DecHogan

Your continued suggestions is vastly appreciated, so please go away a remark with ideas.

A month of wealth destruction is upon us. Guide values and share costs plunged. These losses aren’t all non permanent. Sorry, that’s not the way it works. Costs go up and down, however big swings in rates of interest create everlasting losses.

I warned traders about this in September. I warned traders a number of instances. To these of you who protected yourselves, congratulations.

Let’s go over some latest outcomes.

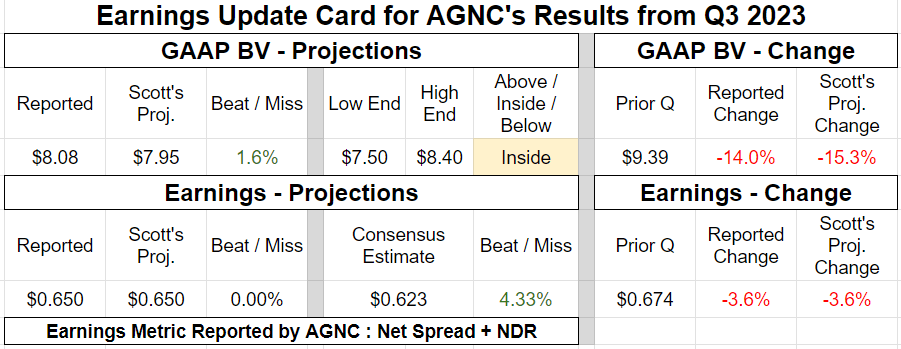

AGNC Funding (AGNC) preannounced their outcomes. Can’t blame them. When an analyst comes out calling for tangible BV of $7.85 with web unfold and greenback roll earnings at $.65 per share, they’ve gotta do one thing. That estimate was simply too good.

The REIT Discussion board

In addition they introduced their estimated BV as of 10/20/2023.

The mid-point of their vary was $6.90.

Scott’s estimate for a similar day was $6.85.

Did Halloween come early? These guide values are so correct it’s spooky.

The REIT Discussion board

I feel AGNC hoped the shares wouldn’t drop practically so far as they did. If shares solely declined reasonably, it might’ve been an incredible alternative to concern shares. AGNC had a completely huge premium to tangible guide worth. Shares closed 10/23/29023 at $8.11. They’re presently $7.16. Down 11.7%.

They have been down as a lot as 10% after hours on the report. All of the bears have been feeling fairly good.

The REIT Discussion board

How did we see this coming?

Forecasting Apparent Worth Declines

AGNC was buying and selling at about 1.2x tangible guide worth. That was hilariously overpriced. Traders may purchase friends round guide worth.

Which one sounds higher?

$100 for $100 of fairness in a peer

$120 for $100 of fairness in AGNC

Most of you may guess which one is best, however it’s the $100 of fairness in a peer. There are friends which are each bit pretty much as good as AGNC. When there’s an enormous hole in valuation, you don’t wish to personal the expense one.

That’s how we forecasted the decline in share worth.

However the true query is:

How did we forecast the plunge in guide worth?

Nice query! Thanks for asking.

I may put collectively 4,000 phrases. Boring. No thanks. Most of you don’t wish to learn 4,000 phrases, and I don’t wish to kind them. Brevity is the soul of wit.

Forecasting Guide Values

That is meant to be concise.

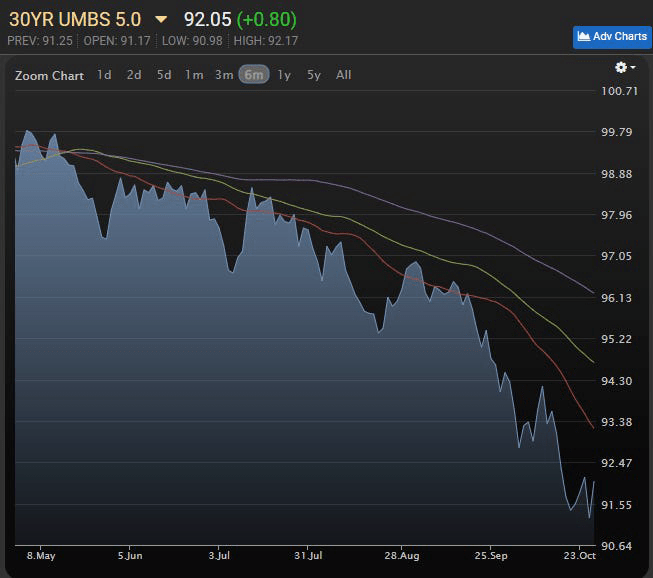

Asset values plunged:

MBSLive

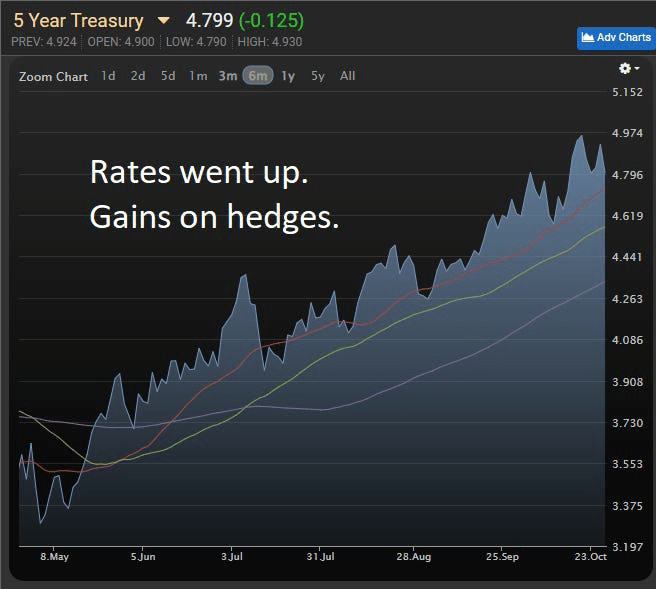

Hedges produced some beneficial properties:

MBSLive

The decline in property was materially bigger than the achieve from hedges.

The enterprise mannequin is extremely leveraged, so the guide worth swung a lot additional.

Guide Worth

Fast lesson. Ought to an company mortgage REIT commerce at an enormous premium to guide worth? No. A brand new one may be created at guide worth. Why would you pay an enormous premium to purchase a portfolio of MBS and hedges? What ought to a mortgage REIT do if it trades at an enormous premium? It ought to concern a bunch of shares. Why? As a result of they will take the money and instantly make investments it into their mannequin. In case you have $100 of guide worth, why wouldn’t you need another person to present the REIT $115 for a share? His share is not any higher than yours. He’s lifting your guide worth.

Sorry, take into consideration mutual funds.

You personal 1/tenth of a mutual fund that solely has $1,000 of property. Faux there are not any overhead bills.

Your place is value $100.

Now think about there’s some sucker who will purchase 5 shares for $115 per share. Faux that is authorized as a result of it’s authorized once we take care of publicly traded REITs.

So the fund points 5 shares at $115 and provides the money to the fund.

There are 15 shares excellent and the entire worth of the fund is $1,575.

How a lot is your 1 share value?

$1,575 / 15 = $105.

The worth of your place simply elevated by $5.

There’s nothing proprietary concerning the property this fund owns. The fund merely invests the brand new capital in related property to the present capital. Your place has 5% extra of every part.

That’s higher. That’s how the market works. Extra is best. You need extra.

In follow, the corporate isn’t going to concern sufficient inventory to extend shares excellent by 50%. It’s going to be a smaller improve and a smaller achieve to guide worth. Nevertheless, getting 1% extra of every part remains to be nice. Who doesn’t need an additional 1% of every part?

In case your dealer may offer you an additional 1% to your share depend in each place, wouldn’t you need that?

That’s the lesson. Issuing shares above guide worth is nice.

Why don’t we try this for fairness REITs? Fairness REITs have not less than reasonably distinctive property and guide worth below GAAP is meaningless for them. Nevertheless, when fairness REITs commerce above NAV (Internet Asset Worth) we typically need them to concern shares.

Battle Name of the Fish

At most poker tables, there’s a mixture of sharks and fish. Over the course of many palms, the sharks take cash off the fish.

There’s a saying in poker. If you happen to can’t spot the fish, you’re the fish.

The REIT Discussion board

There’s a typical battle name I hear from fish. It goes like this:

“When rates of interest decline, we’re going to win so large. AGNC goes to tear larger.”

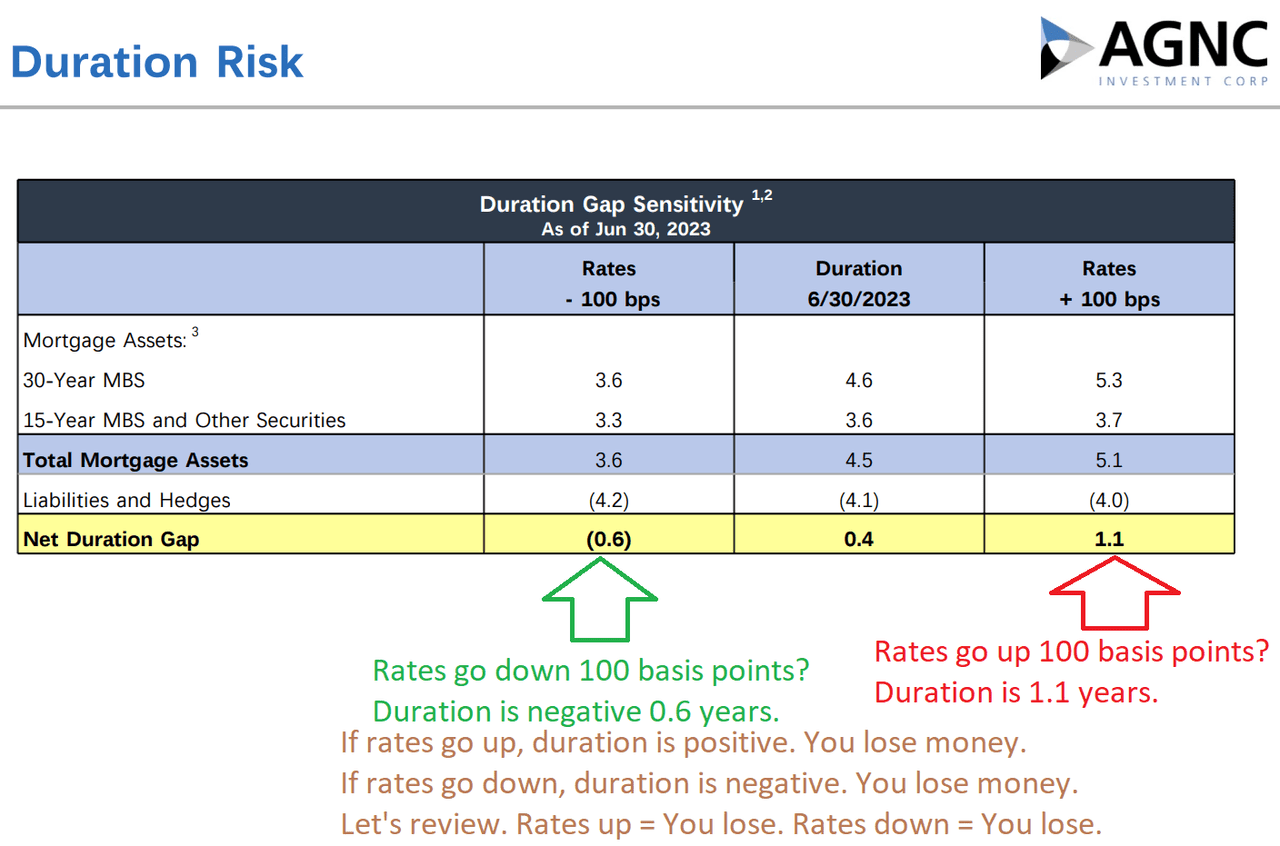

That’s simply fallacious. You don’t should consider me. AGNC instructed you.

AGNC, Commentary by The REIT Discussion board

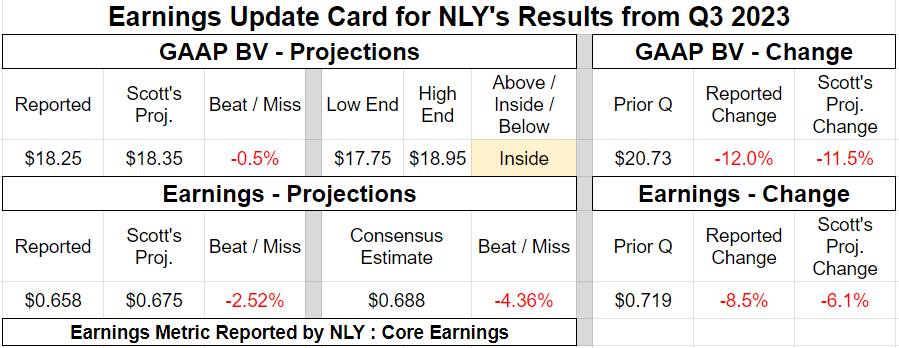

Transferring on to Annaly Capital Administration (NLY). Annaly just lately introduced their outcomes. The BV loss for NLY was smaller than for AGNC. NLY “solely” misplaced 12%.

The REIT Discussion board

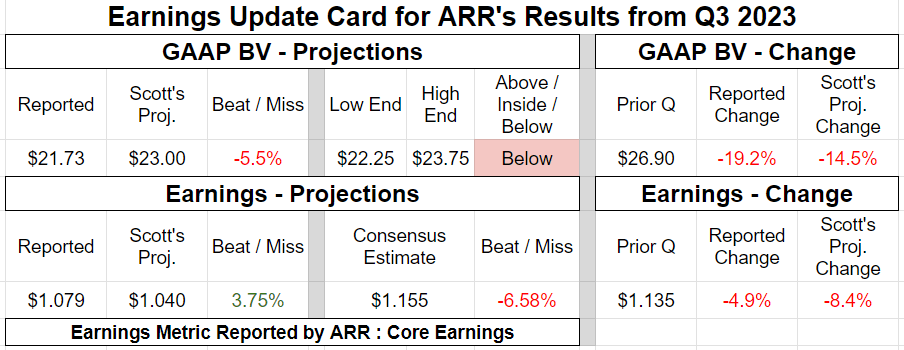

That is a lot better than ARMOUR Residential REIT (ARR).

The REIT Discussion board

ARR may’ve used some mid-quarter changes to guard their guide worth. As an alternative, they burned by way of guide worth quicker than a bonfire at a library.

The REIT Discussion board

What else to count on?

Extra carnage within the company mortgage REITs. Average guide worth losses for many different mortgage REITs. The most important harm is on the company mortgage REITs as a result of they’ve essentially the most publicity to rates of interest. Dynex Capital (DX) already reported. Outcomes have been very near our projections. Similar for Orchid Island Capital (ORC). We’re nonetheless awaiting outcomes from Two Harbors (TWO), Cherry Hill Mortgage (CHMI), and Invesco Mortgage (IVR).

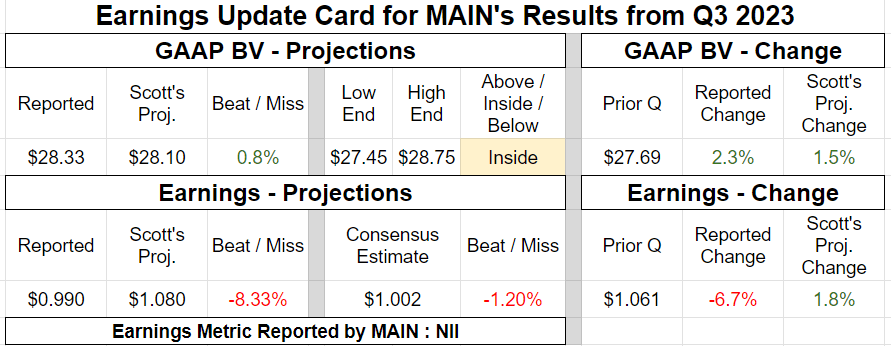

Alternatively, as predicted, BDCs are doing a lot better.

Most important Road Capital (MAIN) had a modest achieve in guide worth as they proceed to easily navigate the surroundings.

The REIT Discussion board

Conclusion

It’s been a tough quarter for company mortgage REITs. Traders are relying on charges to stay regular. If you happen to’re projecting charges to plunge, you actually don’t wish to purchase into the sector.

If charges truly stabilize, they might carry out very properly. Till then, it’s a really harmful space. To be truthful, it’s all the time harmful to play with shares in case you don’t perceive them. Holding till the reverse cut up and dividend lower doesn’t make it safer.

Editor’s Notice: This text covers a number of microcap shares. Please pay attention to the dangers related to these shares.

:max_bytes(150000):strip_icc()/Investopedia_Historyofcostofliving_colorv1-46383557fcda4f5a8e54f38e3096c4b8.png)

/what-difference-between-magnum-cum-laude-and-summa-cum-laude_V2-3ae02babdc714ea9adaeec0f0a6bf1a5.png)

/HabitsThatWillHelpYouPayOffDebtMay202021-51f5539c69cf4a7ba82f9f7059c10f5c.jpg)

:max_bytes(150000):strip_icc()/GettyImages-1529792128-03b50b785da845aebb6d00b232c45596.jpg)

{kind=link}