AWSeebaran

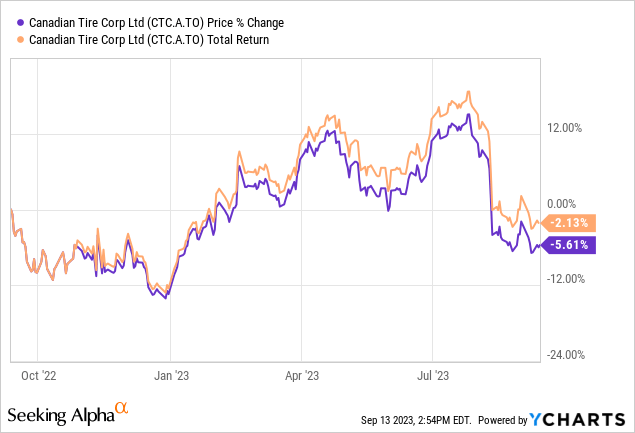

The investing neighborhood appears to be ignoring Canadian Tire (OTCPK:CDNTF) (TSX:CTC.A:CA) for now because the final Searching for Alpha protection on it was greater than 4 months in the past. The inventory has simply retreated north of 16% from a current excessive of about $185 set in July. Within the final 12 months, the inventory is down about 5% with complete returns being -2% due to the cushion from its dividend.

What’s Weighing on the Inventory?

Anticipated Upcoming Recession

An upcoming recession might be what’s weighing on the inventory. With economists anticipating a recession by 2024 in Canada, traders are most likely right to look at cautiously on the sidelines, because the inventory possible will not go a lot greater within the close to time period.

As a result of it presents sturdy items, the buyer discretionary inventory normally falls meaningfully in a recession. When Canadians are strapped for money, they might deal with the necessities like groceries. Within the Q2 report, even Greg Hicks, the Canadian Tire president and CEO, said, “As inflation endured and fee hikes continued, shopper demand for discretionary items softened, notably within the latter half of the quarter, and Canadians shifted to extra necessities inside our multi-category assortment.”

Within the final two recessions (throughout the world monetary disaster of 2008-09 and the pandemic in 2020), from peak to trough, the inventory fell greater than 40%. What’s notable is that it did backside in some unspecified time in the future throughout the recessions and subsequently made a comeback whereas paying secure dividends. So, it might be worthwhile to focus on to purchase low and promote excessive whereas gathering the dividend in between.

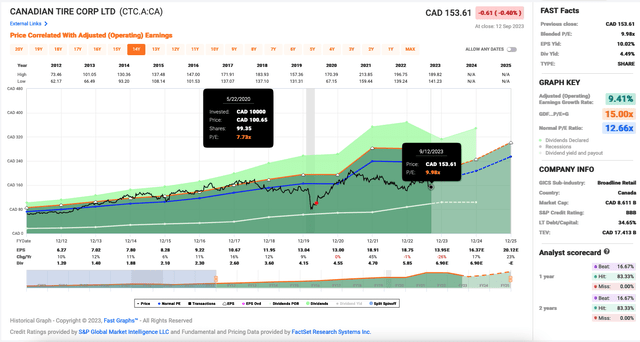

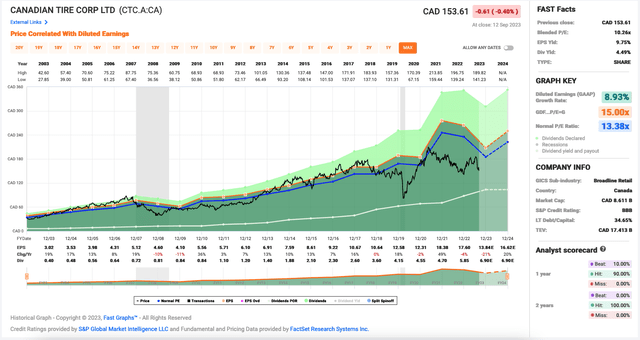

Quick Graphs

As an illustration, if you happen to had eyed the inventory and purchased it cautiously after it has bounced and made a little bit of a consolidation in throughout the 2020 pandemic crash, you’ll have made respectable annualized returns of north of 17% holding it until now, as proven within the purchase and promote factors within the above graph.

(The corporate stories in Canadian {dollars}, so the figures on this article are in CAD$ until in any other case famous.)

Credit score Score

Since 2022, the Financial institution of Canada has raised the benchmark rate of interest quickly to five.0% to curb the comparatively excessive inflation. The inventory’s credit standing is just not one of the best in at the moment’s greater rate of interest atmosphere, which will increase the price of capital for the corporate and is a dampener on financial progress. Particularly, Canadian Tire has a S&P credit standing of BBB for its long-term debt.

To get a way of the rates of interest that Canadian Tire is uncovered to, it simply pushed out $600 million price of unsecured medium time period notes, together with $400 million due September 2030 at a fee of 5.372% and $200 million at a floating fee due September 2026.

The Enterprise

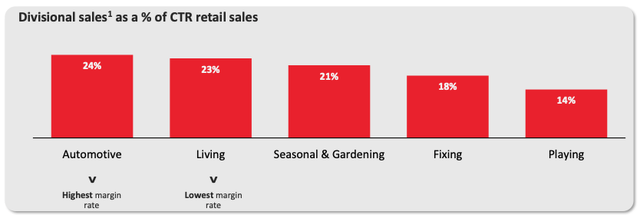

Canadian Tire is an iconic model that was based in 1922. It has picked up different retail manufacturers alongside the best way. Aside from Canadian Tire, its umbrella of manufacturers embody Mark’s (for informal and industrial put on), Professional Hockey Life (a hockey specialty retailer), SportChek, Hockey Specialists, Sports activities Specialists, and Ambiance, and so on. Particularly, its retail enterprise has 5 divisions with main gross sales coming from its higher-margin Automotive division, as proven within the graph beneath.

Company Presentation

The omni-channel merchandise retailer has 1,700 retail and gasoline shops which might be supported by its Monetary Providers division. It additionally has a stake in CT REIT (CRT.UN:CA). In 2022, Canadian Tire’s income diversification was nearly 90% Retail, nearly 8% Monetary Providers, and shut to three% CT REIT.

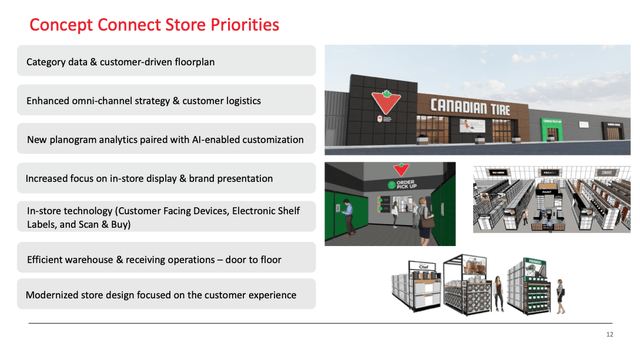

Because the announcement in 2022, the retailer has been revamping its Canadian Tire Retail shops to make them extra modern. Up to now, it has refreshed greater than 10% of the shops to enhance buyer expertise and assist drive incremental gross sales. Areas of enchancment are highlighted within the slide beneath.

Company Presentation

12 months to this point, it has invested $238 million in working capital investments and accomplished 22 of those retailer enchancment ideas.

Current Outcomes

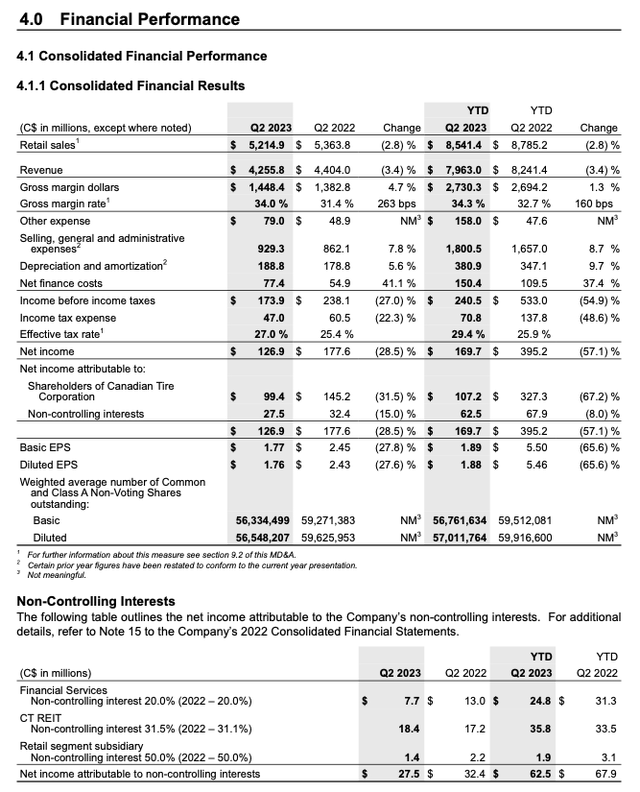

Its eCommerce gross sales hit $1.1 billion during the last 12 months. 12 months to this point, its retail gross sales fell 2.8% to $8,541.4 million. The gross margin rose 1.3% to $2,730.3 million with the assistance of the gross margin fee increasing 1.6% to 34.3%. Gross sales stayed resilient in at the moment’s macro atmosphere.

Sadly, bills jumped. Promoting, common and administrative bills added $206 million to its prices. Increased finance prices added $40.9 million. The efficient tax fee of 29.4% was additionally 3.5% greater 12 months over 12 months. In the end, the GAAP earnings dropped 57% to $169.7 million with the diluted earnings per share (“EPS”) falling nearly 66% to $1.88.

Q2 2023 MD&A

Dangers

All investments include threat. Listed below are some dangers Canadian Tire are uncovered to.

As talked about earlier, with a credit standing of BBB for its long-term debt, Canadian Tire is topic to rate of interest threat. Increased rates of interest improve its borrowing prices and make its debt a larger burden and dampens its progress potential.

Because the begin of the 12 months, Canadian Tire has accomplished the multi-year rollout of its digital platform throughout all banners. Which means, in a way, it is competing with different corporations which might be promoting comparable merchandise on-line. In keeping with Similarweb, a few of Canadian Tire’s prime on-line opponents embody Walmart (WMT), Rona that is owned by Lowe’s (LOW), and Amazon (AMZN).

That mentioned, Canadian Tire did point out that about 75-90% of its gross sales are in-store purchases. As famous within the slide beneath, its digital platform is supposed to boost or assist gross sales for its brick-and-mortar shops. So, on the finish of the day, predicting buyer demand and shopper preferences, and deciding on the appropriate merchandise to promote is vital.

Company Presentation

As a result of Canadian Tire sources its merchandise from totally different international locations, it’s uncovered to international foreign money volatility. In 2022, China was its prime sourcing nation, adopted by Canada, america, Bangladesh, Vietnam, Cambodia, Mexico, Malaysia, Taiwan, and Israel. When the Canadian greenback is weak towards these foreign currency, notably, the Chinese language Yuan and the U.S. greenback, it is going to be successful on the retailer’s backside line.

Comparatively excessive inflation can be one other threat issue. It is tougher to go greater inflationary prices to shoppers for sturdy items which might be discretionary purchases. It signifies that in lots of circumstances, Canadian Tire has to eat up that price.

Progress Catalysts

Canadian Tire targets to refresh 50% of the sq. footage in its community, which might encourage foot site visitors and the buyer purchasing expertise. Since most of its gross sales are in-store purchases, this funding can probably drive gross sales progress.

Its enterprise tends to do properly post-recessions. As properly, it tends to generate steady progress in different financial circumstances (apart from doing poorly in recessions). So, assuming Canada does fall right into a recession by 2024, traders can anticipate the inventory to do higher someday after that.

Furthermore, throughout recessions, the Financial institution of Canada tends to cut back the coverage rate of interest to encourage financial progress. The discount of rates of interest can be a progress catalysts for companies, together with Canadian Tire.

Valuation and Dividend Security

Regardless of it sells non-essential merchandise, Canadian Tire’s earnings have been in a progress pattern and largely steady, particularly if you happen to ignore the large rise in earnings in 2021 post-pandemic.

Quick Graphs

Within the final 10 years, the inventory delivered annualized returns of about 8%, which isn’t stellar. Nonetheless, at the moment, at $154.62 per share at writing, it trades at a ahead P/E of about 11.1 primarily based on adjusted EPS. It is a first rate a number of to purchase shares assuming a subsequent financial enlargement. Nonetheless, traders may want to attend for this to happen after a recession.

Within the meantime, Canadian Tire pays a secure dividend. It has maintained or elevated its dividend for no less than 20 consecutive years with 5-, 10-, 15-, and 20-year dividend progress charges of 17.6%, 17.2%, 15.0%, and 14.4%, respectively. At writing, it presents a dividend yield of near 4.5%. Its sustainable trailing-12-month payout ratio was 44% of internet earnings.

Investor Takeaway

Previously 10 years, Canadian Tire elevated its adjusted EPS by nearly 11.6% per 12 months. Being extra cautious, let’s assume Canadian Tire grows its earnings by about 8%. Then, primarily based on its affordable valuation at the moment, it ought to be capable of ship complete returns of roughly 12%, assuming no valuation enlargement over the following 5 years.

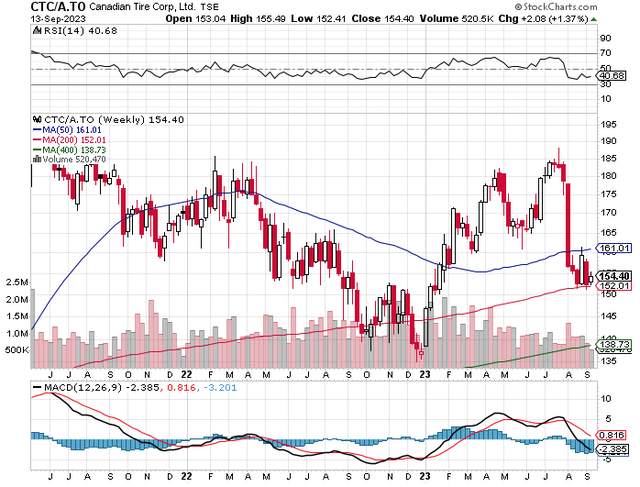

That mentioned, within the close to to medium time period, if Canada does run into a gentle recession, the inventory might be vary sure, which might make it an honest candidate for buying and selling on potential pops from any excellent news. The technical chart beneath reveals a ceiling within the $180 vary.

Stockcharts

Editor’s Observe: This text discusses a number of securities that don’t commerce on a serious U.S. alternate. Please pay attention to the dangers related to these shares.

{kind=link}