Ethan Miller/Getty Pictures Information

“If you’d like one thing you’ve by no means had, you should be keen to do one thing you’ve by no means achieved…”

Thomas Jefferson.

The case to purchase LVS now has by no means been stronger

My view of the shares of Las Vegas Sands Corp. (NYSE:LVS) over years has been the persistent puzzle to me as to why Mr. Market seems to be blind—repeat blind—to the colossal undervalued worth of this inventory and the corporate behind it.

Above: What’s Mr. Market lacking right here? Or does he know one thing we nonetheless cannot work out that simply?

I’m not one to imagine that I’ve all the time had the right tackle many a inventory, no much less the way forward for the corporate it represents. I’ve plunged many instances into the doable rationale for LVS’ low cost buying and selling vary. In spite of everything, there’s lengthy -term huge settlement within the premise that finally markets are an correct worth discovery mechanism. But, the knowledge of markets usually takes trip and snoozes by way of alternatives on one hand, and or will get wildly ODed on shares that transform whiffs disguised as 4 baggers.

I have to stipulate right here that I come from a 180-degree data of the corporate and a few of its key leaders over time. Manner again within the day, I competed with its precursor firm in Atlantic Metropolis. I additionally shared time kicking round takes on the trade with fellow on line casino executives who labored for Sheldon Adelson. We had consensus again then: Adelson was by any measure a licensed, however tough-minded, genius within the enterprise. Its present CEO, Rob Goldstein, a lawyer by commerce, started his profession means again within the tough and tumble junket enterprise. Over time, he’s reworked himself right into a worthy CEO of an LVS few ever imagined would develop to its huge management presence. Since Adelson’s dying, there was concern at what many buyers see as a generally rudderless ship, not with a sure port vacation spot. The covid disaster exacerbated that view.

The early 2022 closing of the $6.2b sale of LVS Vegas properties has been criticized as being badly timed, given the sturdy post-covid restoration on the strip. A part of the rationale put out by administration on the time was that: a) LVS’s main future was in Asia; b) The corporate can be in search of to develop in a 3rd Asian nation if alternatives opened there; c) The corporate was contemplating an entry into on-line gaming, an space of visceral opposition from Adelson; and d) Had been a chance in a serious U.S. market like New York or Texas open, LVS can be a entrance row bidder to construct.

To date solely certainly one of these pronounced pivot shifts to the LVS enterprise mannequin has nudged forward. That’s its bid for one of many three gaming licenses to be issued by the state for the metro NYC space. The corporate has been much less vocal about its intentions for an additional Asian nation regardless of a choice final spring by Thai authorities to legalize casinos there.

There may be little doubt that LVS can be the 600lb gorilla within the room if and when Thailand begins to maneuver critically past phrases. So what we have now seen that maybe is partially liable for Mr. Market’s persevering with meh response to LVS inventory, is a scarcity of conviction that its exit from Vegas and comfortable speak on different fronts has gone nowhere.

google

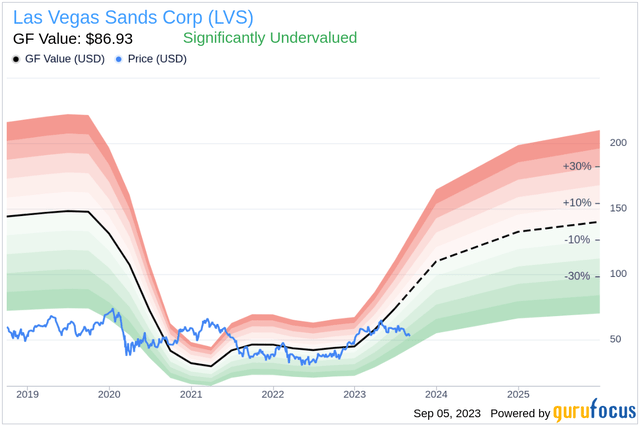

Above: Lengthy-term GuruFocus forecast agrees with our view that LVS has been and is appreciably undervalued.

Confidence within the present management has clearly waned because the dying of Adelson. Goldstein and his key persons are seen nearly as good stewards, however not guiding visionaries in taking LVS to the subsequent, promised step. Their timidity per se, has been attributed to a number of causes.

One, after almost three years because the Vegas sale, LVS’ majority holder, Dr. Miriam Adelson’s medical basis seems to be completely pleased with conserving its 50%+ fairness place entire. The restoration in Asia post-covid means the return of dividends and a half a buck of each greenback declared, goes to the inspiration.

Two, its (ttm) money pile of $5.7b is among the many tallest within the sector., It positions the corporate to behave shortly with extra fairness put into any given new growth that may hold debt in test.

google

Above: Lengthy-term management shall be sustained and elevated as we get farther away from the covid period and LVS property investments underway mature.

Three, the faster-than-anticipated restoration of GGR in each Singapore and Macau that’s already producing spectacular positive aspects in income and working earnings for LVS has contributed to a don’t rock the boat mentality in administration. Genius isn’t required right here: Take a robust surge of income from current markets, add a powerful steadiness sheet and await what could possibly be a recreation changer if New York faucets LVS for a metro space license and you’ve got a snug ready recreation. Outdoors of Vegas, the historical past of LVS has been one thing of a shoulder shrug.

It’s to be remembered that that they had a footprint in Bethlehem PA, for ten years in a renovated metal plant. The property did pretty properly however in 2019, LVS offered it to a tribal group for $1.3b with Adelson telling the Avenue that it was too small scale for company ambitions at the moment. Their present ambition for a New York mega property within the nation’s largest market feels like a plan. LVS is competing in opposition to two current state licensees of lengthy tenure, MGM (MGM) with its racino property simply over town line, and Genting’s Resorts World property within the metropolis’s borough of Queens.

Latest revelations a couple of dismissed Resorts World Vegas govt who might have stepped over the regulatory line throughout his tenure at each corporations might injure their shoo-in standing. Regardless of the result, Mr. Market isn’t more likely to see this prospect right now as a purpose to be within the inventory.

4, Mr. Market inexplicably, doesn’t look like impressed with the phenomenally speedy restoration arc seen in each LVS markets since Beijing dropped its zero covid coverage final January. The efficiency by way of 2Q23, and we consider a good higher one forward for 3Q23, has produced crickets.

And that by far has produced an unfathomable indifference to the shares of LVS by Mr. Market. In truth, the inventory has sagged a bit since its final earnings launch. So whether or not buyers consider administration is just too timid, beneath the mandates of the Adelson Basis, or establishment comfortable or simply ready to pounce if New York occurs, the result’s in our view, the identical:

At its present worth, Mr. Market is staring a screaming purchase within the face and but sitting on its fingers.

google

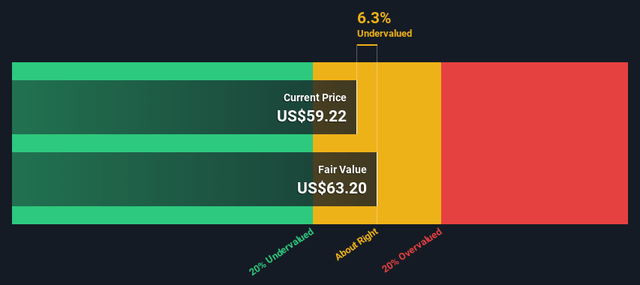

Above: Underneath probably the most conservative estimates, truthful worth is $63.20 far above the present worth at writing of $48.

Mr. Market’s valuations of LVS and friends MGM and CZR earlier than 3Q23 earnings start to reach

We’ve been followers of LVS and its two nearest friends for a number of years now. We’ve made the instances we consider that the shares of MGM Resorts (MGM) and Caesars Leisure (CZR) have likewise been underappreciated over time. They’re all stable performers in gaming with a lot rationale going to help bullish ahead eventualities for them.

And that leads us to the idea of relative worth. In different phrases, relative to shut friends, what does the LVS share worth really feel like? Pretty valued given the sector? Overvalued for causes we will’t see as dispositive. Or undervalued and to what extent?

Firm Worth at writing MC Income (ttm)

LVS $48.83 $37.1b 6.7b

MGM 39.33 13. 7 14.4b

CZR 44.81 10.7b 11.4b

Stability sheet highlights

Firm Money (mrq) LT debt Present ratio

LVS: $5.7b $14.2b 2.77

MGM: 3.83b 32.1b 2.04

CZR: 1.1b 26b 0.78

For 2Q23 LVS reported revenues of $2.54b with a internet revenue of $368m. EBITDA was $973m—the highest quarter posted since 2019. Analyst outlook for the fiscal 12 months 2023 earnings $1.93 with a projected 2024 at $2.96. Projections for income in 2023 and 2024 in line with a consensus of analysts:

2023: $10.3b. Our calculations geared to the rate we see in Macau restoration arc will get us to $10.93b for this 12 months. Analyst estimates for 2024 $12.290b. Our forecast primarily based on reaching 100% of 2019 run price earlier than the tip of 1Q24 brings us to an annual forecast of $13.3b for 2024. LVS declared $0.02 a share dividend final month and we count on a basic return to dividends to proceed.

Conclusion

Consensus analyst worth goal (“PT”) nonetheless stays round $70. We’ve raised our personal PT to the vary of $75-$80 by early Q24. SWS has calculated the discounted money circulate (“DCF”) truthful worth at $63, or ~18% undervalued at this level.

We put this on the conservative aspect. YTD Macau has already seen 17.4m guests, selecting up month-to-month because the finish of zero covid. However officers count on common day by day footfall to get again to 100,000 per day by the point of the Golden Week 8 day vacation in October. That month would be the first month because the finish of zero covid that Macau will actually be firing on all cylinders as its month-to-month GGR inches ever nearer to 2019 baseline.

In August, it continued posting GGR above the US$2b mark. (September was negatively impacted by the hurricane and Hong Kong flooding disruptions). Complete flight schedules out and in of Singapore have reached 71% of pre-covid ranges and are anticipated to enhance over the Golden Week interval.

What’s exceptional in our view is the tempo of restoration Macau and Singapore is constant regardless of the continued financial strains in China. Proper now, LVS has all its cash guess on Asia in two jurisdictions which can be exhibiting sturdy restoration in a speedy run price. But by any comparability, its shares nonetheless don’t look like responding to that bullish state of affairs. We’ve conjectured as to why after a deep dive examine of the inventory over a few years.

Right here you’ve an organization, dominant within the globe’s largest gaming market, dashing to earnings restoration sooner than most analysts first thought. It’s a firm with a powerful steadiness sheet, comparatively decrease debt in opposition to its trade friends, sturdy money positions going ahead to doable expansions forward. And it has been considered in capital allocation constructing for the long run each in Macau and Singapore capex expansions.

And but, defying logic, the inventory appears caught in significantly decrease buying and selling ranges far too lengthy. On the similar time it trades at very comparable ranges to each MGM and CZR. We might have a market huge lack of curiosity for the time being within the sector on the whole.

Or one thing extra fundamental could possibly be at work right here. Simply as we will detect a recurrent proclivity of the inventory market to overvalue some shares in favored sectors, for no cheap rationales, there’s a puzzling likewise meh amongst different shares with sturdy numbers. However when that seeming indifference reaches the extent of hole between the prospects for Las Vegas Sands Corp. and the fact of its buying and selling vary, one has I consider, found an alpha hidden in that indifference.

You go this one up at what could possibly be a heavy worth.

:max_bytes(150000):strip_icc()/What-difference-between-standard-Error-means-and-standard-deviation_color-1c203133aca641aca0d03936d9558693.jpg)

/what-difference-between-magnum-cum-laude-and-summa-cum-laude_V2-3ae02babdc714ea9adaeec0f0a6bf1a5.png)

{kind=link}