Robert Method

Again in Could, I wrote that whereas PDD Holdings (NASDAQ:PDD) appeared attractively valued, I believed there was an excessive amount of controversy across the title. With the shares up over 50% since then, let’s atone for the inventory.

Firm Profile

As a refresher, PDD operates two e-commerce platforms: the Pinduoduo e-platform in China and the Temu platform internationally. Its most important e-commerce providing is the Pinduoduo platform, the place it entices its customers to make group purchases by providing decrease costs on staff purchases. Most of its income is generated from on-line advertising providers for its market, whereas round 20% of its income comes from service provider charges for value-added providers.

The corporate’s Temu platform, in the meantime, permits clients to buy straight from Chinese language and different international producers and types. PDD launched the platform final 12 months.

Large Q2 Lifts The Inventory

In my July follow-up on PDD, I mentioned that Q2 was an essential quarter for the corporate, as rivals took goal on the firm’s Chinese language e-commerce platform throughout the 618 procuring pageant in June. The corporate shrugged off the competitors and posted some very large outcomes.

For Q2, PDD noticed income soar 66% to $7.21 billion, crushing the $6.03 billion consensus within the course of. Income from on-line advertising providers jumped 50% to $5.2 billion, whereas transaction service income climbed 131% to $5.2 billion.

Gross margins got here in at 64.3%, down from 74.7% a 12 months in the past. Gross sales and advertising bills elevated 55% 12 months over 12 months. Nonetheless, as a share of income, S&M was 33.5% versus 36.0% a 12 months in the past.

The corporate mentioned it aggressively launched promotions to spice up demand, together with low cost coupons and promotions across the 618 procuring pageant. Promotions ran throughout classes, together with in areas of attire, electronics, cosmetics, and produce. The corporate mentioned that the general market in China has been bettering and that consumption is up as customers are extra prepared to buy popping out of lockdowns.

Adjusted earnings per ADS have been $1.44, topping the consensus by 42 cents.

When requested about competitors of its name, Co-CEO Jiazhen Zhao wrote:

“We observed modifications within the trade. And as consumption covers and customers present stranded demand, it isn’t shocking for us to see friends organising on subsidies. Competitors is certainly changing into extra intense. And we consider that wholesome competitors, which is pushed by consumer-centric objective can profit the trade, which incorporates not solely the customers, but in addition the platforms as nicely. The e-commerce trade is all the time quickly evolving. And for us, the important thing to adapting to the speedy modifications is to not concentrate on what our rivals are doing. As a substitute, it’s to remain laser-focused on shopper demand and store our personal abilities and in addition to face competitors straight and in addition briefly. We channel aggressive stress into extra motivation to strengthen our core competencies and concentrate on implementing our high-quality growth technique. And serving clients nicely is on the core of our worth creation. We’re deepening our capabilities of offering extra providers, extra financial savings stays crucial to us. And final quarter, for instance, we invested $1 billion within the producing promotion to cowl all product classes and ensure customers have entry to high quality merchandise at inexpensive costs. And optimistic shopper expertise requires a complete effort. It isn’t nearly worth, and we proceed to concentrate on R&D to know and in addition adapt to customers’ evolving wants to assist customers store with a peace of thoughts. We additionally work very exhausting to offer higher providers, which incorporates, for instance, upgrading logistics and in addition after-sale help.”

The corporate didn’t give a lot of an replace on Temu when requested about it, solely saying that it’s nonetheless presently within the studying stage and that its staff is laser-focused on understanding cultural preferences and shopper demand in worldwide markets.

Regardless of stories of weaker-than-expected spending by the Chinese language shopper throughout the 618 procuring pageant and elevated competitors coming from the likes of JD.com (JD) and Alibaba (BABA), PDD put up robust ends in Q2. The corporate does seem to have sacrificed a variety of gross margins to develop, however the trade-off this quarter was price it.

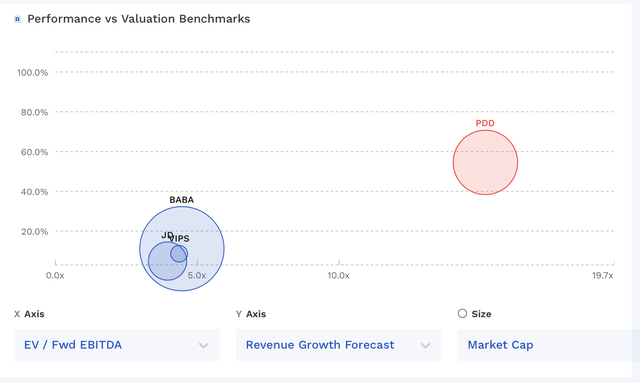

I might nonetheless wish to see some disclosures round Temu and what that platform is definitely contributing to gross sales at the moment. It additionally appears odd how all media stories indicated that the 618 vacation was weak whereas PDD put up such robust progress. By comparability, JD’s Retail unit noticed 5% progress, whereas BABA’s Taobao and Tmall noticed income develop 12% within the quarter, so the 66% income progress from PDD was miles forward of two rivals that have been taking goal on the firm.

Bear Assault

In my unique article on PDD, I famous that the corporate had a variety of controversy round it, as its most important platform had been found to allegedly spy on its clients and there had been a variety of allegations towards its Temu operations, together with the U.S.-China Financial and Safety Overview Fee placing out a report that it and Shein have been potential dangers to the U.S.

Not surprisingly, with the inventory rallying, the corporate has come underneath the scrutiny of shorts, with Grizzly Analysis posting a brief report earlier this month. A lot of the report goes into the problems with Temu and accuses it of mainly being malware/adware. Given the issues of the U.S. authorities in regards to the app and that the corporate’s most important platform was caught spying on its Chinese language clients, this argument is not a lot of a stretch in my view.

Nonetheless, Temu should not be the motive force of the inventory – though we will not be certain as a result of the corporate would not disclose something about it or speak a lot about it. Alongside these strains, Grizzly additionally factors out that PDD’s reporting may be very a lot a black field, with the corporate eliminating disclosures over time, together with issues equivalent to GMV, month-to-month energetic makes use of, energetic patrons, and annual spending per energetic purchaser. The report additionally factors out the rising competitors, which I’ve talked about, in addition to a myriad of different points.

A brief report popping out on PDD should not come as a shock, given the well-documented controversy surrounding Temu. The corporate has grow to be much less clear over time, which additionally results in extra scrutiny. At my outdated agency, whereas I didn’t cowl the corporate, I do know after the corporate IPO’d we had some issues over the best way it reported some metrics. Whereas public quick stories are sometimes sensationalized, I feel PDD must be much more forthcoming with its metrics, particularly with regard to Temu.

Valuation

PDD trades at 15x the 2023 EBITDA of $7.0 billion and 11.6x the 2024 EBITDA consensus of $9.1 billion.

On a PE foundation, it trades at 20.6x EPS estimates of $4.80. Primarily based on the 2024 consensus for EPS of $5.94, it trades at 16.7x.

It is projected to develop income by 78% in 2023 and 24% in 2024.

The inventory trades at a a lot greater valuation than its Chinese language e-commerce friends however can be projecting a lot stronger progress.

PDD Valuation Vs Friends (FinBox)

Conclusion

With PDD’s latest surge in worth and the controversy surrounding Temu, I will transfer the inventory to “Promote.” To me, the corporate’s most up-to-date numbers do not make a variety of sense given the media commentary on total 618 vacation spending and the way its friends who have been aggressively going after the identical market as PDD carried out.

This might point out that a lot of this progress may very well be coming from the extremely controversial Temu, which is presently underneath scrutiny by the U.S. authorities as a menace. With out PDD giving clear disclosures, nobody on the surface really is aware of whether or not Temu has grow to be a progress driver for the corporate or if it’s a small contributor, however the firm has been aggressively selling and increasing the platform. If the federal government bans the app or takes different motion, although, PDD’s inventory will seemingly take a success.

:max_bytes(150000):strip_icc()/Paycheck_AdobeStock_154492502_Editorial_Use_Only-b62ac70013ec4e13b3e2a73be5e9c239.jpeg)

{kind=link}