Non-Unique

I wish to briefly cowl the change in e book worth throughout mortgage REITs and BDCs in Q3 2023. You’ll discover:

Some did a lot better than others. Generally, company mortgage REITs had the worst time. BDCs had the best time.

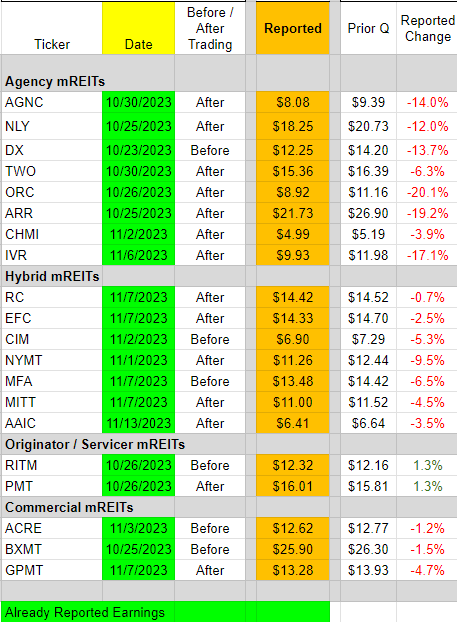

These are the e book worth modifications for the mortgage REITs as of Q3 2023 relative to Q2 2023:

The REIT Discussion board

Clearly the originator / servicer mREITs have been outperforming. We additionally noticed RC performing a lot better than many friends. We not too long ago moved RC into the hybrid classification. Beforehand, it was included within the originator / servicer classification. They acquired one other mortgage REIT (Broadmark) which tilted the portfolio into extra of a hybrid place.

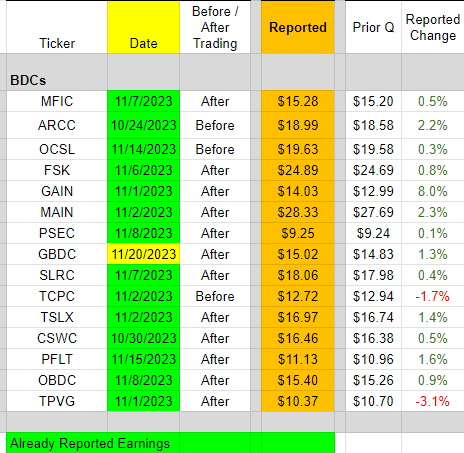

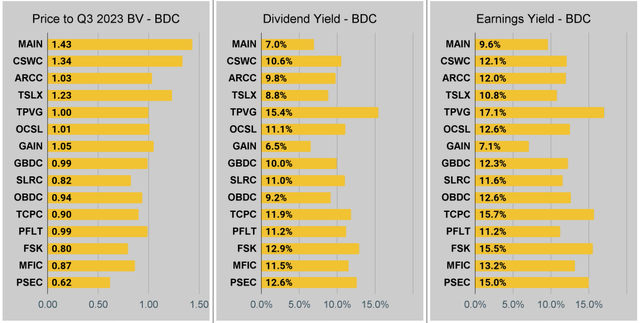

Listed here are the modifications for the BDCs:

The REIT Discussion board

GBDC hasn’t formally introduced This autumn outcomes but, however they offered a preliminary vary of $15.00 to $15.04, so we’ve used $15.02 within the outcomes. That’s a decent sufficient vary that I believe it is smart to make use of it.

How Do BDCs Work?

BDCs primarily put money into or lend to privately-held or small public corporations. Their investments can take numerous kinds, together with fairness stakes, debt financing (like loans), or a mixture of each. BDCs typically present capital to corporations which can be too small to boost funds publicly or too dangerous for conventional financial institution loans. BDCs earn revenue primarily by way of curiosity funds on debt investments and, to a lesser extent, from capital positive factors on fairness investments. In addition they could earn charges for offering managerial help or different companies to the businesses during which they make investments. BDCs are regulated as Regulated Funding Firms (RICs), which suggests they need to distribute no less than 90% of their taxable revenue to shareholders. In return, they’re usually not required to pay company revenue tax on earnings distributed to shareholders. This construction is much like that of Actual Property Funding Trusts (REITs).

The Irony in Company Mortgage REITs

A few of the company mortgage REITs have very comparable portfolios. Consequently, they typically produce comparable ranges of TER (Complete Financial Return). TER is the change in e book worth plus the dividend. It may be expressed in {dollars} and cents or in percentages. AGNC doesn’t have a giant benefit over Annaly Capital Administration or Dynex Capital. Nevertheless, AGNC trades at a materially larger price-to-book ratio. How is AGNC going to generate sufficient further returns to compensate for that distinction in price-to-book ratio?

It has a a lot larger “earnings yield,” however it doesn’t have that sort of edge on whole financial return. The earnings yield could be very closely influenced by accounting selections and hedging methods. The market seems to be pricing shares within the three REITs with a heavy emphasis on “earnings” quite than on producing whole returns. Dividend yield might be an element.

Simply be mindful a mortgage REIT can at all times select to declare larger dividends till they stop having the money. It’s only a return of capital. Utilizing “Core Earnings” simply doesn’t offer you that info. Many buyers want it did, so that they faux it should. That’s simply fallacious.

Consequently, buyers attempting to purchase the REITs with the next “earnings yield” could mislead themselves into pondering transitory elements are lasting advantages.

The Easy Technique

When you can inform when price-to-book ratios are unusually excessive, you recognize when to take a extra bearish outlook.

When you can spot them being unusually low, you’ll take a extra bullish outlook.

I used that course of to hammer AGNC with a bearish ranking once they have been buying and selling about 20% above tangible e book worth (utilizing our estimates as of that day). When AGNC preannounced the Q3 2023 outcomes, shares tumbled over 10% (and the full decline elevated to greater than 20%).

We climbed the turnbuckle and hoisted the belt:

The REIT Discussion board

That was the top of an ideal name. Or no less than it was a brief finish.

Higher Selection

For long-term positions, buyers ought to usually concentrate on the BDCs and the popular shares. It’s actually easy. Much less dividend cuts. Nevertheless, I do wish to emphasize that spreads are unusually broad presently. There are presently fairly a number of alternatives in mortgage REITs. I wouldn’t wish to be tied to them, however some nonetheless have enticing valuations. To be honest, I’ve been primarily shopping for most well-liked shares.

Because the begin of September, I’ve spent $227,485.55 shopping for most well-liked shares. That was partially offset by accumulating $177,375.83 from most well-liked share gross sales. The entire closed positions resulted in positive factors and all however 1 of the purchases is presently sitting on an unrealized achieve. The online influence was including about $50k to my sector allocation.

As I’ve talked about beforehand, I strategy this sector actively. I goal to benefit from mispricing between shares.

Inventory Desk

We’ll shut out the remainder of the article with the tables and charts we offer for readers to assist them monitor the sector for each frequent shares and most well-liked shares.

We’re together with a fast desk for the frequent shares that can be proven in our tables:

Click on to enlarge

When you’re on the lookout for a inventory that I haven’t talked about but, you’ll nonetheless discover it within the charts under. The charts include comparisons based mostly on price-to-book worth, dividend yields, and earnings yield. You received’t discover these tables wherever else.

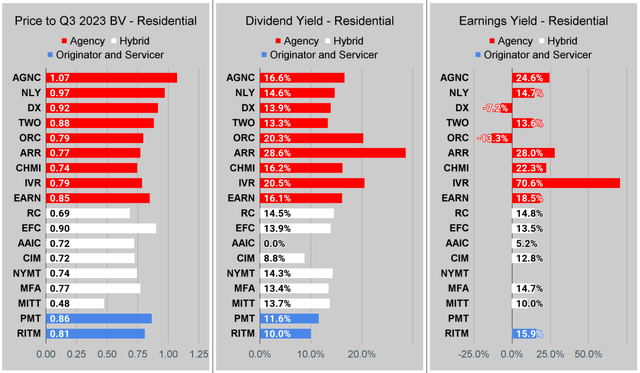

For mortgage REITs, please take a look at the charts for AGNC, NLY, DX, ORC, ARR, CHMI, TWO, IVR, EARN, CIM, EFC, NYMT, MFA, MITT, AAIC, PMT, RITM, BXMT, GPMT, WMC, and RC.

For BDCs, please take a look at the charts for MAIN, CSWC, ARCC, TSLX, TPVG, OCSL, GAIN, GBDC, SLRC, OBDC, PFLT, TCPC, FSK, PSEC, and MFIC.

This sequence is the simplest place to search out charts offering up-to-date comparisons throughout the sector.

Word on Ebook Values

I’ve up to date the charts to make use of Q3 2023 e book values. These are a lot nearer to present e book values. Firms that haven’t reported values for Q3 2023 can be clean. We don’t wish to put Q2 2023 and Q3 2023 BVs in the identical charts as a result of important modifications.

Residential Mortgage REIT Charts

Word: The chart for our public articles makes use of the e book worth per share from the quarter indicated within the chart. We use the present estimated (proprietary estimates) e book worth per share to find out our targets and buying and selling selections. It’s out there in our service, however these estimates should not included within the charts under. PMT and NYMT should not exhibiting an earnings yield metric as neither REIT gives a quarterly “Core EPS” metric. Presently, a number of different REITs additionally don’t have any consensus estimate.

Second Word: Because of the manner historic amortized price and hedging is factored into the earnings metrics, it is potential for 2 mortgage REITs with comparable portfolios to submit materially completely different metrics for earnings. I’d be very cautious about placing a lot emphasis on the consensus analyst estimate (which is used to find out the earnings yield). Particularly, all through late 2022, the earnings metric grew to become much less comparable for a lot of REITs.

The REIT Discussion board

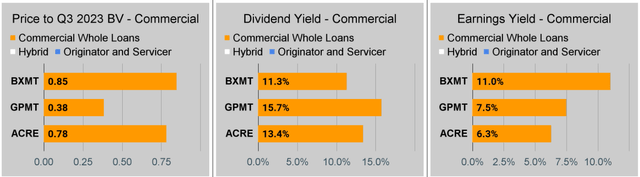

Industrial Mortgage REIT Charts

The REIT Discussion board

BDC Charts

The REIT Discussion board

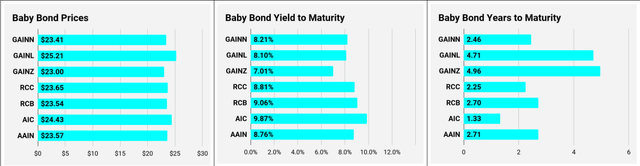

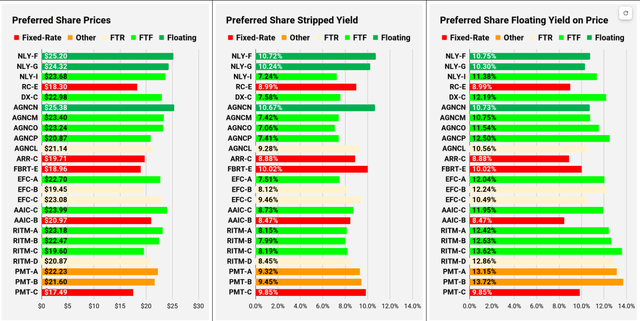

Most well-liked Share and Child Bond Charts

I modified the coloring a bit. We would have liked to regulate to incorporate that the primary fixed-to-floating shares have transitioned over to floating charges. When a share is already floating, the stripped yield could also be completely different from the “Floating Yield on Worth” as a result of modifications in rates of interest. For example, NLY-F already has a floating price. Nevertheless, the speed is barely reset as soon as per three months. The stripped yield is calculated utilizing the upcoming projected dividend fee and the “Floating Yield on Worth” is predicated on the place the dividend can be if the speed reset at the moment. For my part, for these shares the “Floating Yield on Worth” is clearly the extra vital metric.

Child Bonds

The REIT Discussion board

Most well-liked Shares

The REIT Discussion board

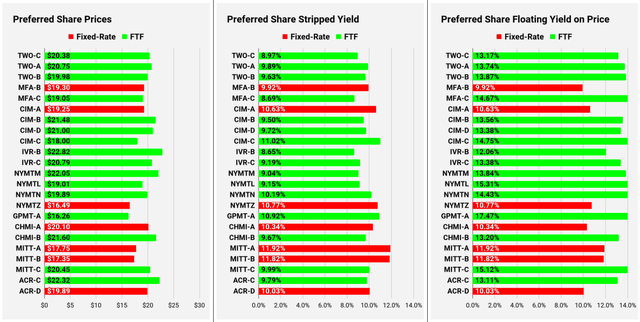

Extra Most well-liked Shares

The REIT Discussion board

Word: Shares which can be categorised as “Different” should not essentially the identical. For the aim of those charts, I lumped all of them collectively as “Different.” Now there are solely two left, PMT-A and PMT-B. These each have the identical problem. Administration claims the shares can be fixed-rate, though the prospectus says they need to be fixed-to-floating.

Most well-liked Share Knowledge

Past the charts, we’re additionally offering entry to a number of different metrics for the popular shares.

After testing out a sequence on most well-liked shares, we determined to attempt merging it into the sequence on frequent shares. In any case, we’re nonetheless speaking about positions in mortgage REITs. We don’t have any want to cowl most well-liked shares with out cumulative dividends, so any most well-liked shares you see in our column may have cumulative dividends. You’ll be able to confirm that by utilizing Quantum On-line. We’ve included the hyperlinks within the desk under.

To higher set up the desk, we would have liked to abbreviate column names as follows:

Worth = Latest Share Worth – Proven in Charts

S-Yield = Stripped Yield – Proven in Charts

Coupon = Preliminary Fastened-Fee Coupon

FYoP = Floating Yield on Worth – Proven in Charts

NCD = Subsequent Name Date (the soonest shares might be known as)

Word: For all FTF points, the floating price would begin on NCD.

WCC = Worst Money to Name (lowest internet money return potential from a name)

QO Hyperlink = Hyperlink to Quantum On-line Web page

Click on to enlarge

Second batch:

Click on to enlarge

Third batch:

Click on to enlarge

Technique

Our aim is to maximise whole returns. We obtain these most successfully by together with “buying and selling” methods. We recurrently commerce positions within the mortgage REIT frequent shares and BDCs as a result of:

Costs are inefficient.

Long run, share costs usually revolve round e book worth.

Quick time period, price-to-book ratios can deviate materially.

Ebook worth isn’t the one step in evaluation, however it’s the cornerstone.

We additionally allocate to most well-liked shares and fairness REITs. We encourage buy-and-hold buyers to think about using extra most well-liked shares and fairness REITs.

Editor’s Word: This text covers a number of microcap shares. Please pay attention to the dangers related to these shares.

:max_bytes(150000):strip_icc()/shutterstock_211961536-5bfc363046e0fb00260d2dd3.jpg)

:max_bytes(150000):strip_icc()/What-difference-between-standard-Error-means-and-standard-deviation_color-1c203133aca641aca0d03936d9558693.jpg)

/what-difference-between-magnum-cum-laude-and-summa-cum-laude_V2-3ae02babdc714ea9adaeec0f0a6bf1a5.png)

{kind=link}