Angelo Merendino

It has been almost 2 months since I introduced to the world that I am nonetheless avoiding Norfolk Southern Company (NYSE:NSC), and in that point, the shares are down about 13.4% in opposition to a lack of about 4.6% for the S&P 500 (SP500). That is gratifying to some extent, however it is time to evaluation the identify but once more as a result of the shares are actually much more low cost than they had been final April once I purchased the shares. For that motive, it is time to evaluation the enterprise once more. I’ll evaluation the most recent visitors patterns now we have obtainable to us, and evaluate these to the present valuation to see if it is sensible to purchase again in or not.

I am the type of reader who likes to learn the ultimate web page of a novel to see how issues work out as a result of I do not like surprises. I assume the identical of my readers on this discussion board. You did not come right here for me to hit you with an expectation-subverting plot twist on the finish of my article. You wish to know what I am considering upfront. For this reason I write a “thesis assertion” initially of every of my articles. It offers you greater than you usually get from a title and bullet factors, however a lot lower than you get from all the article. As importantly, it lets you recognize what you are getting on the outset.

Despite the truth that visitors continues to say no, I’ll be shopping for again into Norfolk Southern this morning. It’s because the valuation has grow to be engaging to me as soon as once more. I’m of the view that shares must be eschewed after they’re too costly, and they need to be embraced after they’re sufficiently low cost, and, for my part, this inventory is now sufficiently low cost to purchase. As I wrote earlier, I believe the dividend in all fairness nicely lined, and I believe there’s room for development on that entrance over the following decade. For that motive, I am snug shopping for regardless of the truth that the yield is about 200 foundation factors decrease than the 10-year Treasury Be aware (US10Y).

Site visitors Assessment

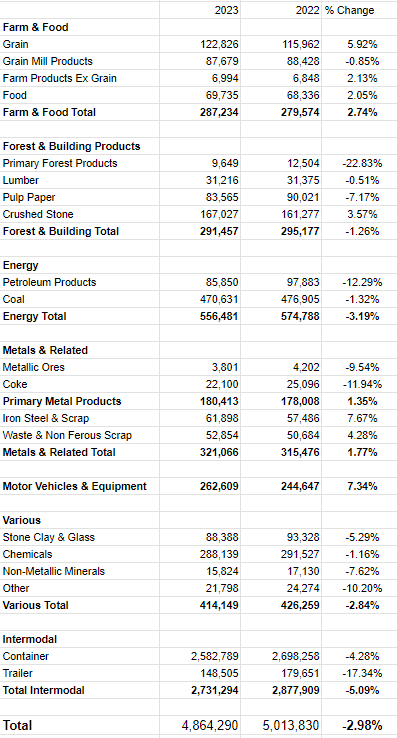

In case you’ve got forgotten, I will remind you that Norfolk Southern is a railroad, and because of this they make their cash hauling stuff. They concentrate on hauling cumbersome, heavy objects with low per unit worth. We see from the desk beneath that thus far this yr, the corporate has hauled about 3% much less “stuff” this yr than they did final yr. Most apparently to me, “forest and constructing supplies” and “vitality” had been down, generally dramatically from final yr. This may occasionally provide insights into what is going on on with the broader economic system, together with building, and the varied vitality sectors.

In any occasion, to ensure that me to purchase again into the identify, I might must see the valuation replicate this slowdown, decrease present value or not.

Norfolk Southern Site visitors to Week 35 (Norfolk Southern investor relations)

The Inventory

When you learn me often for some motive, you recognize that I think about the inventory and the enterprise to be two various things. For example, the enterprise generates income by hauling actually heavy stuff. The inventory, in the meantime, is a slip of digital paper that will get traded round within the public markets. This inventory represents a declare on the longer term revenues and profitability of the enterprise, and one motive that the inventory bounces round a lot in value is as a result of individuals change their minds often about that future profitability. Within the brief time period, although, the inventory’s value actions are extra unstable than most modifications within the underlying enterprise.

For example, if somebody purchased Norfolk Southern on July 28 (the day after they reported their newest earnings), they’re down about 19% on their funding. In the event that they purchased just about an identical shares almost two months later after Transportation Secretary Buttigieg introduced $1.4 billion in funding, they’d be down solely about 5.9%. Both manner, not sufficient occurred from July 28 to now to account for a close to 20% discount within the worth of this inventory. So, we might “purchase companies” in an summary manner, however in actuality we entry the money flows of that enterprise through the very capricious inventory.

In my expertise, this volatility is irritating, however it’s the one supply of sustainable income in terms of shopping for and promoting shares. Particularly, I am of the view that the one technique to make cash buying and selling shares is to work out the assumptions which can be at present embedded in value, and commerce in opposition to these assumptions when they’re unreasonably optimistic or pessimistic. Taking note of what’s identified by most different buyers at this time is comparatively ineffective as present information is already “priced in.”

Moreover, I believe it is value noting that purchasing low cost shares tends to result in greater returns. Within the instance above, the one who purchased when the shares had been cheaper had a “much less unhealthy” return. Not solely are low cost shares decrease threat as a result of they’ve far much less to drop in value, additionally they provide better potential reward, as a result of it is simpler for the businesses of those shares to outperform low expectations.

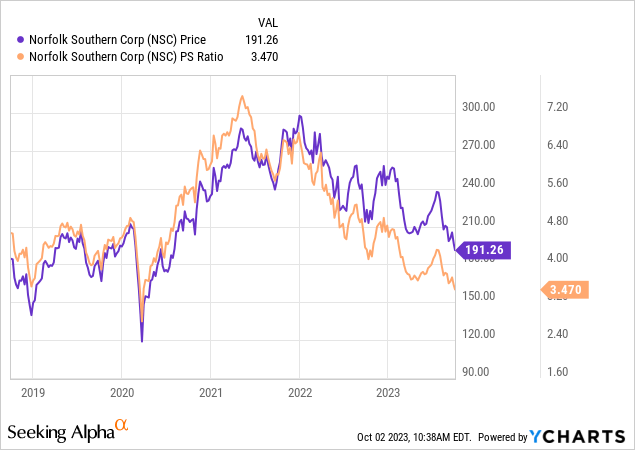

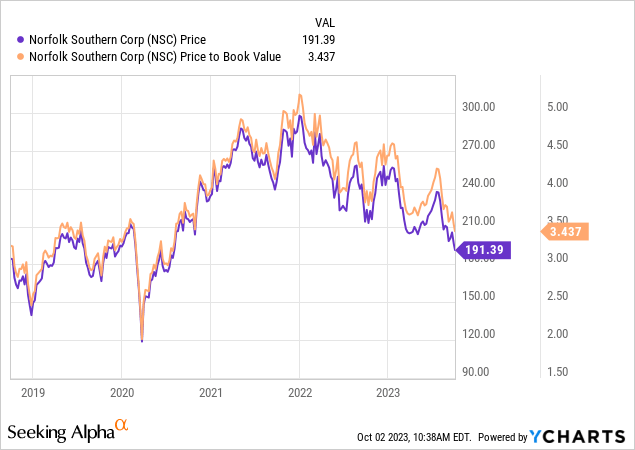

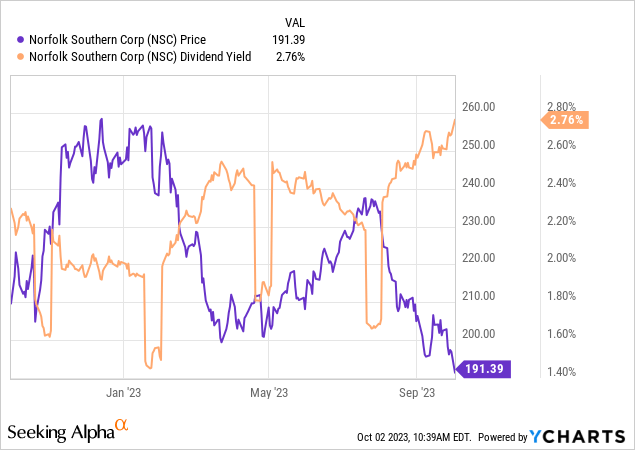

My regulars know that I measure “low cost” in a couple of methods, starting from the easy to the extra complicated. On the easy facet, I like to take a look at the ratio of value to some measure of financial worth, like earnings, gross sales, and the like. I purchased Norfolk Southern in April when the inventory was buying and selling at a price-to-sales ratio of about 3.74 occasions, a price-to-book worth of three.62 occasions, and sported a dividend yield of two.5%.

Quick-forward to the current, and issues look much more engaging at this time. The shares are between 5% and seven.2% cheaper than they had been once I final purchased, and the dividend yield is greater by about 10% greater. I will admit that the yield continues to be almost 200 foundation factors beneath that of the 10-year Treasury Be aware, however I believe there’s some room for dividend development over the following decade.

You might recall that I wrote that the one technique to make cash in shares in my estimation is to identify discrepancies between expectations and subsequent actuality. Which means, then, that we have to work out what the assumptions are at present. Once more, I wish to purchase when the group’s expectations are too dour and promote when the group turns into too rosy. Moreover, I wish to attempt to quantify these expectations as a lot as doable, and to try this, I flip to the works of Stephen Penman and/or Mauboussin and Rappaport.

The previous wrote an important e-book referred to as “Accounting for Worth” and the latter pair not too long ago up to date their traditional “Expectations Investing.” All of those writers think about the inventory value itself to be an important supply of knowledge, and the previous specifically helps buyers with some arithmetic essential to work out what the market is at present “considering” about the way forward for a given enterprise. This includes a bit of highschool algebra, the place the “g” (development) variable is remoted in a regular finance formulation. Making use of this strategy to Norfolk Southern in the mean time suggests the market is assuming that earnings will develop at a charge of about 4% from present ranges. Though that is barely optimistic, it isn’t egregiously so. On condition that Norfolk Southern Company shares are in any other case cheap, I am snug shopping for again into this enterprise with its fantastic “moat.”

:max_bytes(150000):strip_icc()/What-difference-between-standard-Error-means-and-standard-deviation_color-1c203133aca641aca0d03936d9558693.jpg)

/what-difference-between-magnum-cum-laude-and-summa-cum-laude_V2-3ae02babdc714ea9adaeec0f0a6bf1a5.png)

{kind=link}