Up to date on September twenty seventh, 2023 by Nathan Parsh

Cincinnati Monetary (CINF) has a dividend observe report that few corporations can rival.

The corporate has elevated its money dividend for 63 consecutive years, making it one in every of simply 16 shares in your entire market with a dividend enhance streak of a minimum of 60 years.

That places Cincinnati Monetary among the many elite of Dividend Kings, a small group of shares which have elevated their payouts for a minimum of 50 consecutive years.

You possibly can see the total record of all 50 Dividend Kings right here.

You can even obtain an Excel spreadsheet with the total record of Dividend Kings (plus metrics that matter similar to price-to-earnings ratios and dividend yields) by clicking on the hyperlink under:

Dividend Kings have the longest observe data in terms of rewarding shareholders with rising dividends.

Cincinnati Monetary has a comparatively “boring” enterprise mannequin. However insurance coverage shares are among the many greatest shares for long-term dividend development traders. Cincinnati Monetary inventory has a 2.9% dividend yield, which is considerably above the ~1.6% common yield of the S&P 500 Index.

Because of its robust enterprise mannequin, wholesome payout ratio, and its robust stability sheet, the insurer has ample room to maintain elevating its dividend for a lot of extra years.

Enterprise Overview

Cincinnati Monetary is a property-and-casualty (P/C) insurance coverage firm based in 1950. It presents enterprise, house, auto insurance coverage, and monetary merchandise, together with life insurance coverage, annuities, property, and casualty insurance coverage. It’s headquartered in Ohio and is buying and selling with a market capitalization of $16.5 billion.

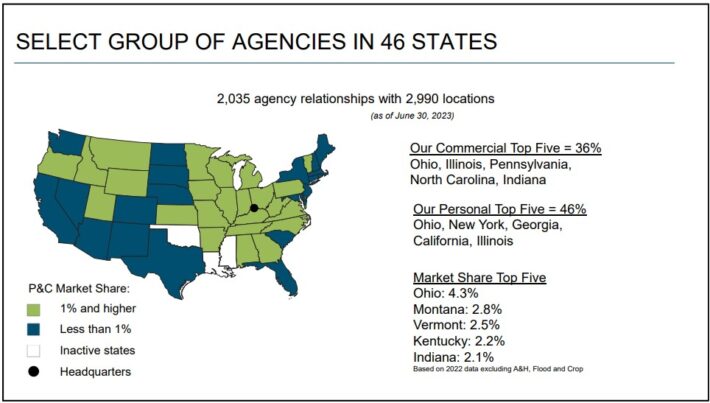

The corporate has operations in 46 states. The corporate additionally has 2,035 company relationships with 2,990 places as of June thirtieth, 2023.

Supply: Investor Presentation

As an insurance coverage firm, Cincinnati Monetary makes cash in two methods. First, it earns earnings from the insurance coverage premiums of the insurance policies it sells to its clients.

Second, it additionally earns funding earnings by investing its float, i.e., the cash it receives from its clients minus the quantity it pays out in claims.

Because of this the insurance coverage enterprise could be so profitable–insurers generate a considerable amount of float, which could be invested with a excessive price of return, thus producing compounded returns.

Then again, the P/C insurance coverage enterprise could be particularly tough for traders.

Some insurers are sometimes tempted to cut back the premiums they cost with the intention to entice extra clients and thus improve their market share. Throughout favorable years, during which catastrophic losses are low, these insurers will publish excessive ranges of earnings.

Nevertheless, a yr with excessive catastrophic losses will inevitably present up in some unspecified time in the future and can erase the earnings of all of the earlier years if the insurers haven’t adopted a prudent underwriting coverage.

Because of this traders ought to consider P/C insurers primarily based on their long-term efficiency.

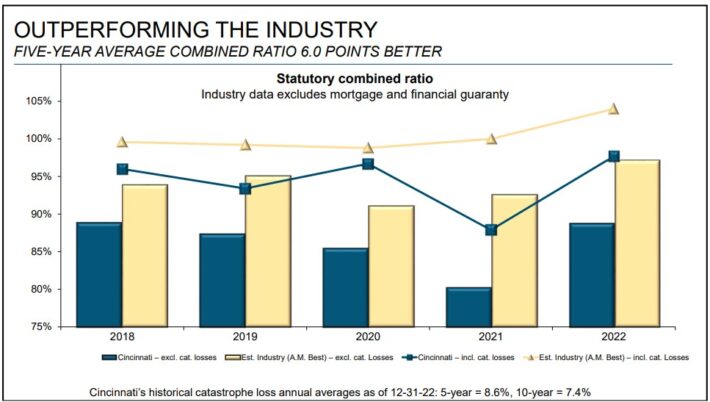

Cincinnati Monetary is healthier than common on this respect when in comparison with its friends. Within the final 5 years, the corporate has posted a mixed ratio of 6.0 share factors higher (decrease) than that of its friends.

Supply: Investor Presentation

The mixed ratio is the first index of efficiency of P/C insurers, as it’s the ratio of the quantity of claims paid to the quantity of premiums acquired. As this definition exhibits, the decrease the mixed ratio, the higher.

Cincinnati Monetary has managed to take care of a superior mixed ratio due to the predictive modeling instruments and analytics it makes use of in addition to knowledge administration with the intention to decide the likelihood of every catastrophic occasion and thus set the suitable worth for every buyer.

The superior underwriting coverage of Cincinnati Monetary is clear not solely from its superior mixed ratio but additionally from its distinctive dividend development report.

As catastrophic losses are very risky in nature, they’re extremely excessive in just a few hostile years.Consequently, it’s almost not possible for many insurers to develop their dividends throughout these few tough years.

Cincinnati Monetary is a vivid exception to this rule, because it has raised its dividend for 63 consecutive years. It is a testomony to its prudent underwriting coverage and the long-term perspective of its administration.

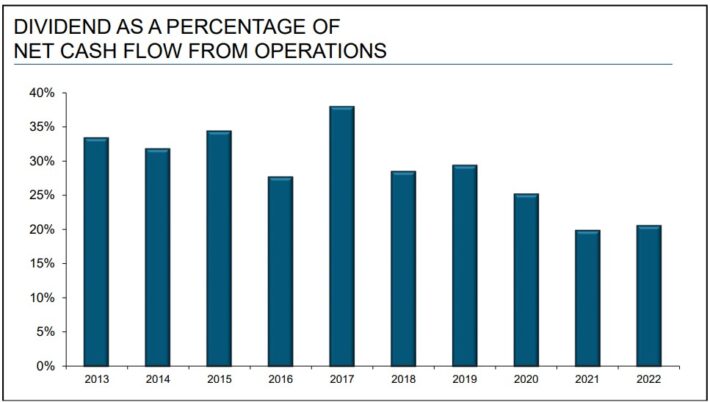

One other issue behind the distinctive dividend report of Cincinnati Monetary is the wholesome payout ratio that the corporate has at all times focused with the intention to create a large margin of security for its dividend.

Supply: Investor Presentation

Because of its wholesome payout ratio and its monetary power, the insurer can preserve elevating its dividend for a lot of extra years.

Within the second quarter of 2023, income surged 218% to $2.61 billion, whereas earned premiums improved 10% to $1.9 billion. Non-GAAP working earnings per share totaled $1.21 in comparison with $0.59 within the earlier yr.

For the primary six months of 2023, whole revenues grew 138% to $4.85 billion and earned premiums have been larger by 11% to $3.86 billion. Non-GAAP working earnings per share decreased 5% over the primary six months to $2.10 per share.

Firm ebook worth elevated 4.6% because the finish of 2022 to $70.33.

Progress Prospects

A tough yr each few years must be anticipated on this enterprise. However traders ought to deal with the long-term prospects of P/C insurers, and we imagine that the longer term development prospects of Cincinnati Monetary are intact.

We count on 6% annual earnings-per-share development over the following 5 years for Cincinnati Monetary.

Administration targets a ten% to 13% common annual development price over the following 5 years. As per its definition, the expansion price is the same as the expansion price of the ebook worth per share plus the dividends paid to the shareholders.

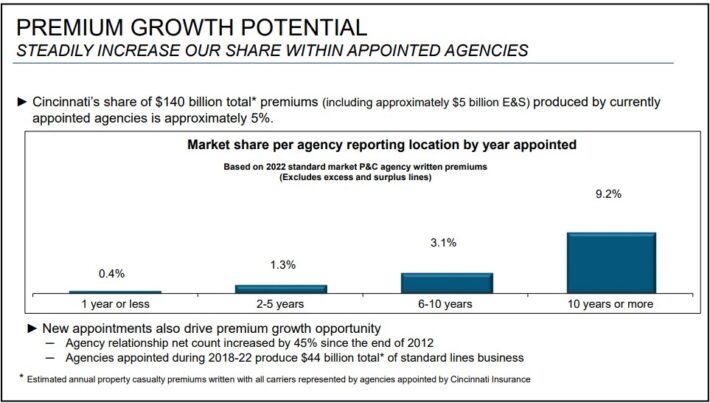

It goals to realize a ten% to 13% development price over the following 5 years, primarily by way of new company appointments and premium development within the already appointed businesses.

As proven within the chart under, Cincinnati Monetary has persistently elevated its market share in its businesses over time.

Supply: Investor Presentation

Its market share stays low within the first 5 years from the appointment of every company, however then it rises considerably and thus contributes to vital premium development.

Then again, the corporate generates an awesome portion of its earnings from its funding beneficial properties, and thus it’s extremely delicate to the prevailing rates of interest and the inventory market efficiency.

Notably, Cincinnati Monetary is a considerably aggressive investor, with 43.3% of its funding portfolio being invested in frequent equities.

Remarkably, 31.9% of its inventory portfolio is invested in know-how shares. Nevertheless, that is solely barely forward of the weighting of the S&P 500, which holds 28.3% of know-how shares. Cincinnati’s high fairness holdings are Microsoft (MSFT), Broadcom (AVGO), JPMorgan (JPM), and United Well being (UNH).

Nevertheless, this technique renders the corporate susceptible to a possible bear market.

Aggressive Benefits & Recession Efficiency

Cincinnati Monetary boasts of the good relationships it has with most of its brokers, which assist the insurer earn entry to the very best accounts of its brokers.

As well as, it has a superb repute for its monetary power and its environment friendly procedures in declare funds. These options present some type of aggressive benefit.

Then again, this aggressive benefit is slender. The P/C insurance coverage is characterised by intense competitors, which has heated greater than ever in recent times.

Warren Buffett has repeatedly said that the very best days for insurers belong to the previous as a result of present intense competitors. Furthermore, Cincinnati Monetary is susceptible to recessions because of its excessive publicity to the inventory market and its sensitivity to rates of interest.

Throughout recessions, rates of interest stay depressed and thus take their toll on the insurer’s bond portfolio yield. Nevertheless, Cincinnati Monetary’s means to generate robust money move, and preserve profitability even throughout recessions, has allowed it to boost its dividend for six a long time.

Valuation & Anticipated Returns

We count on Cincinnati Monetary to generate earnings-per-share of $5.00 this yr. In consequence, the inventory is buying and selling at a ahead price-to-earnings ratio of 21.0, which is simply forward of our truthful worth P/E goal of 20.0.

In consequence, it seems that the inventory is barely overvalued proper now.

If the inventory reaches our truthful degree over the following 5 years, then a number of compression will act as a 1% headwind to whole returns over this era.

We additionally count on 6.0% annual EPS development over the following 5 years whereas the inventory additionally presents a 2.9% dividend yield. Due to this fact, we estimate whole returns at 7.6% per yr over the following 5 years.

Ultimate Ideas

Cincinnati Monetary is a high-quality P/C insurer. The distinctive dividend report of the corporate, with greater than six a long time of annual raises, is a testomony to its disciplined underwriting coverage.

The inventory is considerably overvalued proper now, however to not an awesome diploma.

Regardless of the qualities of the corporate and the attractiveness of each the dividend yield and development streak, we price Cincinnati Monetary as a maintain because of whole return potential.

The next articles include shares with very lengthy dividend or company histories, ripe for choice for dividend development traders:

Thanks for studying this text. Please ship any suggestions, corrections, or inquiries to [email protected].

/what-difference-between-magnum-cum-laude-and-summa-cum-laude_V2-3ae02babdc714ea9adaeec0f0a6bf1a5.png)

:max_bytes(150000):strip_icc()/What-difference-between-standard-Error-means-and-standard-deviation_color-1c203133aca641aca0d03936d9558693.jpg)

:max_bytes(150000):strip_icc()/GettyImages-1529792128-03b50b785da845aebb6d00b232c45596.jpg)

{kind=link}