion that they will return to development as soon as once more if customers proceed a more healthy way of life.

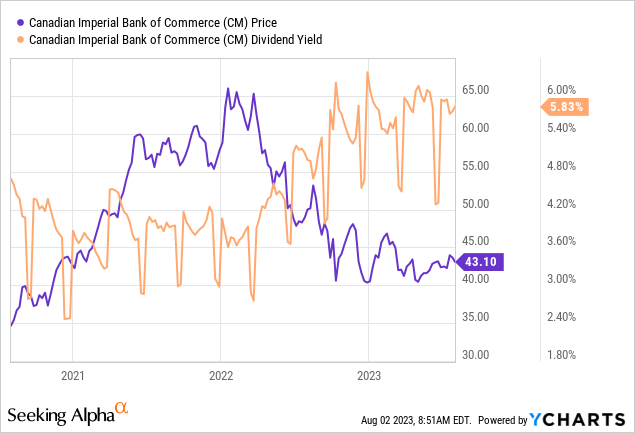

Canadian Imperial Financial institution of Commerce 5.84% Yield

The final and first time that CM confirmed up on our month-to-month screening article was again in February 2023. This happened as their share worth has come underneath strain – which is just about a key theme on what number of of those names make their approach onto this screening piece. That is sort of the purpose, although, discovering greater yielders which have proven pretty constant dividend development at a less expensive valuation on what may very well be non permanent dips.

YCharts

CM is one among Canada’s “massive 5” banks, so clearly, it performs an essential position in Canada. In fact, not solely are they essential in Canada however essential world wide with their international operations regardless of not being Canada’s largest financial institution.

An essential financial institution means it must be provided some protections when it comes to authorities assist when issues get shaky. That does not all the time imply losses might be averted for traders, nevertheless it ought to imply some added scrutiny from regulators that preserve a better eye on these entities.

The dividend will get paid in CAD and is transformed to USD, so in wanting on the dividend historical past, it may look a bit uncommon when wanting on the USD quantities.

CM Dividend Historical past CAD to USD (Looking for Alpha)

As a substitute, taking a look at their newest truth sheet exhibits us a greater illustration of the dividends paid yearly.

CM Dividend Historical past (Canadian Imperial Financial institution of Commerce)

The dividend historical past is enticing, and it may very well be a comparatively enticing financial institution based mostly on valuation. Nevertheless, its earnings development has been fairly minimal or nonexistent. Revenues have been slowly shifting greater over time however are largely anticipated to flatline going ahead within the subsequent couple of years. Earnings are anticipated to be underneath strain, and so they have not essentially been probably the most constant earners within the final a number of years, both.

CM Earnings (Portfolio Perception)

In fact, that was having to take care of the pandemic as properly, and monetary establishments are naturally delicate to financial circumstances anyway. With all that being mentioned, it is actually an attention-grabbing identify to think about going ahead, however it will be nice to see earnings begin trending greater.

Lazard 5.74% Yield

LAZ final appeared for us in April 2023, so comparatively not too long ago. This identify additionally popped up on a few events final yr too. LAZ is a monetary firm that focuses on monetary advisory and asset administration. By way of asset managers, it is a small firm with a market cap of round $3 billion and an AUM of round $240 billion. The final reported AUM exhibits a rise from the prior month, which is encouraging. This can be a partnership that points a Ok-1 tax type.

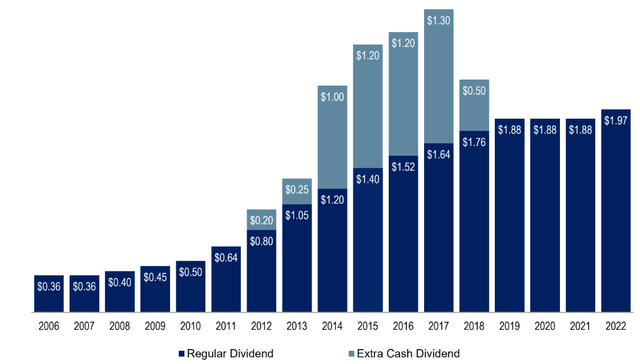

The corporate has been in a position to ship a pattern of strong dividend development and, when occasions have been good, fairly sizeable particular dividends as properly.

LAZ Annual Dividend Historical past (Lazard)

They do not all the time elevate yearly consecutively; for example, the final dividend quantity has now been for 5 quarters in a row. The $0.47 earlier than that was held regular for 13 quarters straight, which incorporates the pandemic interval. This is not essentially a foul factor both, as the corporate pays extra when it may well after which conserves money in additional robust financial occasions.

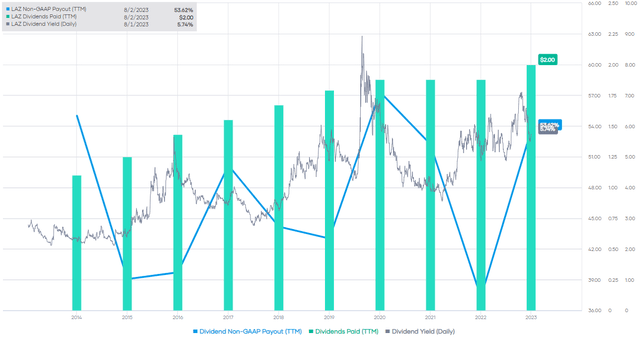

The non-GAAP dividend payout ratio has been effective within the prior years.

LAZ Dividends and Earnings (Portfolio Perception)

Nevertheless, earnings within the final quarter confirmed non-GAAP EPS of $0.24, about half of what the corporate is at the moment paying quarterly. On a GAAP foundation, it was a internet lack of $1.41 per share. The distinction right here was associated to cost-saving initiatives:

Second-quarter and first-half 2023 adjusted results1 exclude pre-tax prices of $146.7 million and $167.4 million, respectively, referring to bills related to cost-saving initiatives; first-half pre-tax prices of $10.7 million referring to bills related to senior administration transition, a profit pursuant to tax receivable settlement obligation (“TRA”) of $40.4 million, and $19.1 million referring to sure asset impairment prices. On a U.S. GAAP foundation, these resulted in a internet cost of $146.7 million, or $1.65, per share, diluted, for the second quarter, and a internet cost of $145.9 million, or $1.66, per share, diluted, for the primary half of 2023.

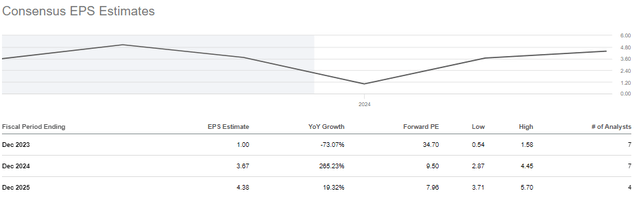

Based mostly on ahead estimated earnings, it does not look nice, as analysts anticipated $1 in earnings for fiscal 2023 earlier than recovering considerably.

LAZ Earnings Estimates (Looking for Alpha)

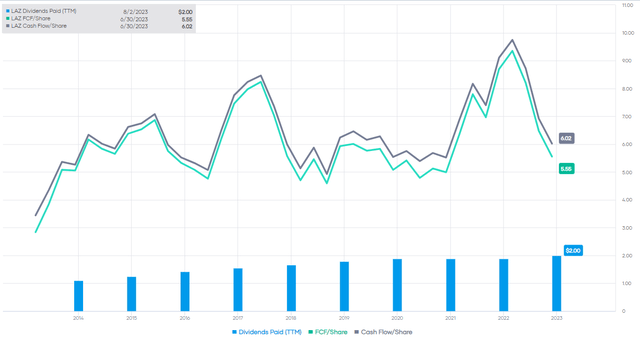

That mentioned, money move and FCF have seemed higher than their EPS.

LAX Dividends and Money Flows (Portfolio Perception)

The corporate seems to be to be in a troublesome state of affairs however is one other instance of an organization reliant on the general financial and market circumstances. The corporate’s CEO sees the M&A market stabilizing, “and circumstances are set for the start of a rebound.” Ought to that happen, it is seemingly that LAZ can start to get well its earnings and money flows and begin placing these again in the precise course as soon as once more.

Editor’s Observe: This text discusses a number of securities that don’t commerce on a serious U.S. change. Please pay attention to the dangers related to these shares.

{kind=link}