Michael Vi

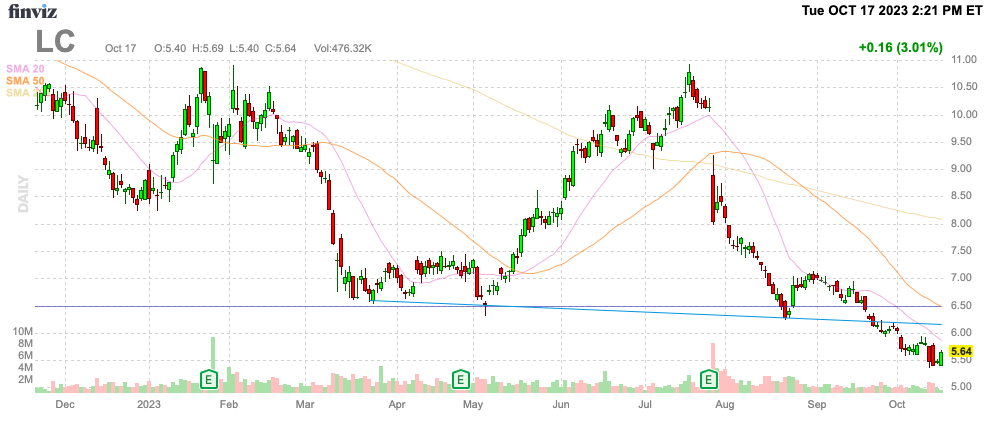

LendingClub Company (NYSE:LC) pre-announced blended outcomes for Q3’23 after a tough 18 months for the fintech. The digital financial institution trades on the lows after updating Q3 numbers and saying one other workforce discount to additional cut back prices. My funding thesis stays extremely Bullish on the inventory, which is buying and selling simply above $5.50, as a result of a deep valuation and higher prospects forward each time the buyer mortgage market normalizes.

Supply: Finviz

Blended Q3

LendingClub pre-announced the next blended Q3 2023 numbers:

Income between $198 to $200 million. Web revenue of $4 to $5 million. Mortgage originations of $1.5 billion. Reduce workforce by 14% for annualized run-rate financial savings of $30 to $35 million.

The most important information is that the digital financial institution is shedding 14% of the workforce, or 172 workers. The corporate forecasts saving at the least $7.5 million per quarter in decrease working bills.

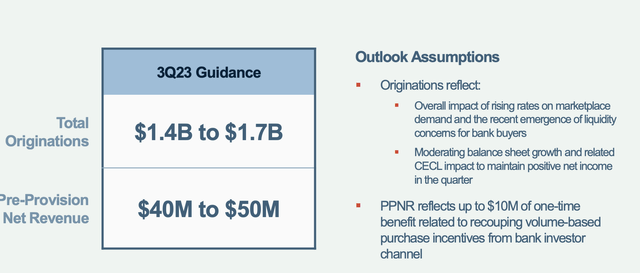

LendingClub had offered the next Q3 steering together with the Q2 ’23 earnings report:

Supply: LendingClub Q2’23 presentation

The Q3 ’23 numbers seem to usually be within the vary of prior targets, with the consensus analyst income estimates at $199 million. The mortgage originations are on the decrease finish of steering, however the numbers simply prime the $1.4 billion low-end goal.

Revenues are set to dip from $232 million within the prior quarter and $305 million again in Q2’22. LendingClub has deliberately lower mortgage originations as a result of fears of upper credit score losses and funding companions pulling again on shopping for loans because of the huge enhance in rates of interest and the disconnect with funding.

Contemplating LendingClub is eliminating ~$8 million in quarterly working bills, the Q3 revenue stage would approximate $12 million in This fall. The enterprise stays below strain, however the fintech remains to be worthwhile.

Priced For Catastrophe

The one disappointing side of LendingClub is that these fixed workforce reductions do not seem to place the corporate for future development. The fintech lower the workforce by an equal 14% again in January, chopping 225 jobs on the time.

LendingClub purchased the digital financial institution partly to develop financial institution choices, and administration usually hasn’t made the product expansions with a extra conservative give attention to being worthwhile within the quick time period.

The inventory has a market cap of solely $600 million, with annual income operating at an $800 million clip after 18 months of depressed lending already. The underside is difficult to select contemplating the U.S. financial system nonetheless faces a possible recession, however the inventory ought to commerce at multiples of this stage when lending normalizes at far greater ranges.

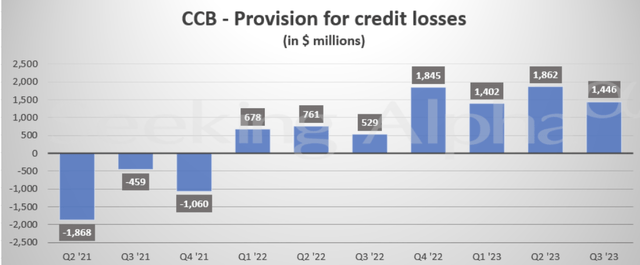

The most important worry is greater credit score losses going ahead with the U.S. headed right into a recession. The massive banks reported robust Q3 outcomes with greater provisions for credit score prices, however a financial institution like JPMorgan Chase (JPM) is not really reporting greater provision with Q3 ’23 provisions for credit score losses under Q2 ranges and a common peak again in This fall ’22.

Supply: Searching for Alpha

LendingClub focuses on private loans, so the credit score numbers from a giant financial institution aren’t precisely an entire match. The fintech is concentrated on the a part of the credit score spectrum hardest hit throughout a recession, not like a number of the company clients of JPMorgan which might be unlikely to be impacted a lot by a recession.

The inventory is now priced for catastrophe, buying and selling close to $5.50 when the digital financial institution has an EPS stream topping $1 in regular instances. LendingClub stays poised to develop the product choices of the digital financial institution to develop earnings off a $1+ EPS base.

Takeaway

The important thing investor takeaway is that LendingClub inventory is insanely low cost, however shares in all probability will not rally within the close to time period. Till a home recession shakes out and the Fed quits climbing rates of interest, LendingClub will stay on pause from aggressively rising the mortgage origination fee. In the end, although, the upside alternative makes the inventory worthy of proudly owning at these low ranges even figuring out a rally may not happen within the close to time period, however a giant rally is prone to finally happen.

:max_bytes(150000):strip_icc()/What-difference-between-standard-Error-means-and-standard-deviation_color-1c203133aca641aca0d03936d9558693.jpg)

/what-difference-between-magnum-cum-laude-and-summa-cum-laude_V2-3ae02babdc714ea9adaeec0f0a6bf1a5.png)

{kind=link}