It is a dividend horror movie for shareholders. xijian/iStock by way of Getty Photographs

Medical Properties Belief (NYSE:MPW) did precisely what it ought to do. MPW chopped off an enormous portion of their dividend cost. Let the anger begin!

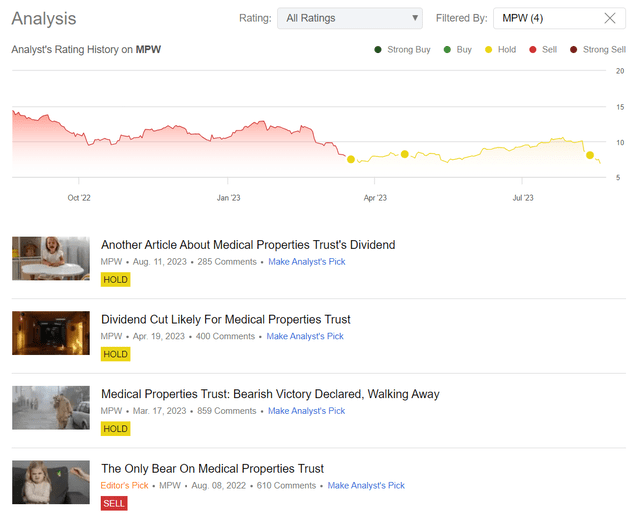

If You Solely Learn Looking for Alpha for Medical Properties Belief

Hello readers, for individuals who solely use Looking for Alpha to examine MPW, chances are you’ll not bear in mind me. I used to be the one bear on Looking for Alpha for a very long time. These are my prior articles:

Looking for Alpha

You could be forgiven for pondering that Looking for Alpha is an internet site dedicated to Medical Properties Belief. There have been usually 1 to five articles about Medical Properties Belief within the trending part. That is a bearish signal to me, by the way in which. When there’s that a lot curiosity, readers are looking for affirmation. Simply my view. No stats to again that one up.

Why did I’m going impartial? The upside from buyout threat was offsetting the draw back from unhealthy choices. That made it onerous to name a course, and I do not prefer to make predictions about coin flips.

Why Did Medical Properties Belief Minimize The Dividend?

Money movement.

Finish of article?

You most likely need extra element.

Promoting Off Belongings

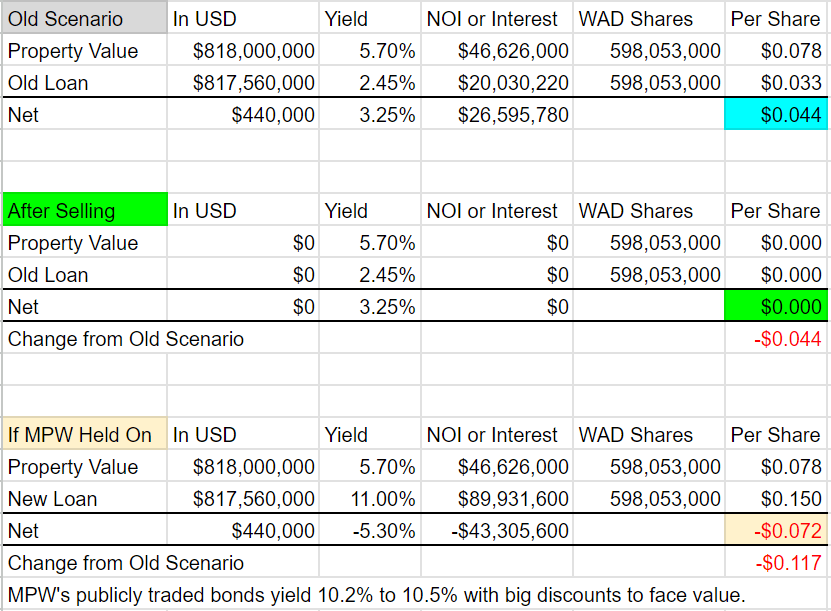

As you recognize, MPW has been promoting some belongings. That was a great transfer. Nevertheless, it was going to be dilutive to AFFO. Considerably dilutive. Not precisely. Math is required.

They used to finance properties with actually low-cost debt. As an example, perhaps a mortgage at 2.45%. Just about any actual property could be accretive to AFFO in case you can finance it at 2.45%.

Nevertheless, as rates of interest went up and credit score spreads for MPW elevated, the price of new debt was going to rise dramatically. MPW might maintain on to the belongings and search new financing at larger charges, or they might promote the belongings.

I ready the next desk beforehand to reveal their choices relating to a previous property:

Creator’s calculations and projections

As a result of MPW’s publicly-traded bonds supplied worth upside and massive yields, I made up my mind an 11% yield was an applicable estimate for brand spanking new financing.

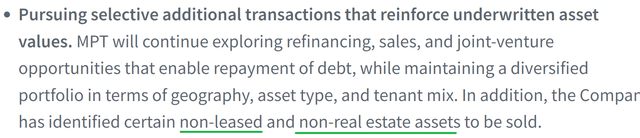

Sadly for shareholders, actual property is not the very best belongings to dump. There are different belongings that contribute much less to AFFO.

MPW has recognized another belongings that should be offered.

Ready by The REIT Discussion board

MPW does personal just a few jets. Some may really feel that administration can buy their very own jets for private use. As an example, I am “some” within the prior sentence.

MPW Debt Discount

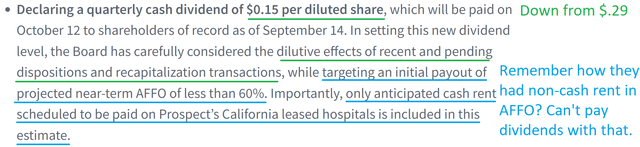

In decreasing the dividend, MPW issued an affordable press launch. They targeted on latest and pending transactions, seemed for a low payout ratio, and targeted on “AFFO” that was not together with non-cash hire:

MPW

Medical Properties Belief Plans to Cut back Working Bills

Medical Properties Belief is also taking intention at working bills:

MPW

Working bills are one other nice space to search for reductions. Hopefully, it isn’t simply property working bills. They could as properly have a look at all working bills to search out areas for discount.

Dividend Corrected

The absurd dividend has been dealt with. They made the massive reduce reasonably than setting themselves as much as want a number of cuts. That was a good selection.

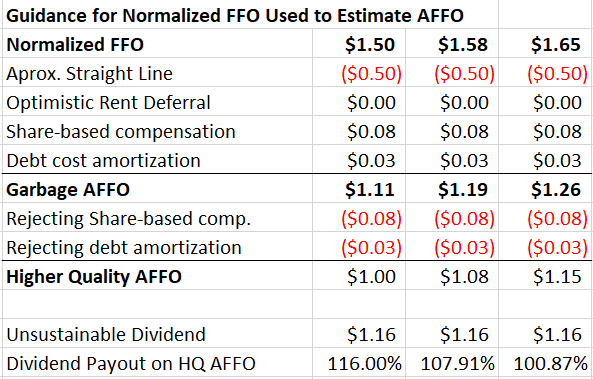

After I was protecting the excessive dividend payout ratio, I supplied the next desk:

Creator’s calculations and projections

For a little bit context, the metric I used as “Rubbish AFFO” is what MPW refers to as “AFFO.”

I eradicated different changes I felt should not be current, and the evaluation demonstrated that dividends have been too excessive. Regardless of having math within the article, one thing most individuals despise, it generated greater than 800 feedback. Some have been from individuals who claimed to be accounting consultants however demonstrated minimal understanding of accounting. In different phrases, it was about what you anticipate within the feedback.

Clearly, an annualized dividend charge of $.60 per share appears far more cheap on this state of affairs.

Conclusion

The dividend discount for MPW is an effective factor. It might considerably enhance their price of capital. They will pay down their money owed and strengthen the corporate. For all MPW’s flaws, they nonetheless have a fabric amount of money movement. It wasn’t sufficient to maintain paying out that dividend, but it surely must be sufficient to maintain them going.

Whereas some buyers blamed the bears, they have been proper to imagine the dividend would should be diminished. If the dividend was not diminished, MPW’s price of capital would hold going up. They wanted a approach to pay down these money owed. This was an essential step in the appropriate course.

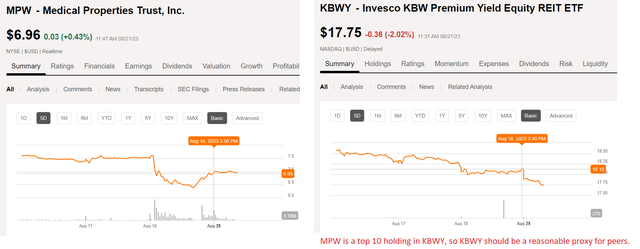

You’ll be able to even see that the market is ok with this transfer. MPW is definitely doing significantly better than different highly-leveraged REITs with large dividend yields and weak or unfavorable AFFO per share development:

Looking for Alpha

The opposite potential “shoe to drop” could be MPW being faraway from some high-dividend indexes. Nevertheless, MPW nonetheless has a really excessive dividend yield. It is nonetheless about 8.6%. So I would not anticipate this reduce to have a giant unfavorable influence on their place in indexes.

With the dividend reduce already introduced, two main bear catalysts fade away:

The dividend reduce (clearly). The potential for MPW to get hammered by larger charges on debt as a result of they have been bleeding out a lot cash by the dividend.

Greater charges can nonetheless damage MPW, however the potential influence is diminished. Bear in mind rates of interest have been going up for MPW in two methods:

Greater Treasury charges. Wider credit score spreads on their money owed.

Decreasing debt can enhance the scenario in two methods:

Cut back the excellent principal. Encourage thinner credit score spreads on money owed.

Outlook

My view continues to be impartial. Looking for Alpha exhibits “impartial” as “maintain.” There is no choice to market an article as “impartial”. In finance phrases, both score signifies the analyst is selecting to finish a score or to not assign a bullish or bearish outlook. In my view, the chance/reward at this time is best than it was at any prior level.

That is not sufficient to really tip me into the bullish camp, but it surely strikes me additional away from the bearish camp. If I needed to come down as both a bull or a bear, I might most likely land with the bulls now that MPW is below $7.00 AND slashed the dividend by practically 50%. Nevertheless, I am not pressured to enter both camp.

Our fairness REITs have dramatically decrease elementary dangers. They use much less debt relative to your entire capital construction and dividends are simply coated by AFFO. I search clever opposition to my thesis as a result of typically I will discover a good argument that may change my view. It is a decrease volatility technique, but it surely has carried out fairly properly for us through the years.

I discover most well-liked shares and child bonds are helpful instruments to reinforce the yield on the portfolio. It offers us a lower-risk approach to improve the yield whereas choosing REITs based mostly on anticipated complete returned (dividend + worth change). There was no want for buyers to know for the MPW yield. That is how greedy for yield usually ends: A a lot decrease share worth and a dividend discount.

Bear in mind, MPW was greater than $24.00 lower than two years in the past. Avoiding these traps is a vital a part of success.

Thanks for studying.

:max_bytes(150000):strip_icc()/150513-F-ZZ999-906-5b6cd53146e0fb0025ec090c.JPG)

:max_bytes(150000):strip_icc()/What-difference-between-standard-Error-means-and-standard-deviation_color-1c203133aca641aca0d03936d9558693.jpg)

/what-difference-between-magnum-cum-laude-and-summa-cum-laude_V2-3ae02babdc714ea9adaeec0f0a6bf1a5.png)

/HabitsThatWillHelpYouPayOffDebtMay202021-51f5539c69cf4a7ba82f9f7059c10f5c.jpg)

{kind=link}