Michael Kovac/Getty Photos Leisure

Gary Friedman: A Controversial Determine

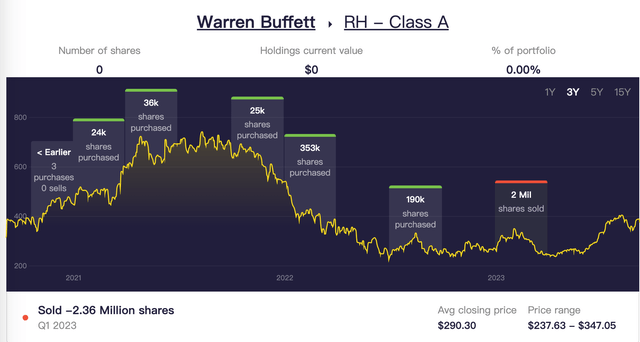

Now we have adopted RH (NYSE:RH) for a number of years now. For these enthusiastic about RH, you will need to observe Gary Friedman, the corporate’s CEO and Chairman. Friedman is a controversial determine. He had a robust resume, having beforehand served manufacturers like Williams-Sonoma (WSM) and Pottery Barn, earlier than becoming a member of RH. His daring and aggressive type saved RH from the brink of breakdown in 2016. Friedman is a powerful believer in branding, as evidenced by his dedication to constructing RH into one of many world’s premier furnishings manufacturers. His ambition to make RH an excellent model on the extent of Apple or LVMH has been acknowledged repeatedly in shareholder letters over time. He additionally appreciated to tout having Warren Buffett as a shareholder, although Buffett is not any longer invested in RH after COVID.

Stockcircle

RH’s Evolution

Whether or not you want his character or not, Friedman’s transparency in disclosing his views and pursuits appears extremely aligned with shareholders in our opinion. Now we have adopted him since 2016 when he purchased a big stake in RH throughout a difficult interval when the corporate confronted competitors from e-commerce gamers like Wayfair and omni-channel retailers like West Elm. RH was barely worthwhile on the time, however Friedman firmly believed brick-and-mortar was the way forward for furnishings. Right here is the quote:

We consider, “There are these with style and no scale, and people with scale and no style,” and the thought of scaling style is giant and far-reaching.

In consequence, he began constructing RH’s signature large-format shops mixed with eating areas.

RH

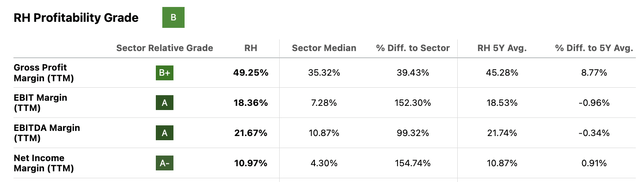

We tended to agree on the time, and his technique appears to have labored, with RH rising from a 5% working margin in 2016 to twenty% in 2022.

RH has additionally confirmed resilient throughout COVID-19, when the US economic system was practically shut down. Whereas the furnishings {industry} benefited considerably from work-from-home tendencies, RH’s lack of on-line presence and distribution initially fearful buyers. Surprisingly, the corporate maintained 7.6% income development and 28% working earnings development in 2020 by way of catalog gross sales and designer visits. It additionally maintained industry-leading margins. This demonstrated the ability of its enterprise mannequin.

Searching for Alpha

Gary’s Early Warning

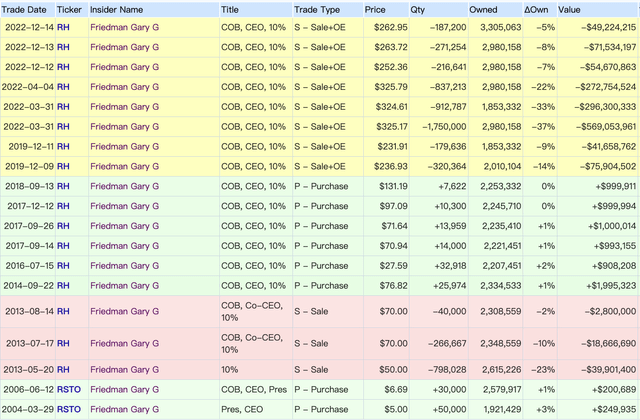

Gary additionally signaled early that RH can be impacted when the Ukraine battle began in March 2022, as he noticed client demand slowing. Although RH’s financials nonetheless appeared resilient, Gary disclosed he was promoting shares and suggested buyers to not purchase if the CEO was promoting. We view his insider buying and selling historical past gives a helpful indicator for RH buyers in shopping for and promoting.

Nevertheless, we now have not seen Gary buy any shares but since his final sale in 2022, although RH has began shopping for again shares, one other significant indicator to look at.

Openinsider

RH’s Share Buyback Historical past

RH’s share buyback coverage could be very aggressive. In 2017, to show administration’s confidence in RH’s future, the corporate spent $1 billion in money to purchase again shares, retiring virtually 50% of shares excellent and leaving simply $18 million in money at fiscal year-end. The inventory rose from as little as $26 to $160 per share in a single 12 months. This displays Gary’s type over RH’s historical past over the previous decade. So it is an encouraging signal that RH began shopping for again shares once more in 2022, spending $1 billion to retire 17% of shares excellent.

Searching for Alpha Searching for Alpha

General, RH is a shareholder-friendly firm, although Gary’s aggressive method carries dangers.

Latest Earnings and Market Challenges

RH reported Q2 earnings as we speak and its inventory was down 7% after hours. RH’s Q2 2023 outcomes confirmed a 20% income lower, much like Q1, with full-year steerage implying a 15% decline suggesting additional enchancment in 2H 2023. Nevertheless, working earnings dropped 36% with important deleverage. The buybacks helped solely modestly, as diluted EPS nonetheless fell 26%.

Gary expects the luxurious housing market and the broader economic system to stay difficult by way of fiscal 2023 amid excessive mortgage charges. This aligns with tendencies in luxurious client spending per current outcomes from LVMH, Kering, and West Elm. RH additionally admitted its technique of sustaining excessive costs failed, and it elevated promotions after Q1. RH’s 8% stock decline in Q2 was slower than the income drop, signaling stock liquidation pressures forward. Nevertheless, RH stays resilient, sustaining an 18% working margin regardless of promotion and visitors challenges.

Market Circumstances for Luxurious Properties

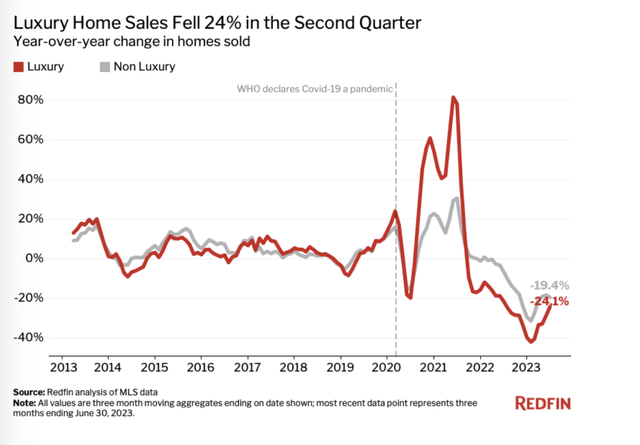

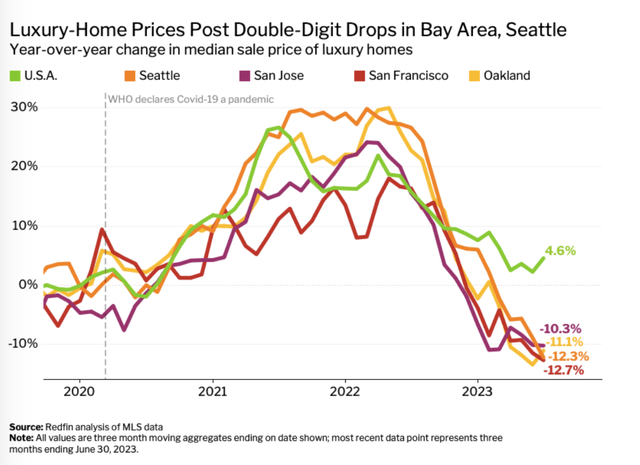

Per Redfin, luxurious residence gross sales fell 24% in Q2, the smallest drop in a 12 months, as excessive charges convey some patrons again.

Redfin

We consider the luxurious section has seen a slight easing in gross sales declines as a result of luxurious residence costs have already fallen considerably from final 12 months’s peaks. Costs dropped way more in previously scorching markets like San Francisco and Austin. This important correction in costs has made high-end properties extra reasonably priced.

Redfin

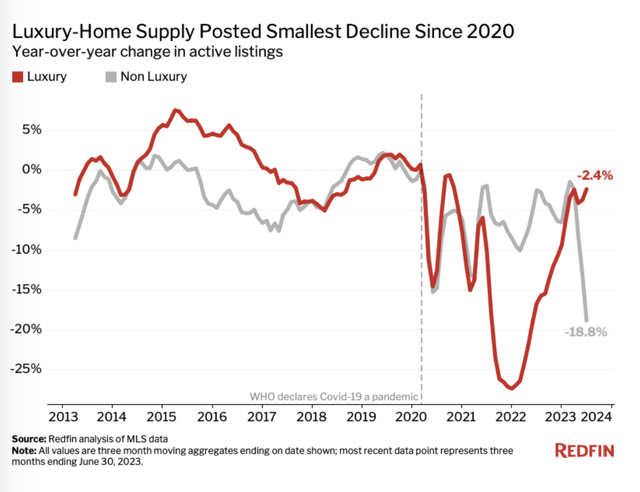

Nevertheless, whereas the availability of luxurious houses seems to be stabilizing, luxurious residence costs probably face additional downward stress in comparison with non-luxury housing. Demand for costly properties stays weak, with mortgage charges excessive and an unsure financial outlook. Although early indicators level to the market bottoming out, full restoration will probably be gradual, particularly on the high finish. Luxurious homebuilders and retailers like RH nonetheless face headwinds till gross sales volumes and costs stabilize.

Redfin

Valuation

RH has succeeded in boosting working margins considerably over the previous decade, pushed by its efficient brand-building and flagship retail experiences. Regardless of these strengths, RH’s total income development has been modest at finest. Over the previous 10 years, revenues have elevated at a compound annual price of simply 10%, even with the introduction of a membership mannequin and spectacular earnings development.

This has left RH extra of a worth play than a development inventory in our view. New retailer openings present some incremental development, however that technique has limits.

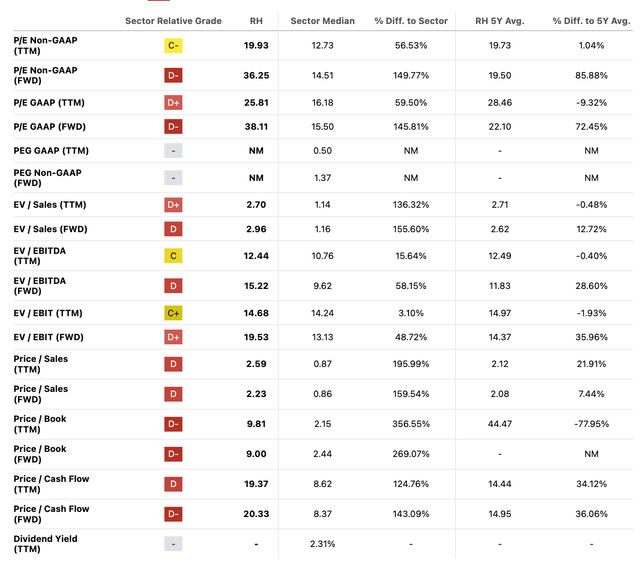

Therefore, RH doesn’t seem low cost primarily based on historic P/E or P/S ratios. The inventory’s pullback after the current earnings report appears comprehensible when factoring within the firm’s development challenges and the administration’s muted market outlook. Circumstances within the luxurious housing market additionally stay unfavorable for the following few quarters at the very least. Therefore, we don’t see the present worth stage enticing.

Searching for Alpha

Conclusion

RH CEO and Chairman Gary Friedman’s aggressive management type could not attraction to all buyers, very similar to Elon Musk’s polarizing persona. Nevertheless, we regard Friedman’s shareholder insurance policies as clear and investor-friendly. Monitoring his private inventory buying and selling gives helpful indicators on RH for buyers. The corporate has stable underlying fundamentals as a premier luxurious furnishings model. Given these strengths, RH stays a inventory price monitoring or holding long-term in our view. That mentioned, with the luxurious housing market going through ongoing pressures and RH nonetheless working by way of extra stock, the corporate shouldn’t be out of the woods but. With valuation not enticing for a worth play presently, persistence appears prudent till macro circumstances enhance and stock normalizes. We propose ready for now.

{kind=link}