Hundley_Photography/iStock by way of Getty Photos

This text was coproduced with Leo Nelissen.

It’s time to speak about what could also be one of many coolest shares available on the market.

An organization flying underneath the radar.

An organization that advantages from the oil growth with out producing a single drop of oil.

An organization that has its roots within the railroad business that was once a land belief and now advantages from the shale revolution as a C-Company.

That firm is the Texas Pacific Land Company (NYSE:TPL).

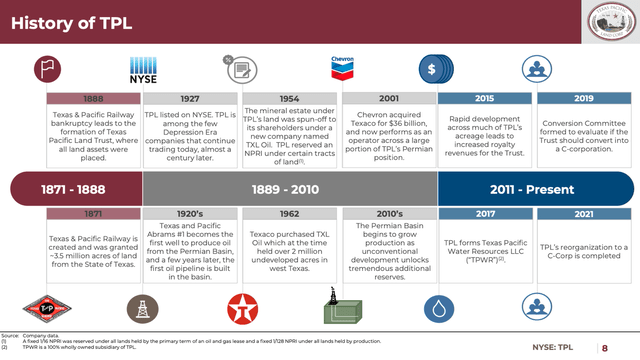

Texas Pacific Land, tracing its roots again to 1888, was initially established as Texas Pacific Land Belief.

Working underneath a Declaration of Belief, the entity’s major objective was to obtain and handle intensive land tracts within the State of Texas, beforehand owned by the Texas and Pacific Railway Firm.

This railroad is now a component of the mighty Union Pacific Company (UNP), the nation’s largest stock-listed railroad.

Texas Pacific Land Co

A big chapter in TPL’s historical past unfolded on January 11, 2021, when the belief underwent a strategic reorganization.

This transformative course of marked the transition from Texas Pacific Land Belief to Texas Pacific Land Company.

It’s not a REIT and has maybe one of many most secure enterprise fashions on this planet:

Purchase land, they don’t seem to be making it anymore. – Mark Twain

Nevertheless, it doesn’t simply personal random land.

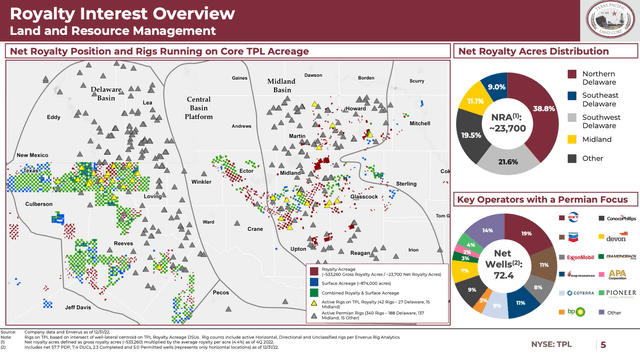

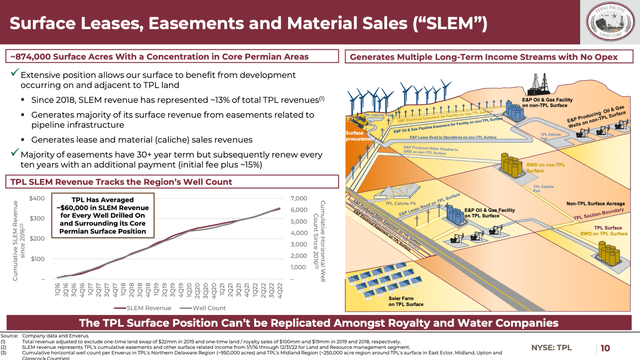

It owns a number of the most dear land wherever on this planet, as TPL stands as one of many largest landowners in Texas, boasting roughly 874,000 acres in West Texas, primarily concentrated within the Permian Basin.

This brings me to a quick historical past of the largest oil and fuel basin in the USA.

The Place To Be: Permian Actual Property

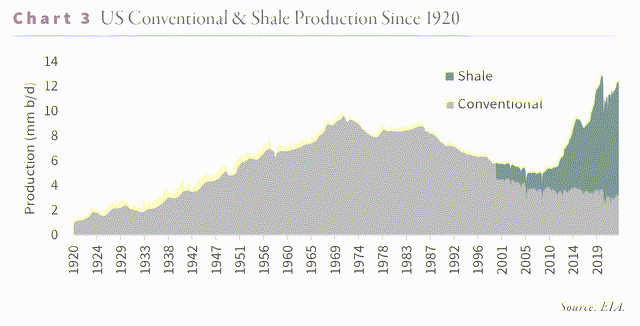

Oil is without doubt one of the most necessary forces transferring macro numbers like inflation. One motive why the USA – and most Western nations – noticed subdued inflation between the Nice Monetary Disaster and the pandemic is the shale revolution.

The chart under reveals simply how vital the shale revolution was in the USA, because it ended a multi-decade decline in oil manufacturing.

(Goehring & Rozencwajg)

The shale revolution was so wild that it triggered provide development to considerably outpace demand development, which paved the wave for 2 main oil value declines in each 2015 and 2020.

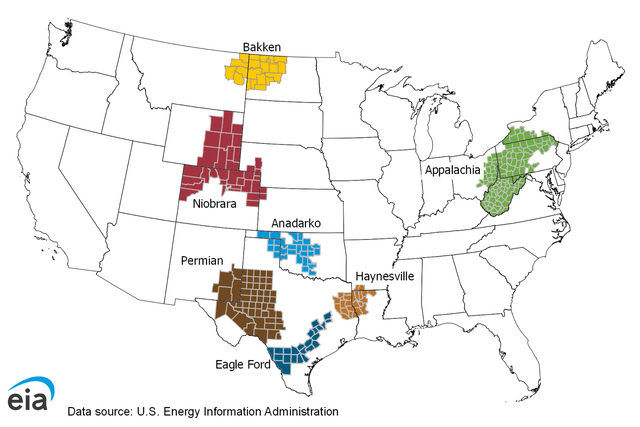

With that in thoughts, the U.S. is dwelling to seven main oil and fuel basins.

(Power Data Administration)

Though all of those basins are necessary, one in every of them stands out.

The Permian is the one most necessary basin in the USA for 2 causes:

It’s the largest basin.

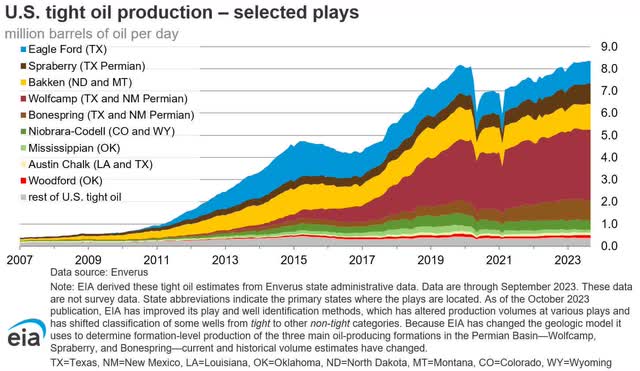

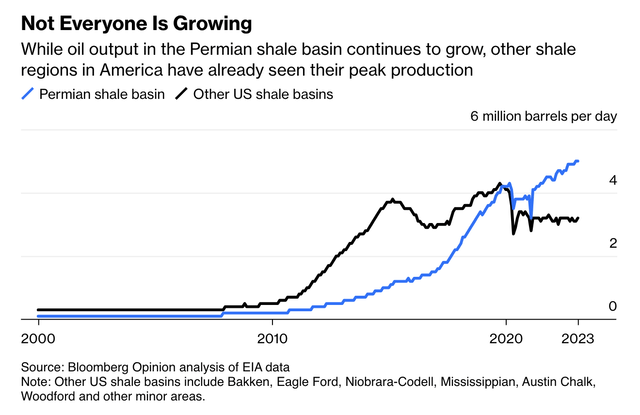

As we will see within the chart under, in 2007, the U.S. barely produced any tight oil (shale/unconventional oil). That quantity is at present shedding momentum at greater than 8 million barrels per day.

The Permian produces most of it, as it’s dwelling to Spraberry, the Wolfcamp, and Bonespring performs.

(Power Data Administration)

Moreover, the information reveals that shale output is shedding steam. Producers are operating out of Tier 1 inventories, and most want to give attention to free money movement as a substitute of fast manufacturing development.

This manner, they stress provide development, making steep oil value declines sooner or later much less doubtless. It additionally permits them to spend additional cash on dividends and buybacks.

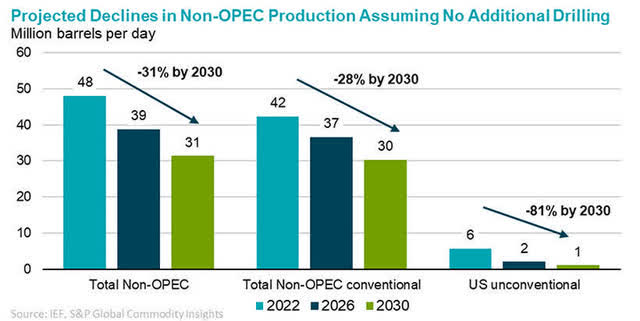

For example Tier 1 inventories, the Worldwide Power Discussion board estimates that with out new manufacturing, U.S. unconventional manufacturing might see an 81% decline by 2030!

(Worldwide Power Discussion board)

This is without doubt one of the explanation why we’re bullish on oil (long-term), as unconventional provide development is quickly slowing down, and OPEC is having fun with its regained pricing energy to guard increased oil costs.

This brings me to motive two:

The Permian is the place for provide development.

As highlighted by Bloomberg’s power professional Javier Blas, who confirms our prior feedback, the shale sector is grappling with the aftermath of capital destruction and altering investor priorities. The business, as soon as pushed by development on the expense of income, now prioritizes returns for shareholders.

From Shale 1.0, characterised by fast development and heavy spending, to the survival mode of Shale 2.0 through the 2014 value conflict, the business has undergone transformations. Now, in Shale 3.0, the main target is on dividends and share buybacks, signaling a shift from development to income.

For now, the Permian is the one play able to rising persistently! Please be aware that the present provide output is struggling. That’s cyclical, not an indication of peak manufacturing.

Bloomberg

Nevertheless, business leaders predict “Peak Permian” inside the subsequent 5 to 6 years, which additional provides to the oil bull case.

Now, we’re seeing a wave of main M&A initiatives to extend Permian manufacturing.

This consists of Exxon Mobil (XOM) shopping for Pioneer Pure Assets (PXD) and Chevron (CVX) shopping for Hess (HES).

In terms of proudly owning actual property, the Permian is the place to be. It nonetheless has years of development forward of it. It additionally has very low breakeven costs, permitting firms to maintain drilling when different basins are seeing decrease output.

On prime of that, Texas is without doubt one of the greatest locations for renewable power like photo voltaic.

In 2022, Texas was the second-biggest state for photo voltaic power. It will get roughly 5% of its power from photo voltaic. In 2021, the state put in 6 gigawatts of photo voltaic power. In 2022, that quantity was barely under 4 gigawatts.

All of this provides to the enchantment of proudly owning Permian actual property, the place the solar shines brilliant, oil manufacturing is considerable and low cost, and new pipelines are wanted to maintain up with increased manufacturing.

Shopping for High-Tier Oil Royalties

As we already briefly talked about, Texas Pacific Land doesn’t produce oil. It owns the very best actual property within the business.

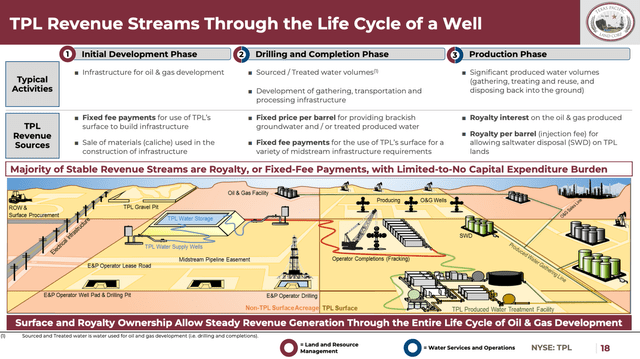

Basically, TPL’s income mannequin spans your complete oil and fuel improvement worth chain.

Texas Pacific Land Corp

Though not an oil and fuel producer, the corporate advantages from mounted charge funds, materials gross sales, and royalties throughout completely different phases of properly improvement. Amongst its largest clients are

Occidental Petroleum (OXY) Chevron (CVX) Exxon Mobil (XOM) EOG Assets (EOG) ConocoPhillips (COP)

…that are the largest operators within the Permian.

Texas Pacific Land Corp

Extra income sources embrace pipeline, energy line, and utility easements, in addition to business leases.

Along with that, TPL is increasing its Water Providers and Operations phase.

By offering full-service water choices within the Permian Basin, the corporate faucets into a vital facet of oil and fuel operations.

Texas Pacific Land Corp

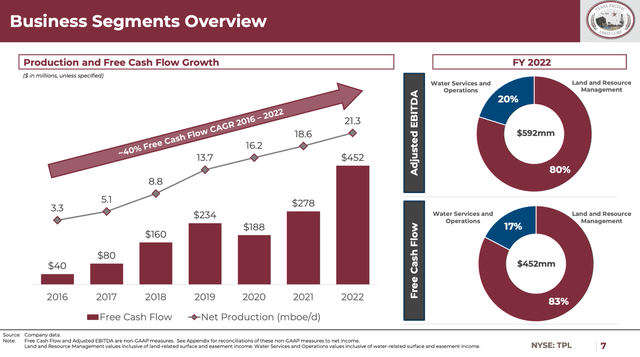

In 2022, the corporate noticed 21.3 thousand barrels of oil equal (“BOE”) of day by day royalty manufacturing. That’s up from lower than 2 thousand BOE in 2014. In 2016, the corporate’s royalties have been based mostly on 3,300 BOE per day.

This allowed the corporate to develop free money movement from $40 million in 2016 to greater than $450 million in 2022. That’s a 40% compounding development fee!

Texas Pacific Land Corp

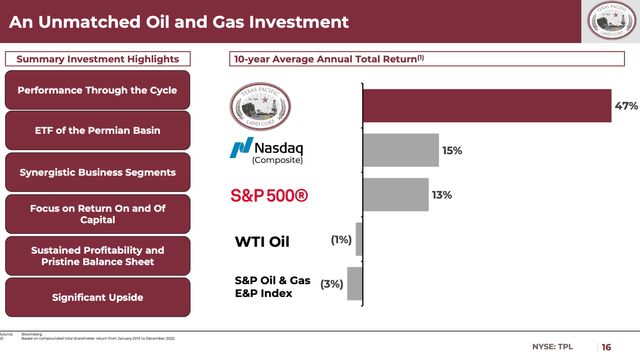

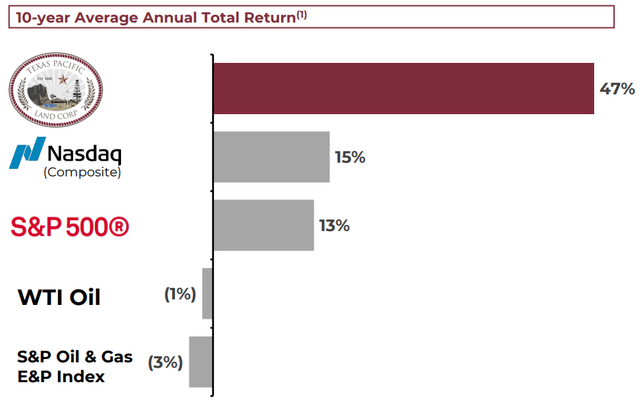

This efficiency allowed TPL shares to crush every little thing of their path.

The ten-year common annual complete return of TPL shares between January 2013 and December 2022 was 47%. The red-hot Nasdaq returned 15% per yr throughout this era. Additionally, throughout this era, oil costs fell by 1% per yr, inflicting oil and fuel shares to fall by 3% per yr. This reveals that TPL is an oil play with a lot much less cyclical threat.

Texas Pacific Land Corp

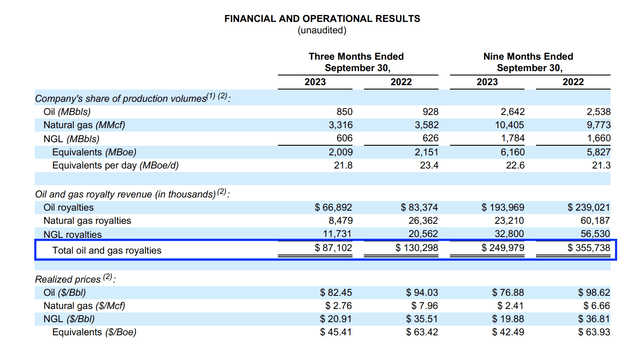

Nonetheless, as one can think about, the corporate stays cyclical, as its manufacturing royalties rely upon the value of oil and fuel.

As we will see under, in 3Q23, the corporate generated $87 million in oil and fuel royalties. That’s down from $130 million in 3Q22 and roughly half of complete revenues. The opposite half was comparatively steady.

Manufacturing volumes have been down barely, with costs taking an even bigger hit, because the decrease a part of the desk under reveals.

Texas Pacific Land Corp

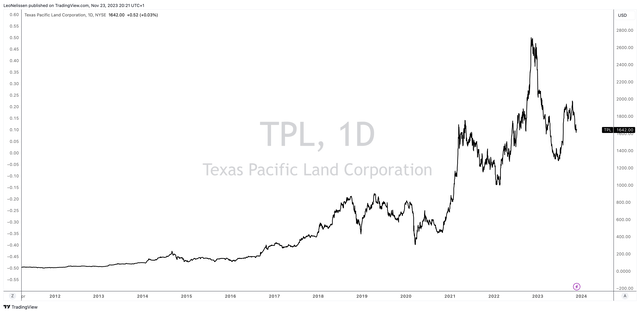

Consequently, this yr, the $13.2 billion market cap firm is down 30% year-to-date. The inventory is buying and selling 38% under its 52-week excessive.

TradingView TPL

This brings me to the following a part of this text.

TPL Dividends

Let’s begin with the disappointing information.

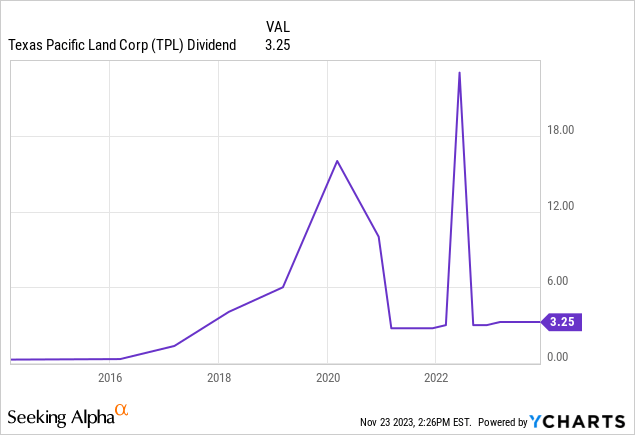

The corporate has a daily quarterly dividend of $3.25 per share.

This interprets to a yield of 0.80%, as the value of a single inventory is $1,642.

The excellent news is that TPL tends to pay juicy particular dividends throughout occasions of elevated revenue.

In search of Alpha

In 2022, the corporate paid $12 in common dividends (4 x $3.00) on prime of a particular dividend of $20 within the second quarter. This brings the full dividend to $32. That’s 1.9% of the present inventory value.

Though 1.9% continues to be nothing in comparison with high-yield upstream oil performs, this inventory must be seen as a complete return play as a substitute of an revenue inventory.

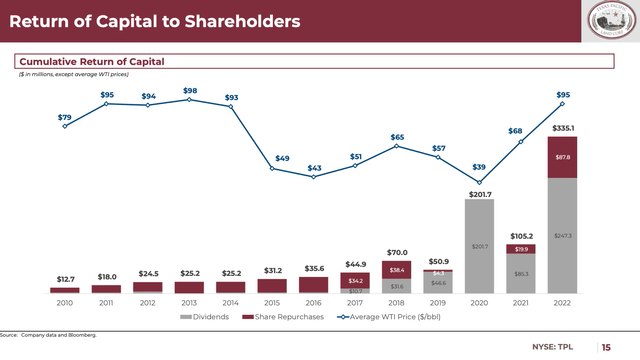

Trying on the chart under, we see that dividend traders profit from a mixture of increased manufacturing and robust WTI costs, permitting TPL to purchase again inventory on prime of distributing dividends.

This has added to its sturdy complete return image.

In search of Alpha

It additionally helps that the corporate has no constructive web debt.

As of September 30, the corporate has complete property of $1.1 billion and complete liabilities of simply $115 million.

That is primarily accounts payable and unearned income.

It has no monetary debt.

Even higher, it has $650 million in money!

That’s 4.8% of its market cap.

This paves the way in which for juicy dividends down the highway, as analysts are very upbeat about its means to generate free money movement.

Analysts imagine that TPL can generate roughly $580 million in 2024 free money movement, adopted by a surge to $680 million in 2025.

This might translate to a free money movement yield of 4.3% and 5.0%, respectively.

When including that the corporate has a major money place, particular dividends are very prone to occur in each 2024 and 2025 – until oil costs implode.

Talking of oil costs, we imagine that TPL will beat free money movement estimates, as we now have little doubt that we’re in a protracted upswing for oil costs, which ought to profit TPL each from a pricing and volumes point-of-view – on prime of water royalties and advantages from renewables and pipelines.

“Every part nonetheless appears to be like good. I believe we nonetheless anticipate total to see manufacturing development within the coming yr. Once more, like we mentioned, that basically excessive quantity of permits, the faster turnaround of permits and DUCs, all of these issues proceed to be constructive indicators.

And I believe as a few of these large pads get introduced on-line, and we get via a few of these temperature points and pipeline constraint points, we will see that manufacturing come to market to the advantage of TPL.” – TPL 3Q23 Earnings Name.

So, what in regards to the valuation?

Valuation

The valuation is difficult, as some traders have a look at TPL as a REIT, which it isn’t.

Provided that TPL doesn’t have a dependable 5-6% yield like some REITs, traders are likely to lose curiosity relatively shortly.

In spite of everything, it takes a deeper understanding of oil fundamentals to seek out the worth behind this ticker.

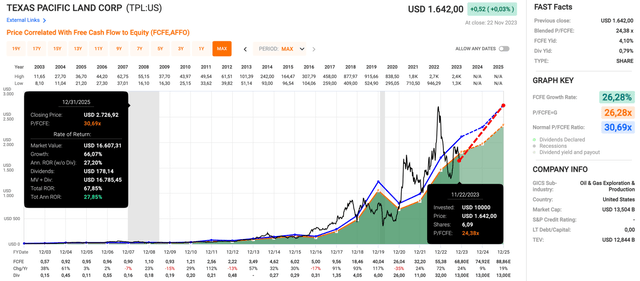

TPL is definitely attractively valued, as we imagine that the inventory must be valued based mostly on its means to generate money.

Therefore, we’re utilizing the price-to-FCFE ratio.

FCFE is free money movement to fairness, which is the amount of money obtainable to shareholders after bills, reinvestments, and debt funds.

Over the previous twenty years, the normalized P/FCFE ratio was 30.7x. That could be elevated. Nevertheless, keep in mind that the corporate is exhibiting excessive development charges.

This yr, FCFE is predicted to develop by 24%. Subsequent yr, FCFE is predicted to develop by 9%, adopted by 19% development in 2025.

Though these numbers are tied to the value of oil and drilled volumes, they present the corporate’s potential.

Having mentioned that, as a result of its poor inventory value efficiency, TPL is buying and selling at a blended P/FCFE ratio of 24.4x.

A return to 30.7x FCFE by incorporation of anticipated development charges would suggest a good inventory value of $2,730, which is 66% above the present value.

It might suggest a 28% annual return via 2025.

FAST Graphs

That is clearly a theoretical worth topic to macroeconomic developments.

Nonetheless, TPL seems to be attractively valued.

The present consensus value goal is $2,180.

Takeaway

We imagine that TPL would make an excellent addition to your broader “actual property” portfolio that features infrastructure REITs like American Tower (AMT) and Digital Realty (DLR), in addition to power performs like Enbridge (ENB) and TC Power (TRP).

Including TPL publicity would assist you to profit from rising manufacturing within the Permian, pricing advantages from different basins operating out of steam, and add uncorrelated power publicity.

In spite of everything, TPL just isn’t a driller.

The one draw back is that TPL just isn’t a high-yield inventory with a daily dividend.

Nonetheless, it makes up for that by having the ability to develop quickly and with occasional particular dividends.

Moreover, its fortress steadiness sheet means it’s well-protected towards elevated charges.

Additionally, TPL has a long-standing coverage to repurchase shares with extra money. As famous within the 2015 annual report,

“As supplied in Article Seventh of the Declaration of Belief, dated February 1, 1888, establishing the Belief, it should proceed to be the apply of the Trustees to buy and cancel excellent certificates and sub-shares. These purchases are usually made within the open market and there’s no association, contractual or in any other case, with any particular person for any such buy.”

By way of efficiency, TPL has been an absolute gem, and I have to confess that I first heard about this choose from Porter Stansberry who touted this unknown land belief over a decade in the past.

TPL Investor Deck

Simply going again over a decade, you may see that TPL has grown by 3X Nasdaq and the S&P 500.

Now, I might problem you to seek out me one other inventory that has seen 3X efficiency in a 10-year interval, particularly a mid-cap or a bigger cap firm like Texas Pacific.

That pattern continues even this yr.

Therefore, we fee TPL a Purchase. We’re on the hunt to purchase the inventory on weak point and hope to include it into our portfolio over the following few quarters.

Causes To Be Bullish TPL Inventory

Prime Actual Property Holdings: TPL owns 874,000 acres within the Permian Basin, the most important U.S. oil and fuel basin, providing strategic positioning for ongoing and future developments. Numerous Income Streams: Regardless of not producing oil, TPL generates income via mounted charges, materials gross sales, and royalties, with main clients like Occidental Petroleum, Chevron, Exxon Mobil, EOG Assets, and ConocoPhillips. Spectacular Monetary Efficiency: TPL’s sturdy financials embrace a 40% compounding development fee in free money movement from 2016 to 2022, resulting in a 10-year common annual complete return of 47%. Dividend Potential: TPL pays common and particular dividends, with a complete dividend of $32 in 2022, offering a complete return play for traders. Sturdy Stability Sheet: The corporate has no monetary debt, complete property of $1.1 billion, complete liabilities of $115 million, and $650 million in money, positioning it properly for dividends and future development. Enticing Valuation: TPL is attractively valued based mostly on its means to generate money, with a blended P/FCFE ratio of 24.4x, suggesting the potential for a good inventory value of greater than $2,700. Progress Potential: Analysts mission TPL’s free money movement to succeed in $580 million in 2024 and $680 million in 2025, with the potential for a 28% annual return via 2025.

Word: Brad Thomas is a Wall Avenue author, which implies he is not at all times proper along with his predictions or suggestions. Since that additionally applies to his grammar, please excuse any typos you could discover. Additionally, this text is free: Written and distributed solely to help in analysis whereas offering a discussion board for second-level pondering.

{kind=link}