Eloi_Omella

It is a troublesome time for REIT buyers. Intrinsically linked to rates of interest, it might be robust to discover a REIT ticker that hasn’t fallen since charges started rising sharply final yr.

Spanish REIT Merlin Properties (OTCPK:MRPRF) is not any exception, albeit with a really welcome ~2,000bps outperformance versus its European REIT peer group (represented right here by the STOXX Europe 600 Actual Property Index).

Fig 1 (Supply: Morningstar)

Merlin operates a diversified property portfolio throughout Spain and Portugal, primarily in Madrid, Barcelona and Lisbon. Workplace is the most important publicity by property class (just a little underneath 55% of gross rental earnings), adopted by procuring malls (~27%) and logistics (~17%).

Massive workplace publicity has been one thing of a priority for US REIT buyers just lately given the persevering with excessive emptiness charges in sure areas. Nonetheless, simply as not all US workplace is in hassle, so goes the scenario in Europe. Some elements of the European workplace area are undoubtedly struggling resulting from work-from-home traits (e.g. monetary district properties in Paris and London), however Merlin’s portfolio appears to be doing simply fantastic proper now.

My major concern with Merlin is principally all macro associated, with rising cap charges placing downward strain on the valuation of its portfolio. Whereas that may likewise threaten debt-to-equity ratios and so forth, asset divestments final yr imply that Merlin is now in a superb place to see off the challenges posed by greater rates of interest.

On the flip aspect, investing in REITs when charges have topped out has traditionally been a good suggestion, and there’s a cheap probability that we’re near (or at the very least very close to) the highest on this cycle. With the shares at present buying and selling at round 13x management-guided FY2023 AFFO per share, Merlin might be a superb longer-term cut price except you assume Eurozone charges have a lot additional to rise.

So Far, So Good In 2023

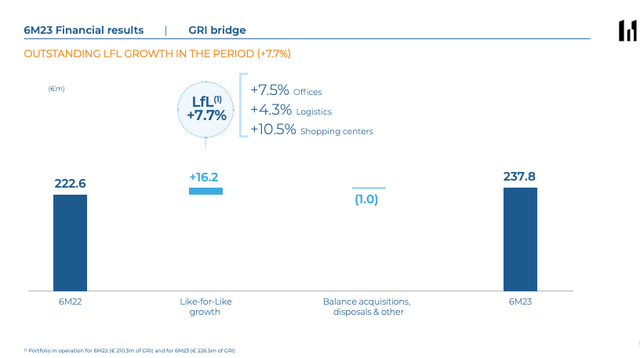

Inflation could also be unhealthy for REITs within the sense that it sometimes means greater curiosity and low cost charges and decrease property valuations, but it surely does usually imply greater rental funds too. Merlin is seeing that dynamic play out at present, with gross rental earnings up 7.7% YoY in H1 on a like-for-like foundation.

Merlin’s underlying property portfolio is performing effectively. Workplace is an space that’s coming in for growing scrutiny proper now, comprehensible given the strain that work-from-home is having on sure elements of the area, however Merlin’s publicity would not appear to be a trigger for a lot concern. Occupancy in its workplace portfolio was 92.3% in 1H2023, a circa 190bp enchancment YoY to take it a shade above comparable-period pre-COVID 2019 ranges. Workplace rents have been up 7.5% YoY on a like-for-like foundation, with the discharge unfold (i.e. distinction between new lease on renewal and prior lease) coming in at 3.2%.

Supply: Merlin Properties Interim FY2023 Outcomes Presentation

Merlin’s procuring malls are additionally performing effectively after a difficult previous few years, with occupancy ranges as much as a report 96.4%, like-for-like lease up 10.5% YoY, and launch unfold additionally up by 10%.

Macro Nonetheless The Major Danger

Merlin’s major threat proper now’s macro associated. Rising yields pose a couple of points, most clearly within the type of decrease property valuations and costlier funding prices. As stable as its properties’ cashflow efficiency is proving, this will solely go to date within the face of upper yields. Merlin’s gross asset worth fell 1.4% YoY in 1H2023 following a 1.5% decline in 2022.

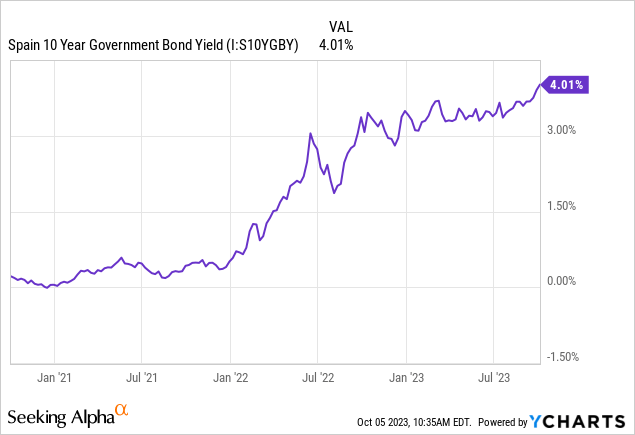

Given the above, an funding in Merlin is usually negatively correlated to Spanish 10-year authorities bond yields, which have been heading greater:

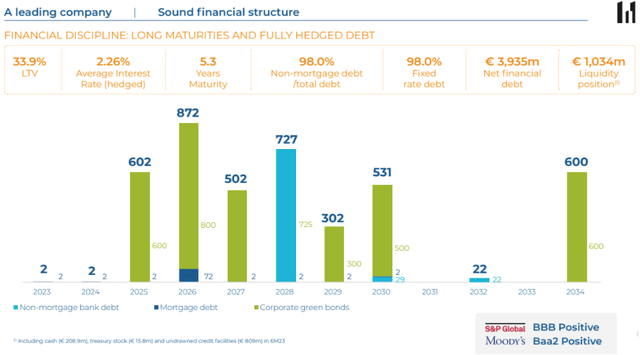

Administration has been proactive in getting Merlin into a superb place to face this problem. It raised round €2 billion final yr from numerous asset disposals, primarily from the sale of a portfolio of tons of of BBVA (BBVA) financial institution branches. With the proceeds administration has paid down debt, lowering Merlin’s loan-to-value ratio to only underneath 34% versus over 39% on the finish of FY2021. That offers it a level of headroom to soak up additional probably declines in property valuations. I would additionally add that debt discount means there aren’t any maturities due right here till mid-2025, lowering the necessity to search out funding or promote belongings outdoors of administration’s normal capital recycling plans.

Supply: Merlin Properties September 2023 Outcomes Presentation

There’s one other threat from greater charges, in fact, and that’s that they bring about about an financial downturn. The Spanish economic system has really been considered one of Europe’s bright-spots in current instances, a welcome change from being considered one of its sick sectors within the 2010s. GDP progress is at present forecast to develop 2.2% in 2023, earlier than moderating to 1.9% in 2024. Even so, a pointy downturn stays a threat to think about given the potential detrimental impression on occupancy ranges and lease renewals.

Merlin shares commerce arms for €7.88 apiece at time of writing in Madrid buying and selling, placing them at round 13x FY2023 AFFO steering (€0.60 per share). The dividend yield is 5.60% based mostly on FY2023 steering of €0.44 per share. Up to now, Merlin’s dividend yield has traded on roughly 150-200bps unfold versus the Spanish 10-year yield. At 400bps proper now, that may make the present share value roughly honest.

The place Merlin goes from right here is due to this fact largely a query of the place you assume charges are headed. Eurozone inflation slowed once more in September as per In search of Alpha, with core inflation likewise falling. That raises the prospect that the ECB could also be near being performed so far as this climbing cycle goes. Having delivered some dovish remarks when it final raised charges in September, there may be good cause to assume that is perhaps the case. If that’s the case, now might be a superb time to take a better have a look at these shares, however the persevering with robust surroundings for REITs extra usually.

Editor’s Observe: This text discusses a number of securities that don’t commerce on a serious U.S. trade. Please pay attention to the dangers related to these shares.

:max_bytes(150000):strip_icc()/GettyImages-1094465614-21bbc343266042b6ac2ce060d95cf44a.jpg)

{kind=link}